Personal Wealth Management / Market Analysis

Data Spotlight: Commodity Prices

Commodities have largely erased last year’s spike.

Amid all the mixed economic data and recession forecasts, some actual good news hit the wires Wednesday: UK gasoline prices have now erased the spike that followed Russia’s invasion of Ukraine. That adds to the growing list of commodity prices that have settled near or below pre-invasion levels—a big disinflationary force. Here we will round up a few to highlight the shifts. It may take time for this improvement to flow through to consumer prices—and Consumer Price Index inflation data—but in time it should, easing one of 2022’s primary fears.

As the world digested the invasion and the West’s economic response, commodity prices of all sorts spiked as fears of shortages ran rampant. While food and metals started easing as spring progressed, oil stayed elevated into the summer, and natural gas went haywire as Russia cut supply to Europe—spiking electricity prices with it. All of this contributed to fast inflation rates. Not just via food and energy prices, but through businesses’ increased overhead costs and the fact that a wide range of consumer products have petrochemical feedstocks. In our view, this was one of the primary contributors to the fear storm that drove 2022’s bear market. Inflation itself may not be inherently bearish, but the fear of it—combined with fears of rate hikes, supply chain kinks, the war, politics and more—hit sentiment hard. That means improvement should be a big relief and tailwind for stocks. Commodity price improvement suggests this is in the offing.

To see it, here are several charts showing how many commodities have come full circle. We start with the energy basics: Global crude oil prices, US natural gas and European natural gas.

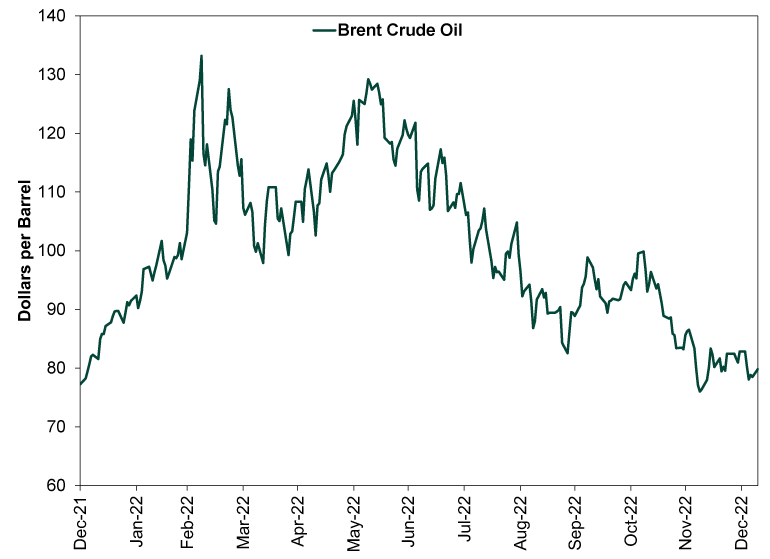

Exhibit 1: Brent Crude Oil

Source: FactSet, as of 1/10/2023. Brent crude oil spot price, 12/31/2021 – 1/9/2023.

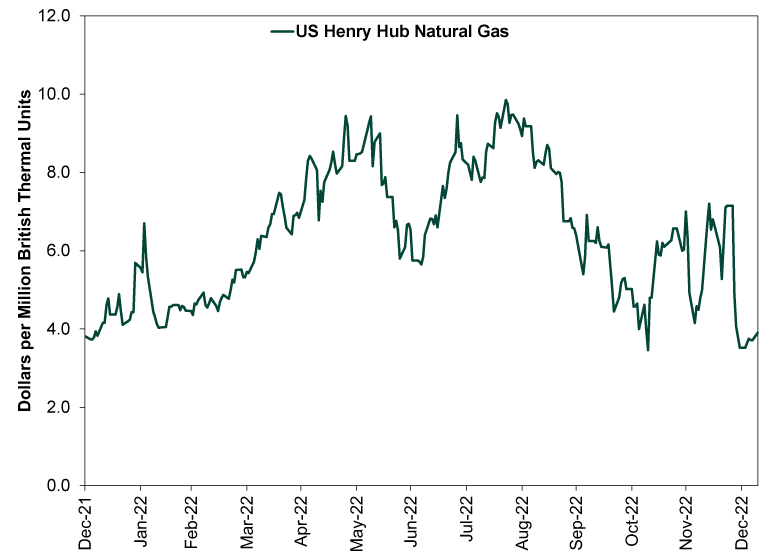

Exhibit 2: US Natural Gas

Source: FactSet, as of 1/10/2023. Henry Hub Natural Gas spot price, 12/31/2021 – 1/9/2023.

