Personal Wealth Management / Market Analysis

The Bull Market Doesn’t Depend on Rate Cuts

Don’t buy the narrative that rate cut hopes are the only thing propping stocks up.

Are cuts coming? Seemingly with every emerging data point on inflation (economy-wide price increases), jobs and more, commentators we follow launch a white-knuckled debate over what it means for potential rate cuts from monetary authorities. It all fits a common narrative to us: That this bull market (broad, extended equity ascent) depends on monetary policy, with global stocks’ recent rally riding on the notion cuts are approaching, with only the timing unclear.[i] But, in our view, this thinking overrates cuts’ impact—markets don’t hinge on (unpredictable) monetary policy. We think the economy is more resilient than most headlines we read suggest—and that seems bullish for stocks.

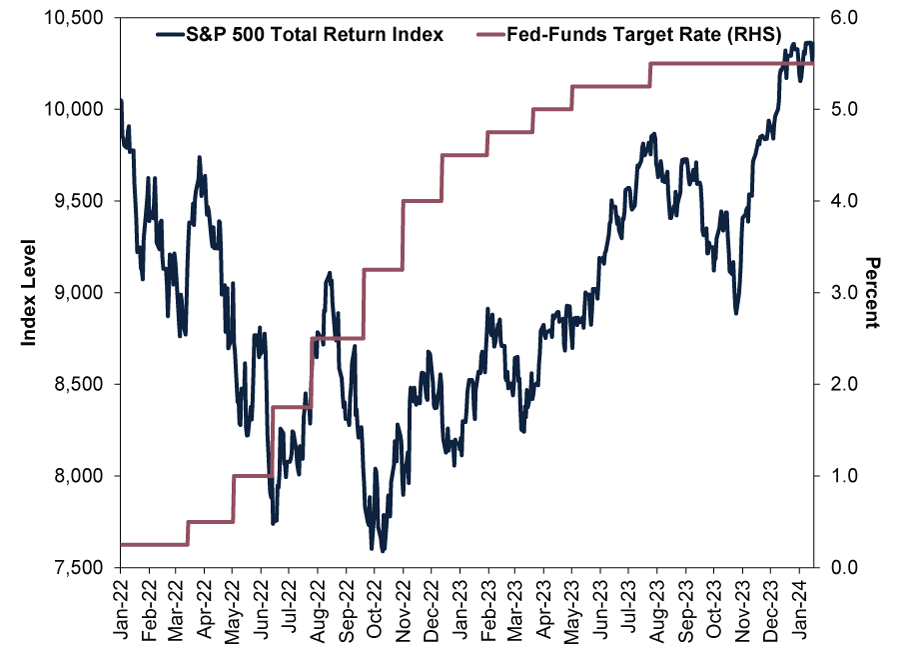

The conventional wisdom we observe holds rate hikes bad, cuts good—an apparent matter-of-fact investing truism hardly worth questioning. But just because it is seemingly repeated ad nauseum doesn’t make the truism, ummmm, true. Consider the last couple years of US rate hikes. (Exhibit 1) In our view, America’s benchmark S&P 500 stock market index initially fell as it grappled with the Federal Reserve’s rapid rate U-turn from arguing inflation was “transitory”—and didn’t require a shift in policy—to hiking fast.[ii] Alongside other issues that roiled sentiment in 2022, we think this contributed to the bear market (typically prolonged, fundamentally driven decline exceeding -20%) in US dollars.[iii] But a new bull market began that October as stocks moved on, in our view, largely because the deep economic contraction commentators we follow said would ensue failed to materialise.[iv]

Exhibit 1: Stocks Rose Through Rate Hikes

Source: FactSet, as of 18/1/2024. S&P 500 total return and fed-funds target rate (upper limit), 3/1/2022 – 18/1/2024. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns. Please see our Annex below for an extended, five-year version of this chart.

