Personal Wealth Management / Politics

The Infrastructure Bill’s Embedded Taxes’ Tiny and Temporary Effect on Prices

A lesson in how to assess downstream consequences.

Editors’ Note: MarketMinder favors no political party or any politician. We assess political and legislative developments solely for their potential effect on markets and the economy.

After the House passed the infrastructure bill and sent it to President Joe Biden to sign last Friday, most coverage—including ours—focused on the spending side of the ledger. The bill’s tax provisions didn’t get much attention, which we find both sensible and telling. Sensible because the tax changes are minor and probably won’t dent corporate earnings a ton or discourage new investments. Telling because people often ignore top-line income and corporate tax changes, presuming something so niche won’t have broad reach. Yet as we all know, nothing in life is certain but death and taxes—and corporations’ knack for passing on taxes to consumers. Understanding how this works now can help reduce surprise power when you inevitably start noticing the (likely small) impact. More broadly, assessing second- and third-order consequences is one of the most beneficial things investors can do when assessing policies’ impact, and we are happy to show how this is done.

On the surface, the bill’s tax changes appear to have limited reach. One seeks to curb tax evasion by requiring brokers to report all of their customers’ cryptocurrency transactions, with the definition of “broker” expanded to include cryptocurrency exchanges. If you don’t own crypto, that has nothing to do with you. The other change is the reinstatement and modification of Superfund excise taxes on a range of petrochemicals—taxes that were born in the 1980s and lapsed in the mid-1990s. This would tax production and importation of a broad range of chemicals. Perhaps that still sounds distant, as many of which are feedstock for plastics and a host of everyday goods from shoe soles to household cleaners. The list also includes nickel and cobalt, which feature in rechargeable batteries. Also, zinc—used in all of your home’s brass and bronze fixtures (as well as galvanized steel and iron).

The tax rates, which range from $0.48 per ton (nitric acid) to $9.74 per ton (on 10 chemicals like benzene and butane), aren’t astronomical. They are all doubled from the 1980s – 1990s tax rates, but a lot of these products have increased in price over the past 25-plus years. If the taxes weren’t prohibitive then, we doubt they will be now. At the same time, it seems fair to assume they will eventually show up in your shopping bills, as companies have strong pricing power right now and will almost surely pass them to consumers—just like they pass on tariffs and other targeted taxes. That limits the taxes’ effect on stocks, as it means companies can preserve earnings and profit margins. But it also adds another, albeit very small and temporary, inflation driver in the short term.

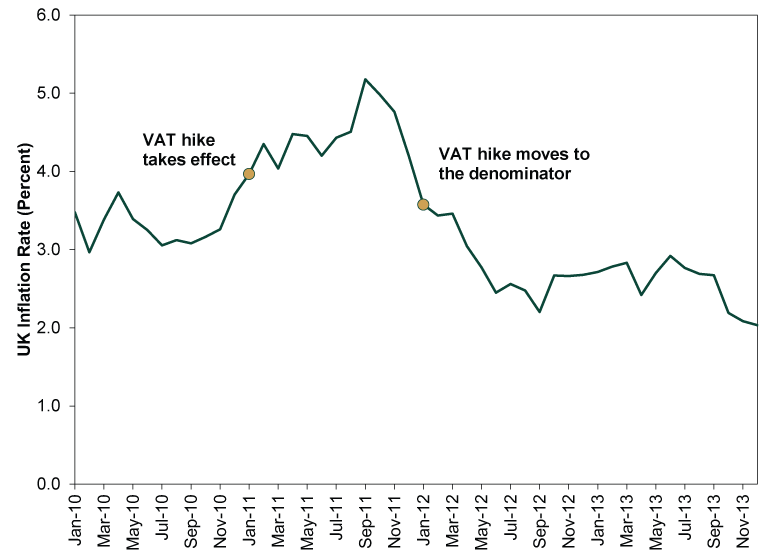

To see how these taxes actually affect inflation—in a case with a much more meaningful tax increase—consider UK inflation in 2011. The UK, like most of Europe, uses a value-added tax (VAT) instead of sales tax. It is a charge that companies pay at every step of the production chain but ultimately gets embedded into the final good’s prices, sticking consumers with the bill. In January 2011, the UK raised the standard VAT from 17.5% to 20%. As Exhibit 1 shows, Consumer Price Index (CPI) inflation leapt accordingly and stayed elevated all year. But in 2012, once the VAT hike moved from the numerator of the year-over-year rate to the denominator, the inflation rate slowed sharply. By 2013’s end, CPI was growing much more slowly, and the UK would enjoy slow inflation for years.

Exhibit 1: Tax Hikes’ Inflation Impact Is Temporary

Source: FactSet, as of 11/12/2021. UK Consumer Price Index Year-Over-Year Inflation Rate, January 2010 – December 2013.

You can apply this same logic to the supply chain crunch-induced price increases presently elevating the US inflation rate. We often talk of those working their way through the economy and eventually losing their bite—this is exactly what we mean. Exhibit 1 is the very image of “transitory” inflation—a one-time or short-term price increase that eventually exits the inflation math. UK VAT didn’t fall in 2012. The standard rate remains at 20%. But the economy adapted. Households dealt with higher costs and rebudgeted as needed.

There are always small headwinds and cost pressures for businesses and households alike. They aren’t pleasant, ever, but they generally don’t forestall growth. But if you would like to chastise your congressperson for sneaking a consumer tax hike past the country, have at it. Happy Friday.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today