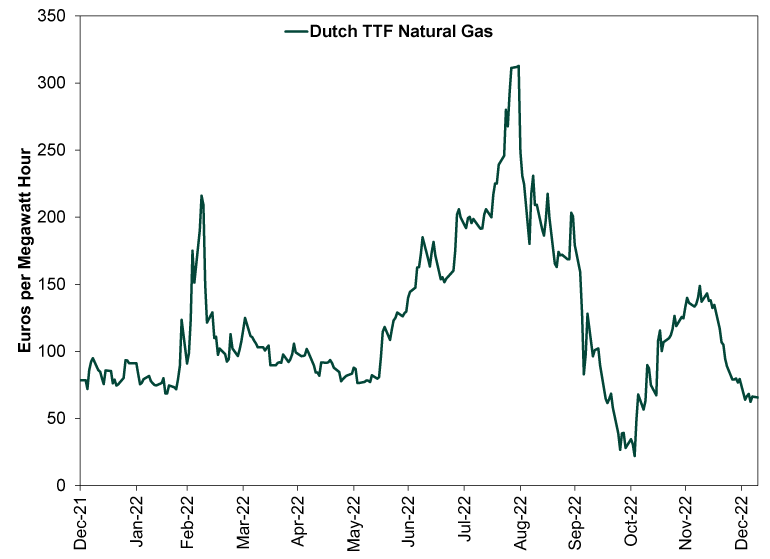

Exhibit 3: European Natural Gas

Source: FactSet, as of 1/10/2023. Dutch TTF Natural Gas spot price, 12/31/2021 – 1/9/2023.

On the last one, note: That level is still elevated, given a rise in late 2021 tied to slack wind power generation. But it is far from the calamity so many feared just weeks or months ago, and it represents a landmark shift away from being under Russian President Vladimir Putin’s thumb on energy.

