Personal Wealth Management / Market Analysis

Flat Yield Curve Fears Yield Little Fruit

While the yield curve is an important leading indicator, it isn’t a timing tool.

Last year’s yield curve fears centered on some segments of the yield curve we find arbitrary and meaningless—the 10-year minus 2-year, 5-year minus 2-year and 5-year minus 3-year spreads. Because banks generally don’t fund themselves at 2 or 3-year rates, none of these gauges correspond to banks’ business models or propensity to lend. But this year, commentary has started shifting to a more meaningful yield spread—the 10-year minus 3-month—which is near its flattest point of this economic expansion. The question on folks’ minds: Will it invert soon, and if so, do dark times lie immediately ahead?

The yield curve is one of the most telling economic indicators on the planet. It influences and predicts loan growth, because banks borrow at short-term interest rates and lend at long-term rates. If it is positive, with long rates above short, then lending is profitable, incentivizing banks to funnel capital to businesses and households. If it is inverted, with short rates above long rates, then banks’ funding costs exceed potential loan revenues, rendering lending unprofitable. If the yield curve stays inverted for long enough, it can cause credit to freeze, starving businesses of the capital they need to expand.

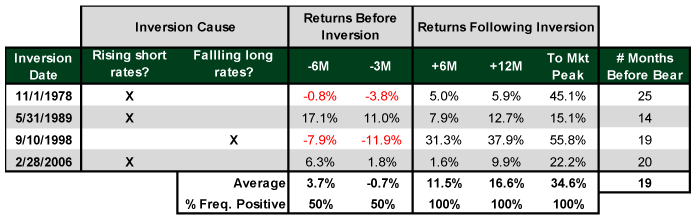

Yet none of this means the yield curve is a timing tool—especially not any single country’s yield curve, even a country as big as America. While an inverted yield curve has preceded every US recession in modern history, there is usually a lag between inversion and recession. As Exhibit 1 shows, there were even four times where the yield curve inverted without a bear market beginning within the next 12 months. On these occasions, selling stocks when the yield curve inverted would have led to missing out on some occasionally big returns.

Exhibit 1: Returns Before and After US 10-Year Minus 3-Month Yield Curve Inversions Without a Bear Market or Recession in the Next 12 Months

Source: Global Financial Data, Inc., FactSet and St. Louis Federal Reserve, as of 1/4/2019. S&P 500 price returns, 10-year US Treasury yield and 3-month T-bill yield, 1/1/1945 – 8/28/2007.

It is impossible to predict the amount of time that will elapse between a yield curve inversion and beginning of a bear market. A lot depends on how central banks respond to the inversion, as well as what the global yield curve is doing. In 2006, for example, the global yield curve remained positive long after the US curve inverted, helping keep the economy and stocks humming for over a year and a half. Or, the Fed could cut rates, making the inversion short, as was the case in 1998.

Perversely, this uncertainty is what can lead to big returns after the yield curve inverts. Inversions can make investors fearful of imminent recession, and that fear gets baked into prices. If recession doesn’t happen, that can be a bullish positive surprise.

Typically, the yield curve signals trouble most of all when few see it or most dismiss it. Not when everyone obsesses over different flavors of it flattening. That said, it is always sensible, in our view, to monitor the yield curve. Especially now, given flatter does mean the risk of a monetary policy error is higher. But don’t overreact out of haste. Particularly now, with the global yield curve still steeper than the US’s.If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today