Personal Wealth Management /

Bonds Wiggle, Will Stocks Jiggle?

Do bond markets know something stocks don’t?

Stock markets rising (with an eerie calm?). Plunging bond yields, leading to a possible reckoning. No, it’s not the investment world’s version of The Twilight Zone: It’s reality, which has led to a lot of speculation about what it all means. But in our view, gyrating bond markets aren’t signaling a big negative that stocks are either missing or will soon see. Both markets are about equally forward looking and the preponderance of evidence is on the side of continued growth and bull market ahead. Bond gyrations are likely just regular old market volatility.

Much has been made of the widely unexpected drop in the 10-year US Treasury yield this year to date. Ten-year yields started 2014 a shade above 3.0% and have fallen by about 0.4 percentage point since. Few thought falling rates were likely this year, given the Fed officially announced it would taper quantitative easing (QE) in December, with the purchase pace slowing in mid-January. If the Fed slowed the use of what many presume are quasi-magical powers, higher rates would surely come. But they haven’t, which has some folks scratching their heads, asking what these bouncy bond yields mean—particularly in light of a stock market that has placidly and gradually worked its way to several new record highs this year.

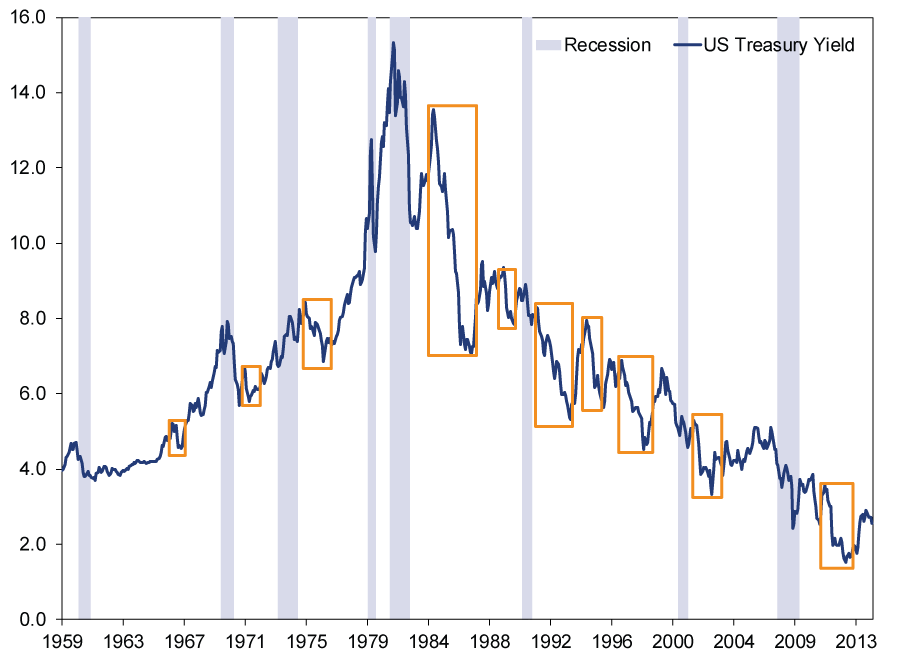

The most common assumption we’ve seen posits economic weakness is looming, weakness complacent stock investors don’t see. Supposedly sober bond investors flock to more “stable” fixed income investments, pushing prices up and yields down, while wacky equities markets just don’t pay any attention. But is there any evidence bond market movements are more predictive than stocks? Are bond markets really so much more sober? The answer to both is no. Consider the 10-Year Treasury yield since 1959.

During those five and a half decades, the US went through eight recessions, as defined by the National Bureau of Economic Research (NBER). As Exhibit 1 shows, with one exception (the 1973-1975 recession), US Treasury yields have overall fallen during recessions. But it’s a mixed bag see before the recession started. Both downturns in the early 1980s followed rising long yields. Same with the early 1970s. Also, there are nearly just as many times where yields fell (orange squares in Exhibit 1) and the US economy expanded. The big drop in the mid-1980s? Very expansionary period. Ditto for the period November 1994 – January 1996, when yields fell by 2.5 percentage points. They then blipped higher before falling another percentage point between July and December 1996. Falling yields don’t automatically mean economic weakness ahead.

Exhibit 1: US 10-Year Treasury Yields Since 1959

Source: St. Louis Federal Reserve and NBER, 10-year Treasury yields for the period 02/01/1959 to 05/01/2014.

It’s possible bond markets are catching something stocks aren’t and bond investors are acting more rationally than stock investors. But that doesn’t make it probable. Bond markets don’t possess some secret knowledge nobody else has access to—all markets tend to price in widely known information. Maybe the bond market is extrapolating lowflation forward (rationally or irrationally). There isn’t anything about the bond market that makes it the more rational arbiter of future economic results.

For example, when former Fed Chair Ben Bernanke alluded to tapering QE purchases in May 2013, both bond and stock markets didn’t wait for the actual “taper” to begin. The US Treasury yield began rising almost immediately, pricing in the impact of the Fed slowing long-yield depressing bond purchases. The S&P 500 started digesting the news right away, too. After some short-term wiggles, stocks continued rising for the rest of the year—stocks don’t seem to have considered the taper a detriment. Similarly, in 2008, stocks and bond yields both fell, reflecting the actual approach of economic weakness. However, preceding the 1970 recession, stocks were falling and yields rising. If you believe falling yields are the indicator of weakness ahead—we don’t—were bond yields acting irrationally then, while stocks were the paragon of sobriety?

Relying on only one indicator to forecast what markets will do runs the risk of missing the bigger picture. You need more context, and that context today doesn’t support the notion bonds are acting in a more prescient manner. Consider the forward-looking Leading Economic Index (LEI), a composite of 10 mostly forward-looking indicators (including the bond yield spreads and stock prices, testament to their ability to foresee economic conditions ahead). Recession has never followed a rising LEI trend, and it rose 0.4% in the latest reading (April), the third consecutive increase. LEI’s other inputs include manufacturers’ new orders to building permits for new housing, which were up in April. Services new orders, not in the LEI but representing the largest sector of the US economy, are growing. Today’s orders are tomorrow’s production. Relying on just one indicator (bond yields) to the exclusion of these others seems an odd selection.

Politically, upcoming US midterm elections suggest further gridlock in the near future—a positive for markets, which like a lack of sweeping legislative change. And despite the rise in investor optimism, we’re still far from euphoria—which, ironically, this focus on yield volatility to the exclusion of virtually every other leading indicator illustrates. Folks arguing bond market volatility portends stock market volatility is evidence of the doubts still lingering around this bull. Investor sentiment hasn’t completely flipped yet.

So what’s up with bond yield volatility? We’d suggest it’s just that—volatility. In our view, that there have been wiggles in bonds lately says nothing more than the lack of wiggles in stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today