Personal Wealth Management / Book Reviews

The Psychology of Money

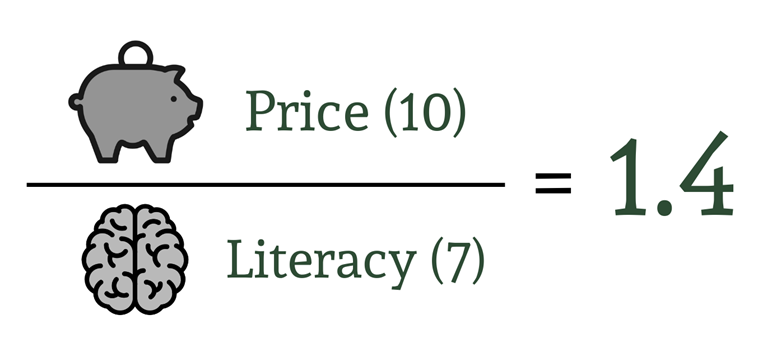

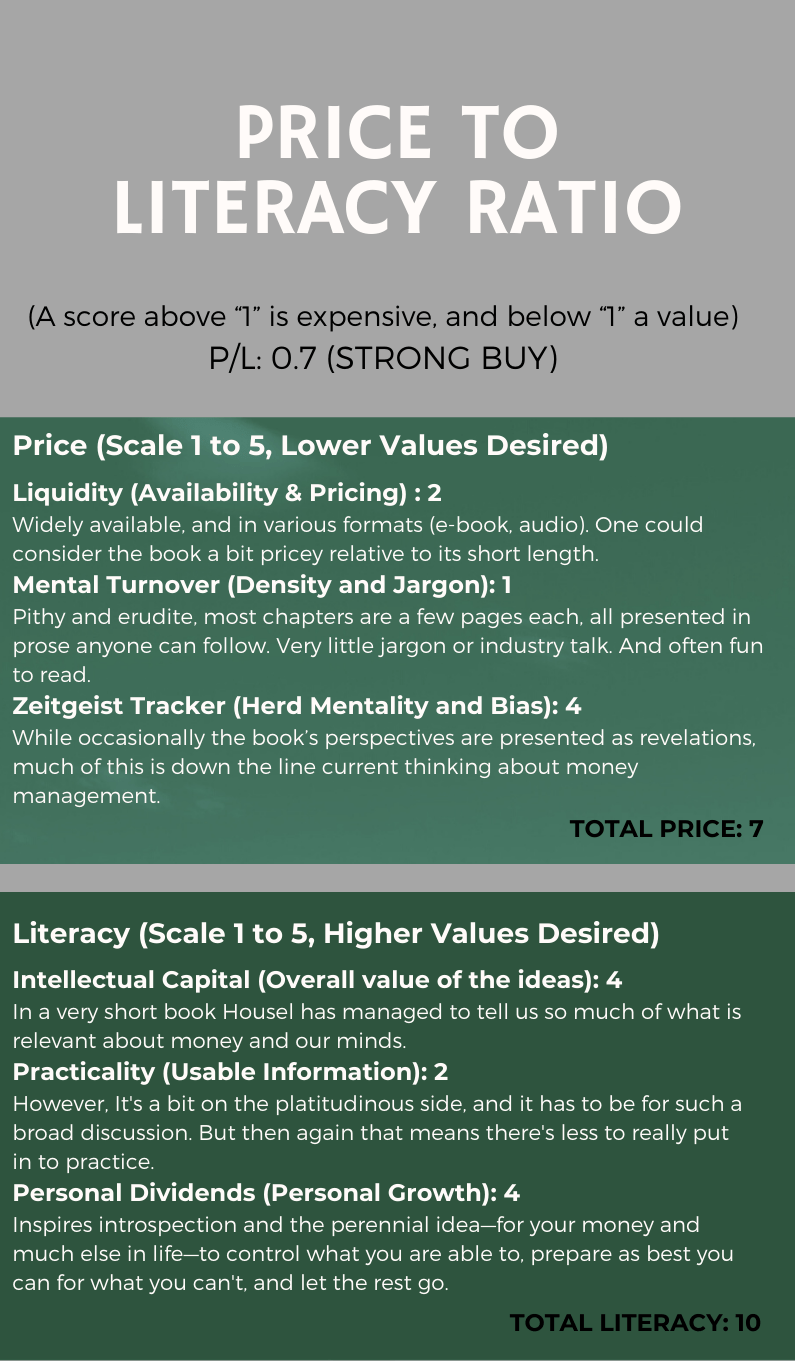

Morgan Housel has written a very good book about investing. It's not really a psychology book per se, it's more like a wisdom book for the average investor. At that, it succeeds.

The book is full of traditional investing wisdom of the sort that says take control of what you can, and don't worry over what you can't. We are admonished not to strive toward "rationality", instead to be "reasonable". Which reminds of Meir Statman's "people are normal" idea (listen to our podcast with him here!), positing that pure rationality among our imperfect selves thrown into an imperfect and chaotic world, is a fantasy, let alone a recipe for unhappiness.

All that is fine and well. I can see brokers across the land gifting this book to clients over the holidays, earmarked to their favorite pithy insight.

Housel really got me going though in his take on what volatility actually is: a fee! This is a brilliant insight and one every long term investor should think through. To get the long term return of the stock market, everyone must pay: you can do that with emotion, or with money. Sadly, many choose the latter—hedging when they don’t need to (an explicit cost that erodes long term returns), or jumping in and out of the market when they get jittery only to get back in when it seems “safe” (an often huge opportunity cost). The alternative is to stomach it, grind through the constant uncertainty of “now” in all its apparent peril, and do the disciplined work of keeping your eye on the longer goal. Both are forms of payment—explicit or emotional—you need to know yourself well enough to know which is right for you. (This year has surely revealed folks’ true risk preferences like no other, so take note of how you reacted and be honest with yourself.)

There are, of course, things to quibble with. Housel describes the process of achieving investing goals chiefly as “survival”. While the observation that becoming wealthy and staying wealthy are two different skillsets is true enough, I believe the mindset of “survival” unfortunately promotes a psychology of hedging too often and frightening too easily. What matters most is