Personal Wealth Management / Market Analysis

Recession Talk in the Fed’s Minutes Is Nothing New for Stocks

Economists have projected recession for months.

In the corporate world, few documents conjure boredom and mundanity more than those with the dreaded title, “Meeting Minutes.” After all, who needs to relive the tedium of a meeting with a recap of what happened in said meeting?[i] Unless, that is, you are a Fed watcher. Then, you jump with glee whenever minutes of the Federal Open Market Committee’s (FOMC’s) monetary policy meetings come out. It is usually the first peek behind the curtain at the debate and forecasts that led to whatever decision was subsequently shrouded in a short press release full of Fedspeak. We got another dose of this week, with the release of March’s meeting minutes—which revealed Fed staff project a mild recession this year. Headlines have jumped on this, implying it represents some major new recession risk for stocks. We doubt it.

For one, the Fed’s forecast isn’t exactly revolutionary … and it isn’t exactly the Fed’s forecast. March’s meeting releases included the FOMC’s infamous “dot plot,” which illustrates each member’s personal projections for economic growth, inflation and interest rates. The FOMC’s consensus projection, at least on the face of these dots, wasn’t for a recession. But Fed staff economists, after crunching some numbers and mulling over a potential lending pullback after Silicon Valley Bank and Signature Bank failed last month, evidently deemed a “mild” recession likely later this year, followed by renewed growth in 2024 and 2025. We guess the transcripts will show exactly how much this influenced the FOMC’s decision to slow rate hikes to just 0.25 percentage point, but we will have to wait five years for those.

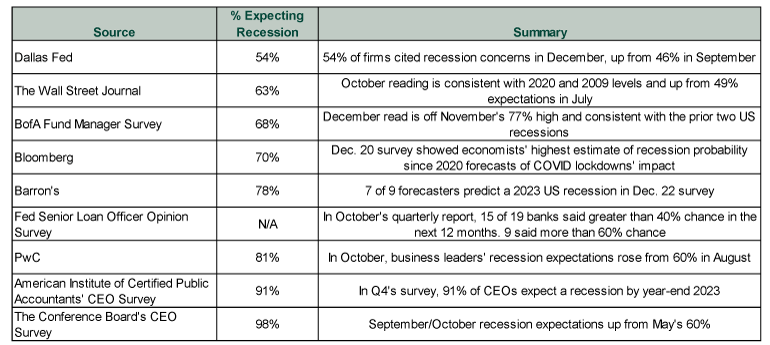

In the meantime, headlines seized on this as some sort of sea change for the US’s economic outlook. We have a hard time seeing that, considering how widespread recession expectations are … and how long that has been the case. To wit, here is a snapshot of surveys and forecasts we put together when the year began. As you will see, recession was a foregone conclusion throughout the business and investment worlds.

Exhibit 1: Economic Forecasts When 2023 Began

Source: Federal Reserve Bank of Dallas, The Wall Street Journal, Bank of America, Bloomberg, Barron’s, Federal Reserve, PwC, AICPA and The Conference Board, as of 12/29/2022. Note: The Fed’s Senior Loan Officer Opinion Survey doesn’t normally include questions about recession. But researchers elected to include a special set of questions on recession in October, which illustrates just how front-of-mind recession worries are presently.

Forecasts improved a bit in January and early February as more economic data beat expectations, but it didn’t last. Soon the good news is bad news mentality struck, and most observers interpreted good data are evidence the Fed would have to hike more to bring inflation down, and those hikes would induce recession. Bank failures added to this, spurring (logical) fear of a lending pullback if contagion fears inspired lenders to hoard cash. We are watching that, too. But the upshot is that where the Bloomberg survey shown in Exhibit 1 improved to a still-lofty 60% of economists projecting recession earlier in Q1, it closed March back up at 65%.[ii]

So in a way, the Fed is doing what it always does: following. Just as its interest rate decisions tend to follow the market’s moves—whether in 3-month Treasury yields pricing its decisions in advance or fed-funds futures moving first—staffers projections merely echo the private sector. That doesn’t shock us at all, considering the amount of groupthink in this world. But it means projections are more a reflection of sentiment than a signpost for what will actually happen. We aren’t saying they will for sure be wrong, but rather that the forecast itself shows what markets have probably already priced in.

Not just because Fed staffers are projecting a recession, but because if a recession were to occur, it would be the most widely expected recession in history. Fisher Investments Founder and Executive Chairman Ken Fisher often observes that he can’t recall a time in his 50-year career when so many people and outlets forecasted a recession. Usually downturns are sneaky, leaving everyone with egg on their face. If one happened now, it would likely just tick a box. For stocks, too, considering bear markets usually precede recession and we had one last year—and recession forecasts abounded when stocks were still falling. To us, that is a very good sign that stocks already dealt with the potential for an economic downturn and are now moving on. Consistent with that, businesses also seem to have reacted to a recession in advance, cutting excess wherever possible. They didn’t wait. So if a recession does strike, we may not see as much cost-cutting as usual, which points to a milder downturn than we might otherwise get. Anticipation is mitigation.

Either way, given stocks pre-price widely known information—including forecasts—a recession would have little to no surprise power. We don’t think confirmation of a downturn alone would be reason for stocks to sink to new lows. For that, the recession would have to be much deeper and longer than everyone expects. Given most economic indicators continue beating expectations and loan growth is holding up so far, that doesn’t seem likely for now.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary What Investors Need to Know About Geopolitical Turmoil

2026-02-06

2026-02-06 -

Market Volatility The Early Midterm-Year Chop Is On2026-02-06

-

Expert Commentary This Week in Review | Government Shutdown, Global PMIs, Q4 Earnings

2026-02-06

2026-02-06 -

Market Analysis Setting the Record Straight: New Fed Chairs Aren’t Auto-Negative2026-02-05

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today