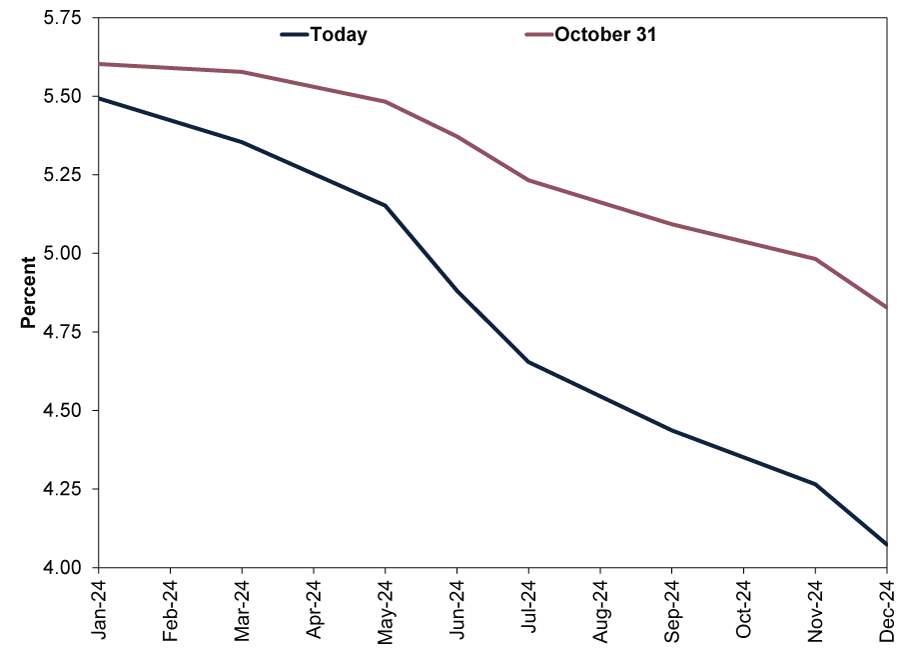

But now, as inflation irregularly but swiftly cools, rate cut expectations are gathering steam. (Exhibit 2) In mid-December, markets started pricing in rate cuts at the Fed’s March 20 meeting—and a more rapid pace thereafter. Supposedly, according to the financial press we review, this is the reason behind stocks’ latest leg up. Some commentators we follow go further, saying if the Fed doesn’t cut rates there will be recession (widespread economic contraction).

Exhibit 2: Markets Pricing in Earlier—and More—Rate Cuts

Source: CME FedWatch Tool, as of 18/1/2024.

But our research shows rate cuts aren’t necessary for growth—or the bull market. The bull market to date has been led by large growth-orientated firms, which we find generally don’t rely on bank lending for funding given the ample cash on their balance sheets.[v] Therefore, we don’t think rate cuts to re-steepen the yield curve and encourage loan growth are crucial to keep the growth-led rally going. (The yield curve shows the difference between short and long rates, and since banks borrow short and lend long—profiting from the difference—a steeper yield curve encourages lending, according to our analysis.)

Now, rate cuts could boost credit-sensitive value-orientated stocks, and we are watching for this as a potential sign of an impending leadership shift.[vi] US commercial and industrial loans have fallen slightly year-over-year since October, down -1.0% y/y at 2023’s end.[vii] If this picks up, possibly amidst rate-cut enthusiasm, then value stocks could benefit. But we doubt business lending’s nascent dip is significant for large growth stocks in Tech and Tech-like industries in other sectors.

We don’t think rate cuts are critical for the economy, either. National average savings deposit rates in America, representing a good chunk of US banks’ funding costs, remain well below the effective fed-funds rate (0.46% vs. 5.33%)—and long rates (4.14%).[viii] This disconnect is why we think yield curve inversion—when short rates top long—since 2022 hasn’t caused deep credit contraction as many commentators we follow anticipated. In previous cycles, deposit rates were more closely linked to overnight fed-funds rates.[ix] Though banks’ funding costs are creeping higher as they compete for customers seeking more attractive rates, rising rates haven’t flowed through to depositors broadly, as banks remain awash with deposits overall.[x] Rate cuts may help relieve the modest funding pressure banks face, but it isn’t as if the economy is starved of credit.[xi] So whilst cuts—and a steeper yield curve—may usher in more confidence, particularly amongst businesses that have retrenched thinking an economic downturn is around the corner, we doubt the economy and markets hinge on them like many financial publications we read suggest.

History also shows rate cuts aren’t the automatic bull fuel they imagine. Just like rate hikes aren’t automatically bearish, we find there are other fundamental factors that drive stocks. Note the last three Fed rate cut cycles (2000 – 2003, 2007 – 2008 and 2019 – 2020) coincided with falling US stocks.[xii] Prior to that, cuts in the mid-1990s came alongside rising stocks.[xiii] Before that, the Fed started cutting in mid-1989 and kept doing so through 1992.[xiv] During this span, stocks initially rose, flipped into a bear market and started a new bull market.[xv] And prior to that, a rate cut cycle in the mid-1980s came amidst overall rising stocks again.[xvi]

Do you see any pattern? We don’t—just like hikes. Why? Monetary policy isn’t all powerful. In our experience, nothing it does has the ability to override economic cycles and how they relate to expectations. Those factors—to which the Fed may contribute at the margin—drive markets most of all, based on our research.

