Investing in Gold: The Right Choice for Your Portfolio?

Gold’s Market Myths

There is a long-standing market narrative that gold is a robust and time-tested safe haven for investors. Proponents argue that gold can hedge your portfolio against market declines, steady it during market volatility or protect your purchasing power from the erosive effects of inflation.

Gold is available to investors in one of many investable forms: physical gold, gold certificates, gold bullion, gold-based exchange-traded funds (ETFs), mutual funds invested in mining companies, gold futures or other gold derivatives. But gold’s history and the common rationales for investing in it often don’t stand up to a fact check.

Myth #1: Gold as a Hedge Against Market Declines

Some investors believe gold prices are negatively correlated with stocks. In other words, they think the price of gold rises when stock prices fall, and vice versa. In times of economic turmoil, many investors want to diversify their portfolio with gold-related investments to hedge their portfolio or protect it against an expected decline in stock prices.

While it is true that gold does have times of boom and bust, those periods don’t always correlate with the opposite movement of stocks. Consider that since 1974, world stocks declined in 11 calendar years. Gold rose in five of those years, but fell in the other six.1 In other words, there is not a reliable inverse relationship that would make gold an efficient hedge for stocks. So, if you’re looking to invest in gold to help protect your portfolio during stock market declines, you may be disappointed by the results.

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Myth #2: Gold as a Volatility Hedge

A similar belief is that gold can hedge against volatility. Because it has historically backed government-issued currencies, gold is widely considered a "store of value." You can touch it, hold it or bury it in the backyard. That makes it seem like a hard form of wealth. Thus, the thinking goes, when times get particularly bumpy, the subsequent uncertainty that will rock stocks won't affect gold.

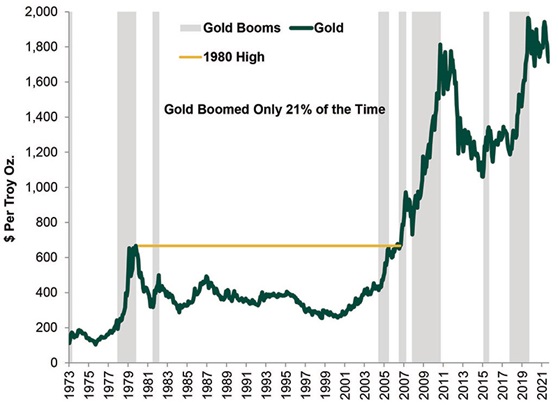

But observe Exhibit 1, which shows gold’s price movements since 1973. Gold’s performance has not been a smooth or steady climb to its relatively low returns. The bulk of its gains have come in just four stretches—bursts of positive returns bracketed by long flat-to-down periods. Missing any of these booms would severely affect returns.

Further, after the 1980 high, it took over 25 years to get back to that pre-drop level.

Exhibit 1: Gold's Inconsistent Price History

Source: FactSet, as of 9/19/2022. Gold spot price, monthly, 11/30/1973 – 8/31/2022.

Gold has had times of relatively stable price performance, but also periods of volatile movement. Since 1933, gold-spot-price returns have a standard deviation (a measure of risk) of 16.1% in comparison to the MSCI World Index’s 13.6%—without any outperformance that would justify the increased risk.2

Volatility isn’t inherently bad. Higher volatility often accompanies higher returns. Not so with gold, though. In our view, the explanation for gold’s high volatility lies in its supply and demand drivers. Supply tends to rise at a fairly slow and consistent rate over time, considering that essentially every ounce of gold ever mined still exists. Demand, meanwhile, tends to be highly volatile.

Since gold has few industrial uses, demand typically fluctuates with investor sentiment. When folks fear big market declines, inflation, a falling dollar or one of the many other things against which gold purports to hedge, they often rapidly bid up the shiny metal for a time. This means it moves in psychologically driven—often massive—short-term price swings, which are exceedingly inconsistent and difficult to time.

