Personal Wealth Management / Market Analysis

As Markets Hit New Lows, Remember the Basics

It is difficult, but don’t let frustration and emotion over what has happened this year drive your portfolio decisions going forward.

Global stocks hit new lows this week as the bear market persists—extending a disappointing year. Naturally, many investors are frustrated, which is understandable. But frustration often gives rise to the urge to act—doing something, anything, can feel like taking back some control in an uncomfortable situation. However, this long into a bear market, such urges can easily be dangerously counterproductive. As challenging as this year has been, reacting to the past is arguably the biggest risk investors can take right now, in our view.

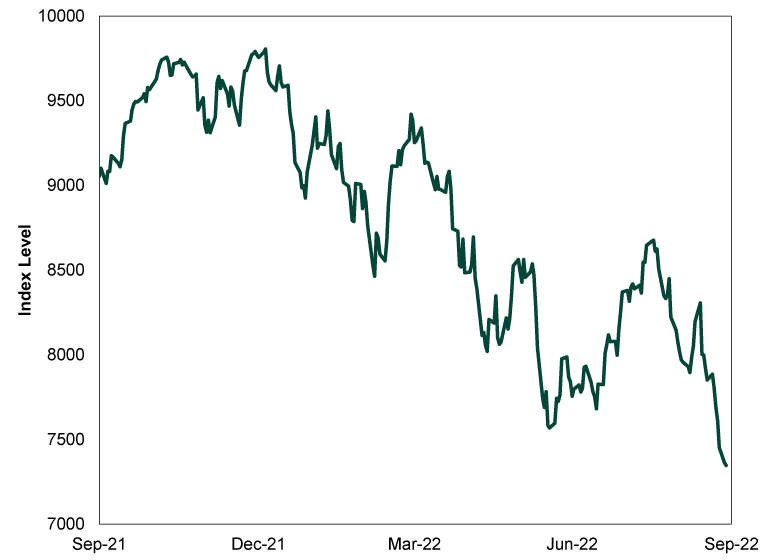

If the past two weeks feel like a bad case of déjà vu, your intuition isn’t far off base. This year has been a rollercoaster for global stocks. After a rocky spring, world stocks first crossed -20%—the threshold for bear markets (typically prolonged and fundamentally driven declines)—on June 13. Days later, on June 17, the MSCI World began a rebound. But after two months, the summertime rally faded and early this week, world stocks hit a new low—down -15.3% since August 16 and -25.1% since the January 4 peak.[i]

Exhibit 1: A Challenging Period for Global Stocks

Source: FactSet, as of 9/27/2022. MSCI World Index returns with net dividends, 9/30/2021 – 9/27/2022.

Enduring bear markets is frustrating and challenging, but it is vital to remember: Investors seeking long-term equity-like returns don’t need to sidestep bear markets to achieve that aim. Now, if you identify a huge, multi-trillion dollar negative developing that markets haven’t already weighed, reducing stock exposure can make sense. However, we didn’t see this bear market forming early enough to encourage readers to act. That is humbling, but it doesn’t change what we think is the wisest course of action now.

Absent early bear market identification and taking action, we counsel going back to the basics. Yes, we know. “Patience,” “stay with it” and all the like may sound like tired mantras—but that doesn’t make them unwise. Sometimes, the things you don’t want to hear are still right, important and smart. Here are a few such concepts: One, don’t exit stocks because of what has already happened. Selling now locks in losses, and if you are out of the market when a recovery begins, it will become much harder to recoup those losses. You could then be fighting equal and opposite emotions that want to keep you sidelined to mitigate potential declines. It is a recipe for potentially missing a recovery. Again, avoiding negativity isn’t essential to earn markets’ long-term returns. The S&P 500’s average annualized return of 10.3% includes all the bear markets from 1926 – 2021.[ii] In our view, if you seek growth commensurate with stocks’ long-term results, earning market-like returns is critical.

Also critical: making investment decisions based on what lies ahead, as markets are forward-looking. Since stock prices move most on the gap between expectations and reality, weigh how sentiment aligns with economic and political fundamentals. Based on what we have observed, moods today are extremely dour. Surveys of investors and consumers highlight rampant pessimism, as does business activity. For instance, the IPO market is having its slowest year in more than a decade, and merger and acquisition (M&A) activity has stalled, with dealmakers blaming higher costs and economic slowdown fears.[iii]

By no means are we saying things are uniformly positive. We also don’t dismiss headwinds from elevated inflation and high energy costs in particular, which could very well hinder growth in parts of the global economy. But we also see signs reality isn’t as poor as many think. Take the New York Federal Reserve’s Global Supply Chain Pressure Index. While still at historically high levels, it has been trending downward for the past four months—suggesting global supply chain pressures, one of 2022’s biggest worries, have been easing.[iv] Fisher Investments Executive Chairman and founder Ken Fisher recently offered a comprehensive look at other sources of reduced price pressures ranging from slowing money supply growth to smaller budget deficits to falling commodity prices—give it a look at RealClearMarkets. Politics should also prove a tailwind as we move into Q4—with the US midterm elections a big source of falling uncertainty—and into 2023. Though just one factor, it is worth weighing for investors. Finally, markets re-testing lows isn’t uncommon in bear markets, and it doesn’t mean more downside automatically awaits before a recovery, as past returns never predict. And therein lies the chief problem many investors are wrestling today: Emotions are shaped and colored by the recent past, but that won’t help you foresee what is ahead.

[i] Source: FactSet, as of 9/28/2022. MSCI World Index returns with net dividends, 8/16/2022 – 9/27/2022 and 1/4/2022 – 9/27/2022.

[ii] Source: Global Financial Data, as of 3/28/2022. S&P 500 Total Return Index, 12/31/1925 – 12/31/2021.

[iii] “IPO Stocks Have Tumbled, Hobbling Demand for New Listings,” Corrie Driebusch, The Wall Street Journal, 9/26/2022 and “Season of Shelved M&A Surpasses $150 Billion as Credit Woes Bite,” Manuel Baigorri and Ben Scent, Bloomberg, 8/26/2022.

[iv] Source: Federal Reserve Bank of New York, Global Supply Chain Pressure Index, https://www.newyorkfed.org/research/gscpi.html, as of 9/27/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today