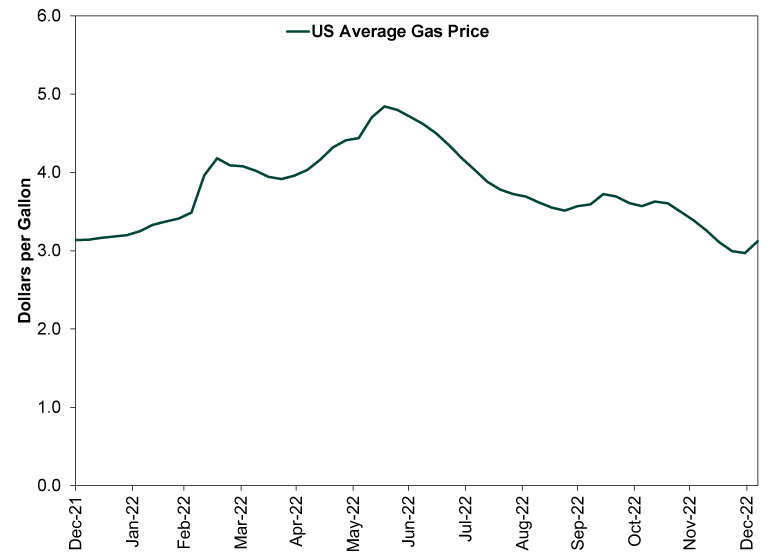

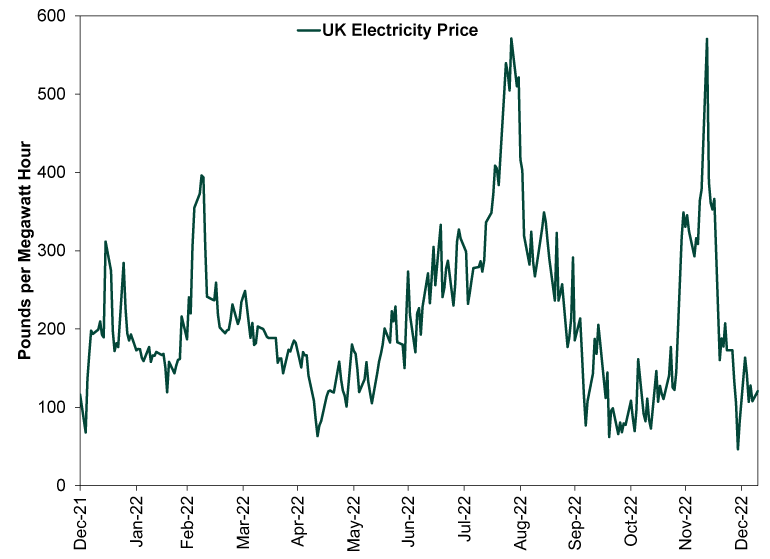

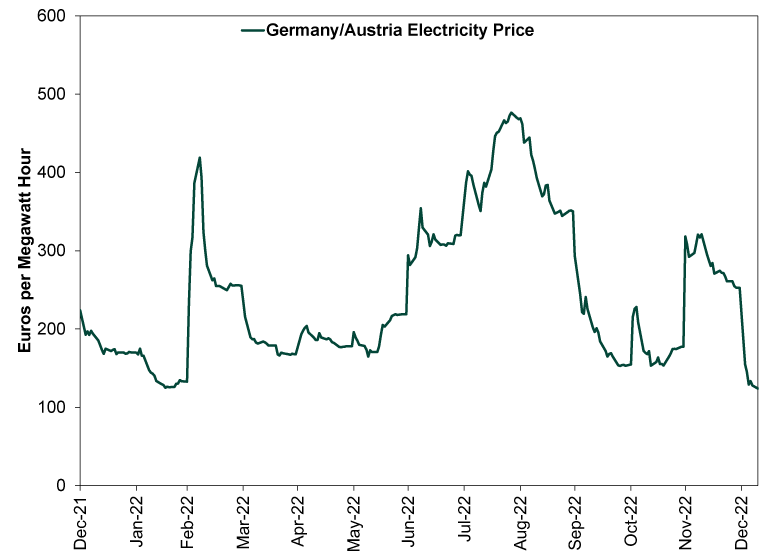

As oil prices eased, so did gasoline prices on both sides of the Atlantic. UK and Continental European power prices, meanwhile, mirrored natural gas’s wild ride. But now they too are down, which should help ease concerns of high overhead putting companies out of business—a big fear in the UK right now as the government mulls reducing support for businesses facing high energy costs.

Exhibit 4: US Average Gasoline Price

Source: FactSet, as of 1/10/2023. Weekly average price for regular unleaded, 12/31/2021 – 1/9/2023.

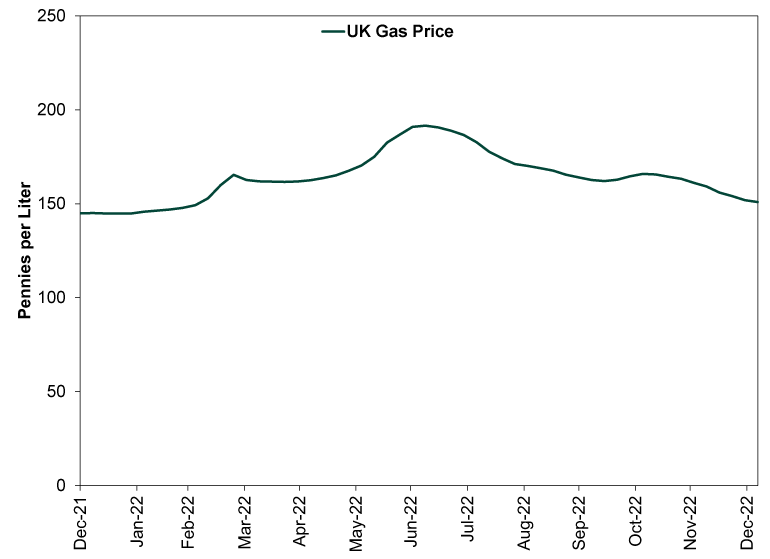

Exhibit 5: UK Average Gasoline Price

Source: FactSet, as of 1/10/2023. Weekly average price for regular unleaded, 12/31/2021 – 1/9/2023.

Exhibit 6: UK Electricity Price

Source: FactSet, as of 1/10/2023. NORX UK Power Daily Average, 12/31/2021 – 1/9/2023.

Exhibit 7: Central European Electricity Price

Source: FactSet, as of 1/10/2023. German/Austrian Power Base Near-Term, 12/31/2021 – 1/9/2023.

