Personal Wealth Management / Politics

Considering the CARES Act ‘Cliffs’

Stocks’ future path doesn’t depend on extending various CARES Act benefits, in our view.

Despite budding signs of a nascent US economic recovery, fears of renewed weakness persist. The latest: Many pundits worry Congress might fail to extend various CARES Act programs. In a throwback to 2012, they argue these benefits’ expiry sets up “fiscal cliffs” the recovery could plunge off of and deepen the recession. While this may make for tense political theater, we don’t believe this bull market’s future hinges on whether or not Congress extends certain programs. These fears seem mostly like common early bull market worries that stimulus alone is keeping stocks afloat.

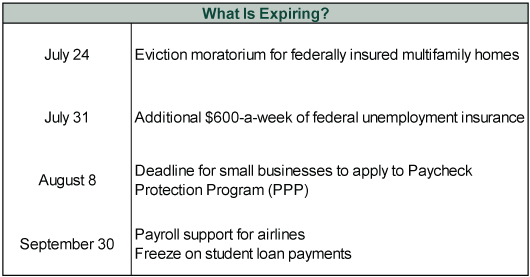

Here are some of the prominent programs set to expire soon.

Exhibit 1: Upcoming Fiscal Cliffs

Source: Bloomberg, as of 7/20/2020.

Don’t get us wrong. The CARES Act likely did provide a lifeline for many households and businesses whose livelihoods were impacted by COVID-driven lockdowns. We don’t dismiss the hardship people who remain forced out of work by lingering or renewed closures will face if the extra assistance ceases, and we are concerned for their near-term financial outlooks. But for investors, we think it is vital to set these emotions aside. To size up how stocks will likely see this, you have to assess the situation from markets’ point of view.

Though some pundits argue markets haven’t considered the potential fallout if these programs expire, we believe stocks are forward-looking and focus primarily on the next 3 – 30 months. Headlines may have started warning about upcoming deadlines recently, but these dates didn’t sneak up on anyone—they were in the initial legislation, making them known to stocks from the start. There is heavy focus daily on fiscal responses to the coronavirus—whether more is yet to come, what may be in a new package, how the original ones worked. Today’s stock prices likely reflect all the discussion and opinions—including fearful forecasts—surrounding these closely followed fiscal cliffs. We think this saps the expirations’ negative surprise potential, limiting their ability to roil markets.

Of course, a major if here is if these programs don’t get extended. Congress has a long history of kicking the can down the road at the last minute. For much of 2012, headlines fretted over the original fiscal cliff—a series of policies including spending cuts (e.g., the Budget Control Act) and tax increases (e.g., expiration of the 2001 and 2003 “Bush tax cuts”) slated for that yearend. Some thought the fiscal tightening could cause a recession unless politicians took action. Though recession fears always seemed overwrought, in our view, Congress eventually compromised on New Year’s Day 2013. Washington has used similar tactics with the debt ceiling, with both parties using the issue as a bargaining chip in recent years. But despite copious handwringing, Congress has either raised or extended the debt limit over 100 times since 1917. Brinkmanship and late-stage bargaineering are among politicians’ favorite pastimes.

While we can’t (and won’t) predict politicians’ actions, it wouldn’t shock if they extended various CARES Act programs either in part or in full. They have already done this with the Paycheck Protection Program (PPP). In June, Congress lengthened the period in which small businesses had to use PPP funds from 8 to 24 weeks (or the end of the year, whichever comes first).[i] With Congress’s summer recess around the corner, many lawmakers will want something to show their constituents—especially if they are seeking re-election this November.

Beyond this, the fear the economy can recover only with government support is common following bear markets, in our view. In July 2009—the beginning of the 2009 – 2020 US expansion—politicians and advisers argued President Obama’s $787 billion stimulus package was “a bit too small” and future efforts were likely necessary.[ii] Those concerns persisted for a while after growth returned. The Bush Administration pushed for a second stimulus package in response to the 2001 recession, and many Americans agreed it was necessary.[iii] Those measures—the second of the “Bush tax cuts”—didn’t become law until May 2003, yet the recession was long over by then.

Government spending can help speed a recovery (and we think it likely has helped many businesses and individuals this year), but a fiscal response isn’t essential for a recovery and bull market. In the eurozone, for example, many countries pursued tax hikes and spending cuts during the 2011 – 2013 recession. Yet growth returned in mid-2013—and a eurozone bull market began a year before the recession ended.

While we understand where the fear over expiring benefits is coming from and can certainly sympathize, we would caution investors against applying that to stocks. Fears that expiring CARES programs will lead to even worse economic troubles illustrate ongoing dour sentiment—evidence of the Pessimism of Disbelief, in our view. Though it may seem counterintuitive, that strengthens our view that we are in a new bull market.

[i] “Senate Passes Changes to Small Business PPP Loan Program,” Erik Wasson, Laura Litvan, and Mark Niquette, Bloomberg, June 3, 2020.

[ii] “Doubts About Obama’s Economic Recovery Plan Rise Along With Unemployment,” Edmund L. Andrews, The New York Times, July 8, 2009.

[iii] “Bush Pushes for Economic Stimulus Package,” Staff, CNN, January 8, 2002 and “Americans Are Divided on Whether Economic Stimulus Is Needed,” Lydia Saad, Gallup, December 20, 2001.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today