setting a realistic long-term goal and having the discipline to stick with it in order to achieve the power of compounding. Time is the greatest asset, of course—what gives compounding its potency. Housel is dead on here in describing the importance of longevity to investing success—most people don't do anything for all that long, not irrationally per se, but because people evolve and their tastes, goals, and interests change. With investing, the key is to stay at it and stay with it. Be consistent, be boring, don’t change much or often. Make compounding work for you.

Housel rails against using experience as a guide for investing, and that’s tragic. There should never have been a debate about "data driven" versus" experiential" investing in the first place. It's a false dichotomy—both are sides of the same coin. You have no one but yourself in the end to make decisions—you have no choice but to cultivate your specific personal experience in the context of the wider, objective world. To ignore yourself as a pathway toward better decisions is a bad idea and leads to following data blindly. Good judgement is the delicate, contextual, often artful, tension between data and experience. Of course experience can breed overconfidence and errors, so can blindly following data—often far worse, in fact.

And so, what a lot of this stuff argues for, unwittingly, is to have a trusted advisor to help you with the plan and with navigating the scariest times. It's great if you can find a genius who frequently beats the market, but the real value is to have someone who is dispassionate (or at least less passionate) about the vicissitudes of the moment to help you make a handful of key decisions better than you otherwise would. Those key moments usually have to do with the fear or euphoria of the short term wanting to derail the basic discipline of sticking to long term goals.

The psychology of money will always be relevant because the archetypes of our collective psychology, manifesting over and again in the cycles of bulls and bears, are the constants in a world of accelerating change. Know yourself at least as well as you know the market.

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Insights & Media

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today