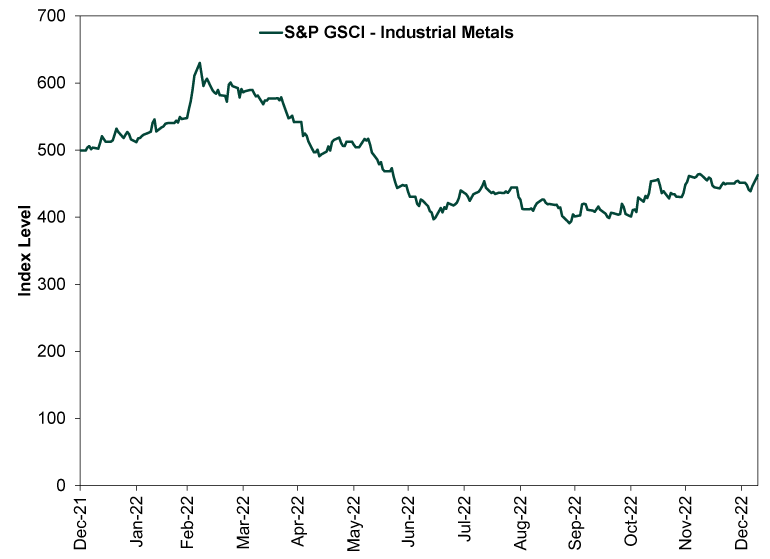

Metals prices have also more than erased their wartime spike.

Exhibit 8: Industrial Metals Prices

Source: FactSet, as of 1/10/2023. S&P GSCI – Industrial Metals, 12/31/2021 – 1/9/2023.

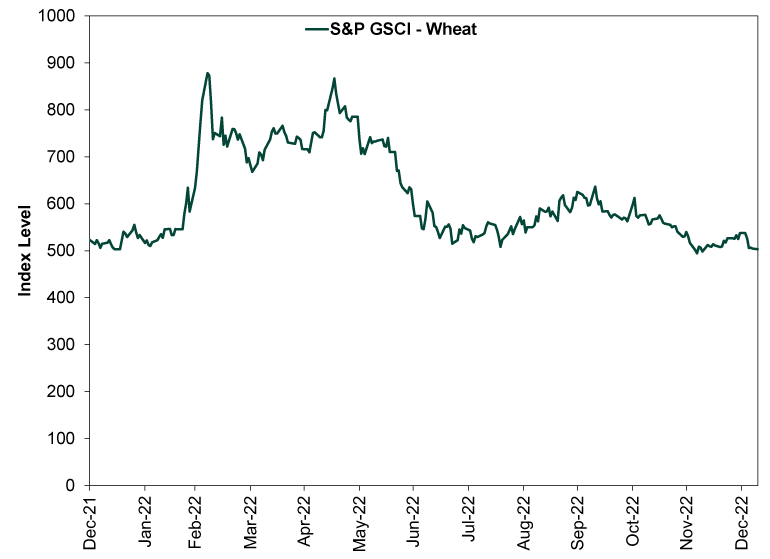

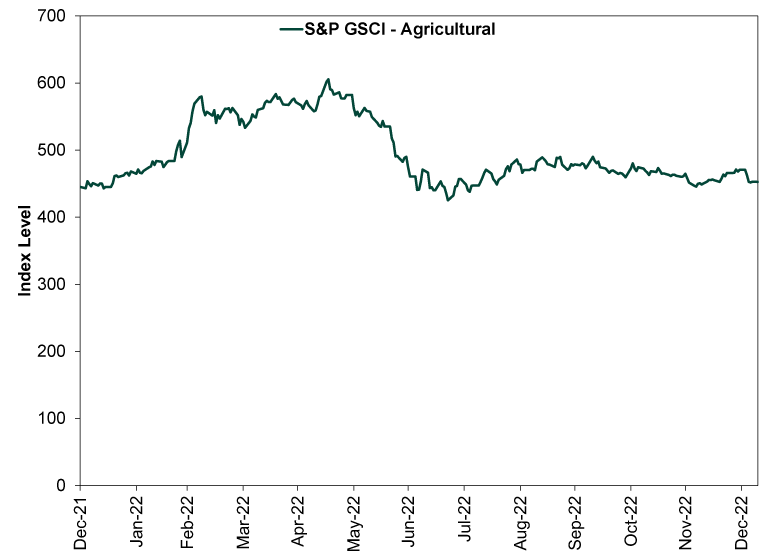

So have grain prices—the nexus of fears, given Ukraine’s status as one of the world’s main breadbaskets—and agricultural commodity prices overall, which point to lower food prices.

Exhibit 9: Wheat Prices

Source: FactSet, as of 1/10/2023. S&P GSCI – Wheat, 12/31/2021 – 1/9/2023.

Exhibit 10: Agricultural Commodity Prices

Source: FactSet, as of 1/10/2023. S&P GSCI – Agricultural, 12/31/2021 – 1/9/2023.

Commodity prices got heaps of attention on the way up, but their drop hasn’t generated anywhere near as many headlines. That suggests to us that there is a lot of room for sentiment to catch up to reality on this front, boosting stocks along the way.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today