Personal Wealth Management / Market Analysis

Draghi, QE and the Perils of Timing Tapers

The ECB's surprise inaction shows the folly of trying to game central bank moves.

Human beings can be pretty inconsistent, often flipping and flopping, contradicting themselves. Frustrating, confusing beasts! Last we checked, central bankers are human beings[i] and it should be no surprise the evidence proves they too are quite inconsistent. For this reason, we'd caution against taking their words as gospel about actions to come-and overthinking bouncy bond yields that occasionally result. Recent statements from ECB head Mario Draghi-and bond-market wiggles many tie to them-are a case-in-point.

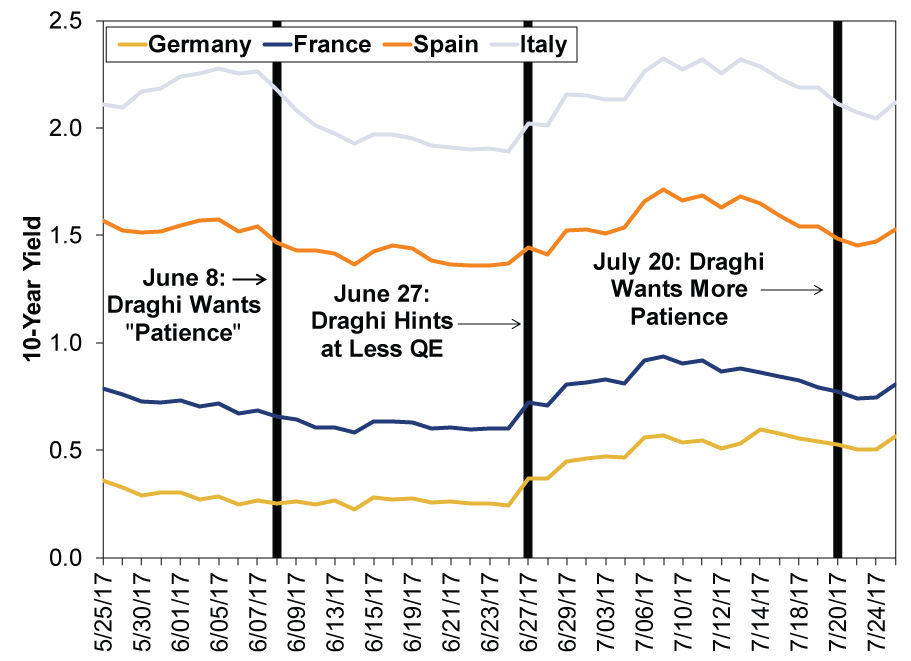

In early June, the ECB's monetary policy statement dropped language alluding to potential further rate cuts, an action many analysts read as Draghi and Co. paving the way for a slowing in bond purchases-a taper, in central-bank-watcher parlance. Yet Draghi noted that "patience" was still warranted as inflation wasn't near the ECB's target, meaning tighter policy wasn't on the horizon. Later in the month, though, Draghi spoke again and took what many interpreted as a more hawkish stance: "As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments -- not in order to tighten the policy stance, but to keep it broadly unchanged." Many analysts saw this as a shift toward tapering soon, with some speculating it would come as early as July or September. Interest rates on 10-year eurozone country bonds rose, with many connecting the move to Draghi's talk. Yet last Thursday, he changed his tune: The ECB held short-term rates and asset purchases steady, and when asked about taper plans, Draghi effectively walked back the earlier comment, claiming it was merely talk about potential talk about maybe tapering.

See what we mean? Inconsistent! But before you wonder what the seemingly contradictory comments mean for policy, consider what it really highlights: Investors gain little from central-bank watching, and adjusting expectations based on coverage leads to dizzying reversals. As the ECB's surprise inaction shows, Draghi's June statements didn't mean what many thought. Or maybe they did, but for whatever reason, the ECB doesn't want you to think he meant it. At least for now.

For all the talk of central bankers as "data dependent," giving an image of impartial, scientific study of numbers and hard figures, they are in reality just humans. Yes, they look at data-but through biased, fallible lenses. Besides, given the size, scope and complexity of major developed economies, there will virtually always be contradictory data. How policymakers weight certain variables is a matter of opinion.

Recent history further shows the folly in overthinking central bankers' words. Consider the evidence globally. In 2012, then-Fed head Ben "the Beard" Bernanke told the world the Fed would consider hiking short-term rates when the US unemployment rate hit 6.5%. The media latched onto the figure, presuming it was a trigger. Within six months, he was walking this comment back and, when the Fed finally hiked in December 2015, unemployment was at 5.0%. In March 2014, his successor Janet Yellen noted the first short-term interest rate hike would come "around six months or that type of thing" after the end of its quantitative easing bond buying. That program ended in October 2014, but again, no hike came until December 2015. That month, analysts took the Fed's dot-plot to mean four rate hikes would come during 2016. We got one.

This isn't a Fed-only phenomenon, either. Bank of England head Mark Carney flipped and flopped so many times during this bull's earlier years that one politician colorfully called him an "unreliable boyfriend." As for Draghi, in November 2016 he told listeners he'd need to see a "sustained convergence of inflation towards a level below, but close to, 2 percent over the medium-term" to support dialing back QE. Analysts took this as surefire evidence the ECB would maintain its program unchanged at the next month's meeting. Yet the ECB slowed the pace of bond buying that month, a de-facto taper (that they assured us was not a taper!) despite no material inflation uptick.

Not only would we recommend not overthinking policymakers' comments, we'd say the same of short term bond market wiggles many tie to them. When Draghi made his June 27 speech seen as a prelude to a taper, yields rose and analysts declared it a tantrum, akin to the (widely overstated) rise in May 2013 when the Fed hinted at tapering. But in reality, major eurozone countries' 10-year yields rose between 0.3 - 0.5 percentage point. Folks extrapolated these moves further, but they soon reversed course. These are short-term wiggles. Sentiment. That's it.

Exhibit 1: Eurozone 10-Year Bond Yields

Source: FactSet, as of 7/25/2017. Germany, France, Italy and Spain 10-year bond yields, 5/25/2017 - 7/24/2017.

Instead of fretting talk and wiggles, we'd recommend analyzing policy through a more time-tested lens: the quantity theory of money. A century of theory and data says higher long rates aren't to be feared if they widen the spread between short-term and long-term rates. That gap is a measure of banks' loan profits-wider spreads encourage lending. This is a big reason why whenever the ECB decides to end QE, it's likely a positive-not a negative. By vacuuming up long-term bonds, the ECB's QE program has suppressed long rates, flattening the yield curve. As the eurozone's present expansion proves, this doesn't necessarily crush growth, but it's a headwind nonetheless. The US and UK experiences demonstrate ending QE is an economic positive.

We expect the same in the eurozone. After the ECB's December announcement it would cut the pace of bond purchases, national yield curves steepened, lending improved and expansionary Purchasing Managers' Indexes indicated even broader growth. So while we won't claim any insight into the ECB's taper timeline-and we caution investors against getting caught up in the speculation-we're rooting for sooner rather than later.

[i] We are like 99% sure they are human beings, at least.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today