Personal Wealth Management / Economics

Quick Hit: US Business Investment's Sad Q3

Falling business investment isn’t wonderful, but it doesn’t always mean recession.

US GDP growth slowed to 1.9% annualized in Q3, the second straight deceleration.[i] Gaining most eyeballs? Business investment’s -3.0% decline, its second drop in a row.[ii] This prompted a slew of headlines arguing American consumers are the only entities propping up growth—which didn’t inspire much confidence, considering consumer spending growth slowed from Q2’s 4.6% to 2.9%.[iii] We think all the handwringing is a bit overdone. While business investment does tend to be a key swing factor for America’s economy, the occasional drop isn’t unusual. Nor are business investment’s wobbles predictive, so we think investors are best off not reacting to the news.

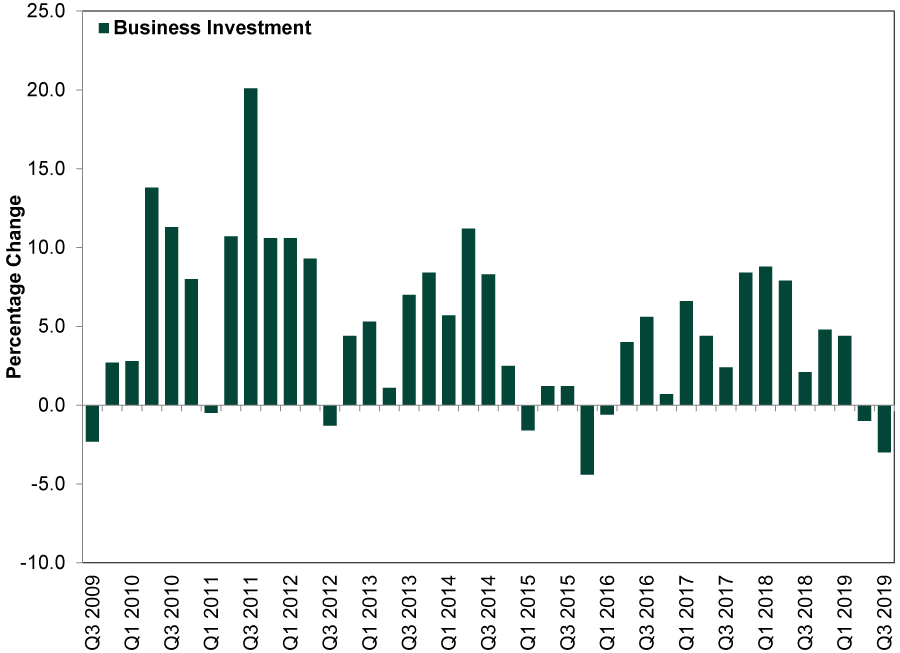

For some perspective, Exhibit 1 shows business investment’s growth rates since this expansion began in Q3 2009. You will see this isn’t the first time it has fallen. It isn’t even the first sequential drop—that honor goes to the drops in Q4 2015 and Q1 2016. That is also when the US and global economies were in a mid-cycle slowdown much like the present. Recession didn’t strike then. Rather, the US and global economy reaccelerated, and stocks busted out of a frustrating flat stretch. Not that the past is predictive! But, you know, interesting.

Exhibit 1: Business Investment Sometimes Wobbles

Source: Bureau of Economic Analysis (BEA), as of 10/30/2019. Percentage change in real non-residential fixed investment, seasonally adjusted annual rate, Q3 2009 – Q3 2019.

Lastly, note that business investment wasn’t uniformly weak—much like 2015 – 2016. Back then, declining investment in wells tied to faltering oil prices zapped investment in structures (e.g., offices, mines, wells, warehouses, factories, etc.). This quarter, investment in structures suffered its second double-digit drop in a row—and drops in mine and well investment (-29.3% annualized in Q3) played a big role in both quarters’ dips.[iv] This is likely due to small shale drillers’ slowing growth amid range-bound oil prices and higher financing costs. The decline in equipment investment was much milder and isn’t part of a trend. It appears a sharp uptick in Q2 2019 computing equipment investment reversed.[v] This is a historically volatile component, so seeing big swings isn’t a shock.

Meanwhile, investment in intellectual property products accelerated, growing 6.6% annualized.[vi] The discrepancy among these components also echoes the 2015 – 2016 slowdown. Again, just an interesting observation! But we do think it is telling that businesses aren’t getting lean and mean across the board. In a recession, that is typically their aim.

[i] Source: BEA, as of 10/30/2019. Real GDP, seasonally adjusted annual growth rate, Q3 2019.

[ii] Ibid. Real non-residential fixed investment, seasonally adjusted annual growth rate, Q3 2019.

[iii] Ibid. Real personal consumption expenditures, seasonally adjusted annual growth rate, Q2 – Q3 2019.

[iv] Ibid. Real investment in mining exploration, shafts and wells, seasonally adjusted annual growth rate, Q3 2019.

[v] Ibid. Real investment in computers and peripheral equipment, seasonally adjusted annual growth rate, Q3 2019.

[vi] Ibid. Real investment in intellectual property products, seasonally adjusted annual growth rate, Q3 2019

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today