Myth #3: Gold as an Inflation Hedge

A third long-held tenet claims gold is a great hedge against inflation. History doesn’t support this. For example, from December 1986 to October 1990, the US consumer price index (CPI), a common measurement of inflation, accelerated from 1.2% year-over-year to 6.4%, while gold fell 2.9%.3 There were periods where gold seemed to hedge well, but as CPI continued to accelerate in 1989 and 1990, gold fell more than 20%, working as an inflation hedge only about a third of the time4—a fleeting record, in our view.

Assessing Gold’s Long-Term Returns

Compared with equities, gold has had subpar long-term returns and higher short-term volatility.

Gold began trading freely in 1973 after the US abandoned the gold standard. From December 1973 through April 2024, US equities returned 11.3%, annualized.5 Over that same time period, gold returned 6.4% annualized.6

In fact, not only has gold performed much worse than equities, it also underperformed US Treasurys, but with more volatility, as Exhibit 2 details.

Exhibit 2: Growth of $1 in Stocks, Bonds and Gold (November 1973-April 2025)

Source: Finaeon, Inc. as of 5/15/2025. US 10-Year Government Bond Index, S&P 500 Total Return Index and Gold Bullion Price fom 11/30/1973 – 4/30/2025.

Gold Is a Commodity, Not a Store of Value

In our view, the reason for this underperformance is that gold, just like silver or any other precious metal, is a commodity, not a company. Firms can innovate, evolve, respond to market incentives and grow over time. Commodities have no such fundamental connection to economic growth and progress.

Gold doesn't generate earnings or pay interest or dividends. It is a physical product whose prices are driven by supply and demand, not by an intrinsic, fundamental value. In fact, many other metals have more far-reaching industrial and commercial use.

Further, gold doesn't preserve capital. Since gold is tangible—and stocks aren't—it seems like it will hold its value indefinitely. It doesn't tarnish or degrade. A gold bar will still be a gold bar in a thousand years. However, like any asset, that bar is worth only what someone is willing to pay for it. Gold's history since the end of the gold standard highlights the metal's spectacular—and limited—boom and bust periods.

Something that swings so wildly is not a stable store of value. An asset that truly preserves capital won't lose value at all. Its current worth should be the same in a month, a year, a decade and beyond. That certainly isn't the case with gold.

Gold Investment Probably Won’t Benefit Your Portfolio

While it is true that gold prices (and those of other commodities at times) can have periods of outperformance, do you have the ability to time the market to take advantage of those price movements? Would you have known to avoid gold during the 1990s, but to jump in and invest before the rise in the mid-2000s? Would you have gotten out of gold before the drop in the 2010s?

Other asset classes also experience volatility that makes market timing difficult or impossible. But, stocks give investors more significant long-term returns in exchange for tolerating that short-term volatility. If you can’t time the gold market, and gold doesn’t provide better long-term returns, how is investing in gold a safer bet than investing in stocks or bonds?

Ultimately, investors interested in long-term success would be better served, in our view, by viewing gold for what it really is: a commodity, a shiny metal offering limited inflation or volatility protection and low prospects of growth and return.

1Source: FactSet, as of 9/19/2022. MSCI World Index Total Return and LBMA Gold Price Return, annually, 12/31/1973 – 12/31/2021. Presented in US dollars.

2 Source: FactSet and Global Financial Data, as of 6/2/2022. MSCI World Index Return with net dividends and gold spot price returns (London AM fixing, USD), monthly, 12/31/1939 – 5/31/2022. Volatility measured by standard deviation, defined as the amount of variation in returns.

3 Source: FactSet and Federal Reserve Bank of St. Louis, as of 10/27/2021. Gold price per ounce, 12/31/1986 – 10/31/1990, and CPI, December 1986 – October 1990.

4 Source: FactSet and Federal Reserve Bank of St. Louis, as of 10/27/2021. Gold price per ounce, 12/14/1987 – 10/31/1990.

5 Source: Global Financial Data, Inc., as of 4/8/2024. S&P 500 Total Return Index from 11/30/1973 – 3/31/2024.

6 Source: Global Financial Data, Inc., as of 4/8/2024. Gold Bullion Price from 11/30/1973 – 3/31/2024.

Insights & Media

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today