Personal Wealth Management / Market Analysis

Don’t Fear a Potential 2019 Earnings Recession

Slowing—and even contracting—earnings don’t necessarily spell doom for stocks.

While stocks have rebounded since 2018’s tough close, financial media continue digging for reasons markets may struggle this year. The latest, a returning ghost from years past: the scary-sounding “earnings recession.”[i] Some analysts are starting to project contracting earnings in 2019’s first half—and a couple even think negativity will persist the whole year[ii]—but in our view, this is a false fear. Earnings forecasts aren’t ironclad, and even if these forecasts end up correct, stocks can fare fine during periods of weaker or even contracting earnings.

Q4 2018 earnings season is wrapping up, with 447 S&P 500 companies reporting 13.1% y/y growth—capping a full year of double-digit earnings growth.[iii] But this seemingly good news doesn’t inspire much cheer. Many credit the 2017 corporate tax cuts for the eye-popping profits—some attribute half of earnings growth to tax reform—and see it as a fleeting sugar high masking weak fundamentals. We will concede this statement is perhaps 40% correct. While we think tax cuts’ overall economic and market impact is often overstated, many US corporations did enjoy a one-time earnings boost from the change—simple math. However, it wasn’t earnings growth’s only driver. Q4 revenues are also up 6.6% y/y, and current estimates peg 8.8% growth for the full year.[iv] Tax changes don’t impact revenue math, making this growth a nice, underappreciated sign of Corporate America’s health.

The tax boost’s falling out of the math lowered earnings expectations for 2019. Those estimates have only grown more pessimistic in recent weeks. At 2019’s outset, Q1 earnings were expected to grow 2.9% y/y.[v] Those estimates have now flipped negative to -2.7% y/y, as some companies lowered guidance.[vi] Some analysts think companies may slash forecasts further given headwinds like global trade tensions and slowing economic growth. The possibility of two straight quarters of falling earnings has fueled those “earnings recession” headlines.

Contracting earnings forecasts sound bad for stocks, but this thesis has holes. For one, earnings estimates aren’t perfect. Companies tend to nudge expectations lower regardless of economic conditions. Businesses want to paint themselves in the best light, and underpromising and overdelivering is an easy way to do so. Moreover, it is normal for consensus estimates to fall in the run-up to earnings season. It is also normal for firms to beat those lowballed estimates more often than not. Both have happened repeatedly during this bull market. Sequential quarterly earnings drops aren’t a foregone conclusion.

Even if earnings do take an extended tumble, history illustrates contracting earnings needn’t derail bull markets. See 2015 – 2016’s earnings recession. Rather than broad corporate weakness, the Energy sector—roiled by oil prices’ plunge from mid-2014 – early 2016—dragged earnings into the red. Though this earnings recession happened alongside a market correction (a sharp, sentiment-driven market downturn of -10% to roughly -20%), coincidence isn’t causality. Energy-related concerns could have impacted sentiment, but other stories—namely China hard-landing and global recession fears—figured more prominently at that time.

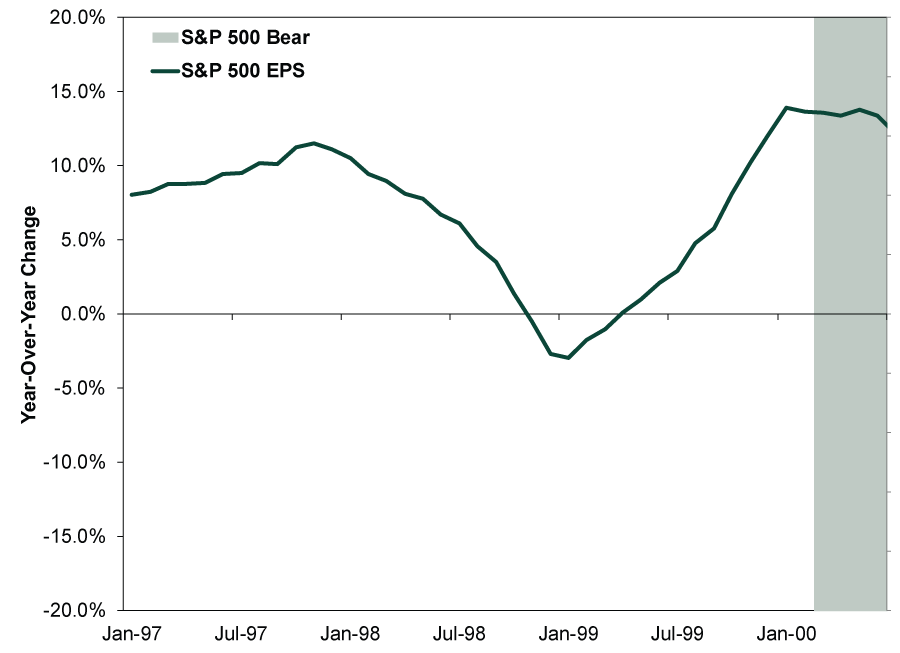

Earnings growth also slowed during the 1990s bull market’s second half—and even contracted for several months. That didn’t make it a bad time to own stocks.

Exhibit 1: S&P 500 Earnings per Share, 1997 – 2000

Source: FactSet, as of 2/27/2019. S&P 500 EPS, monthly, 1/31/1997 – 6/30/2000.

Slower earnings don’t automatically mean weaker market returns ahead, either. It is normal for earnings to slow as a bull market matures and year-over-year comparisons become harder to beat. Maintaining eye-popping growth for years and years would be unrealistic. Consider when earnings growth is typically fastest: at the start of an expansion. Coming out of a recession, companies have cut costs and are lean and mean, so even some modest sales growth makes for big profit margins. Later in the business cycle, revenue growth—rather than cost-cutting—tends to drive earnings. Last year was unusual for featuring a late-cycle cost (tax) cut. Its absence this year is math, not an indication of corporate health. With sales expected to grow 5.2% y/y in Q1,[vii] it looks like any potential earnings drop isn’t tied to flagging demand or economic woes.

Stocks knew the tax cut would fade from the data the moment it was enacted. It is no surprise, and surprises tend to move markets most. Plus, stocks, which look out to the next 3 – 30 months, can see through a quarter or two of expected weaker earnings. Even with weaker expectations for Q1, consensus estimates still expect a positive 2019: Full-year earnings and revenues are expected to grow 4.8% y/y and 4.9%, respectively.[viii] Moreover, in maturing bull markets, investors typically become more willing to pay more for earnings—especially as sentiment improves. This is known as multiple expansion, in which stocks trade at bigger and bigger multiples of earnings. This happened a bit in 2017, but last year’s correction curtailed it. Multiple expansion can last for a while too—a potentially underappreciated bullish force.[i] For the record, we really despise how media distorts the term “recession” by slapping it onto narrow slices of the economy or specific statistics. A recession, by definition, is a broad decline in economic activity. Not a slight downturn in one specific area or stat.

[ii] Source: “An 'earnings recession' has arrived, and the market's not ready for it, Morgan Stanley says,” Thomas Franck, CNBC, 2/11/2019. https://www.cnbc.com/2019/02/11/an-earnings-recession-has-arrived-morgan-stanley-says.html

[iii] Source: FactSet Earnings Insight Report for week ending 2/22/2019.

[iv] Ibid.

[v] Source: FactSet Earnings Insight Report for week ending 1/4/2019.

[vi] Source: FactSet Earnings Insight Report for week ending 2/22/2019.

[vii] Ibid.

[viii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today