The main takeaway we see from current rate cut obsession: All the focus on the monetary policy as the main factor driving stocks’ rally undersells the economy’s fundamentals—sentiment is still sceptical. But if rate hikes never drove recession to begin with, we fail to see why a lack of rate cuts will now. The economy is already proving it can handle this level of rates just fine.[xvii]

When alarm over a false factor—rate cut uncertainty—is prevalent, we find it shows reality is better than appreciated. Rather than fret what monetary policymakers will or won’t do as headlines blare about this or that consequence, we suggest investors take the pervasive handwringing as bullish. After all, to paraphrase Sir John Templeton’s famous quote, bull markets grow on scepticism.[xviii]

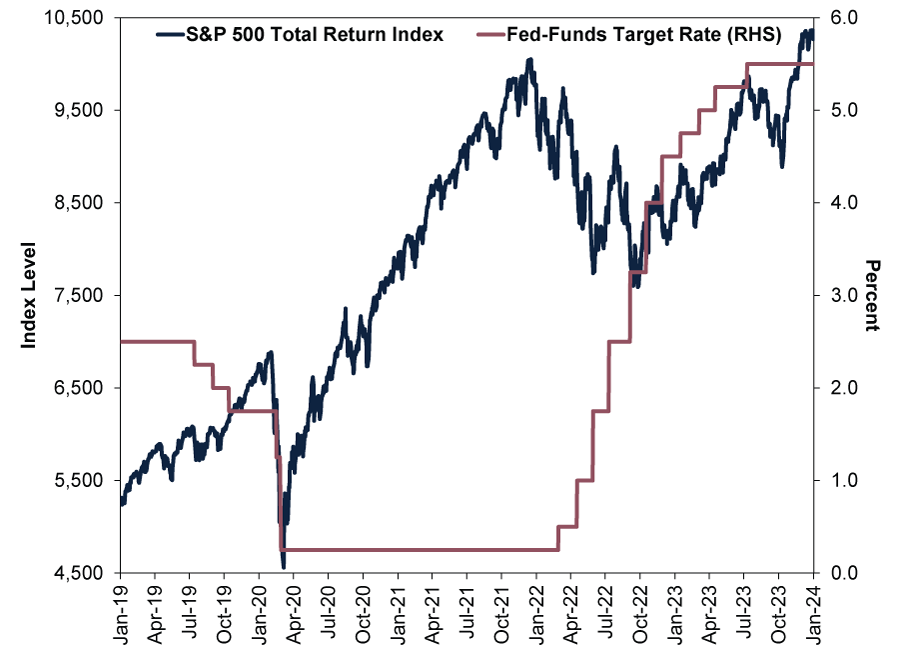

Annex: S&P 500 Total Return and Fed-Funds Target Rate, January 2019 – January 2024

Source: FactSet, as of 18/1/2024. S&P 500 total return and fed-funds target rate (upper limit), 18/1/2019 – 18/1/2024. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[i] Source: FactSet, as of 18/1/2024. Statement based on MSCI World returns with net dividends.

[ii] “Monetary Policy in the Time of COVID,” Jerome H. Powell, Federal Reserve, 27/8/2021.

[iii] Source: FactSet, as of 18/1/2024. Statement based on MSCI World returns in USD, 3/1/2022 – 12/10/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[iv] Ibid.

[v] Source FactSet, as of 18/1/2024. Statement based on MSCI World Large Cap Growth and MSCI World returns with net dividends. Growth-orientated firms’ earnings come from expansion and capitalising on innovation and long-term trends and tend to trade at above-average valuations since investors are often willing to pay more for their long-term potential.

[vi] Value-orientated firms’ earnings are more cyclical (rising and falling with the economic cycle), debt is higher and valuations (like price-to-earnings ratios) are lower.

[vii] Source: Federal Reserve Bank of St. Louis, as of 18/1/2024. Commercial and Industrial Loans, All Commercial Banks, 12/27/2023.

[viii] Source: Federal Reserve Bank of St. Louis and FactSet, as of 18/1/2024. National Deposit Rates: Savings, December 2023, Federal Funds Effective Rate and 10-year Treasury yield, 18/1/2024.

[ix] “Savings Interest Rates Don't Rise as Quickly as You Might Think,” Alex Fitzpatrick, Axios, 29/6/2022.

[x] Ibid.

[xi] Source: Federal Reserve Bank of St. Louis, as of 18/1/2024. Statement based on Loans and Leases in Bank Credit, All Commercial Banks.

[xii] Source: Federal Reserve Bank of St. Louis, FactSet and Global Financial Data, Inc., as of 18/1/2024. Discount rate, January 1950 – October 1982, fed-funds target rate, October 1982 – December 2023, and S&P 500 total return in US dollars, January 1950 – December 2023. Note the Fed’s main benchmark rate switched from the discount rate to the fed-funds target rate in October 1982.

[xiii] Ibid.

[xiv] Ibid.

[xv] Ibid.

[xvi] Ibid.

[xvii] Source: FactSet, as of 18/1/2024. Statement based on US fed-funds rate and gross domestic product (GDP, a government measure of economic output).

[xviii] “John Templeton,” Staff, Philanthropy Roundtable, accessed 18/1/2024.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today