Personal Wealth Management / Economics

What Investors Can Glean From Q4’s GDP Slowdowns

Q4 GDP slowdowns—and even some contractions—surprised few.

One month into 2021 and several major economies have released Q4 2020 GDP readings, which followed huge Q3 jumps to results ranging from slowing growth to an actual return to contraction. Though these data are old hat for forward-looking stocks, the numbers confirm several trends. Perhaps the biggest such trend: The broad reaction to the data is largely rational—a sign of rising optimism, in our view, and worth noting for investors.

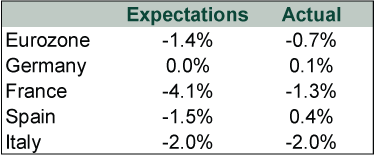

After the US released Q4 GDP—which slowed to 4.0% annualized growth—the eurozone followed suit. Prior to the release, expectations were low, as targeted lockdowns returned across the Continent in November and December. Those projections were rational, as eurozone GDP contracted, but the numbers also largely beat expectations—signaling some economic resiliency. Germany and Spain even eked out Q4 growth.

Exhibit 1: Q4 Eurozone GDP

Source: FactSet, as of 2/3/2021. Q4 GDP quarter-over-quarter percentage change.

These preliminary readings are subject to revision, and subsequent releases will provide more color. But the data, even the contractionary readings, surprised basically no one—and surprises sway stocks most, in our view. So it was no shock that stocks didn’t react negatively.

Among major Emerging Markets (EM), China’s 6.5% y/y Q4 GDP growth beat expectations of 6.0%.[i] Many pundits focused on the country’s full-year growth of 2.3%—the only major economy to expand in 2020. While that tidbit may be helpful on GDP Trivia Night,[ii] the distinction doesn’t matter to stocks.

Taiwan was the rare country that didn’t impose a national COVID lockdown, and the numbers show the economic benefits: Q4 GDP rose 4.9% y/y, the fourth straight quarter of year-over-year growth.[iii] The pandemic also stoked global demand for tech and electronics, driving a semiconductor shortage—a boon for both Taiwan and South Korea (Q4 GDP: 1.1% q/q, -1.4% y/y), two integral hubs in the global tech supply chain.[iv] In our view, the strong demand for electronic goods illustrates the fundamentals supporting the global Tech sector.

Other EM GDPs—e.g., Mexico (3.1% q/q, -4.6% y/y) and the Philippines (5.6% q/q, -8.3% y/y) mirrored the Q4 resiliency seen in America and the eurozone.[v] Similar to developed world economies, economists think EM recoveries largely depend on a return to normalcy—a vaccinated world in which households and businesses operate as they did pre-pandemic. We think stocks are looking ahead to that world now.

In our view, the past 12 months illustrate how stocks function as leading economic indicators. After a calm start to 2020, global equities plunged into a bear market in February – March. Stocks suddenly shifted focus to the very near term to incorporate the lockdown-driven severe economic contraction. Then markets looked out further—to eventual reopenings—as a new global bull market began in late March—right as official economic data began confirming contraction. Today, we think stocks are fathoming a time when vaccine distribution is more widespread and economic normalcy gradually returns. We think it would take a new shock to knock stocks off this view and have them refocus sooner. The lockdowns that drove slower growth and contraction in Q4 were no such thing, and increasingly optimistic investors appreciated that.

As for China, we think it previews what growth will look like in a vaccinated world. Economic data popped following the country’s reopening, and a state-driven credit boom aided the recovery. As in the West, data suggest slowing ahead. Credit growth already seems to have crested, and officials have voiced their intentions to rein shadow lenders back in. Prior to the pandemic, data from 2018 and 2019 show the government’s shadow banking crackdown led to slower GDP growth rates. China’s leadership has signaled its comfort with slower growth so long as it doesn’t imperil its top priority: social stability.

Developed world recoveries won’t look exactly like China’s since the US, UK and eurozone don’t have command economies. However, we anticipate the general course repeating here again. We have already seen growth surge on reopenings once, last summer. We suspect there will be another pop, to a much smaller extent, when current restrictions lift. But the pop should be fleeting. Many data points have already returned close to pre-pandemic levels—in some cases, like goods consumption, beyond them. In terms of magnitude and pace, this highlights a key point: We think most of the recovery is already behind us.

Often, investors think slower growth is bad for stocks. We think that is overrated. Today, slower growth would signal some economic normalcy returning—and that is a plus. Besides, what matters more than GDP growth rates is how sentiment aligns with that reality. Based on largely rational mainstream reaction to the latest GDP numbers, sentiment seems broadly optimistic now—and, with the economy set to return toward normalcy, that would be a great backdrop for stocks.

[i] Source: FactSet, as of 2/3/2021.

[ii] This would be the most boring episode of Jeopardy! of all time. (RIP Alex Trebek.)

[iii] See note i.

[iv] Ibid.

[v] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today