Personal Wealth Management / Market Analysis

Stay in May

Pundits agree: “Sell in May and Go Away” will be a winning tactic this year—but how sound is their reasoning?

Should investors giddy-up and get out of markets this May? Source: Hagen Hopkins, Getty Images.

THIS is the year Sell in May is going to work—at least that’s what many pundits would have you believe. Why this year? Apparently, in addition to those supposedly weak historical summer returns, because we’ve had no recent corrections and 2014 midterms are approaching. But none of those—individually or combined—proves selling in May will work this year. Even if this summer’s a bummer, Sell in May is bunk. Markets are cyclical (not seasonal)—this year isn’t different. In our view, investors would do better focusing on the mid to longer-term outlook and their long-term goals.

Sell in May allegedly dates back to 19th century London, when brokers generally, um, broke for vacation in May and returned to work shortly after September’s St. Leger’s Day horse race. Folks assumed fewer brokers on call meant less trading and higher volatility—so they sold out for the summer and got back in when things returned to normal. Whether that anecdotal origin is valid or not, it has no relation to today. Yes, folks probably horse around some between May’s Kentucky Derby and St. Leger Day—it’s summer! But markets have changed a lot since Sell in May was invented (to the extent it was ever rational in the first place). New technologies allow folks to trade any time almost anywhere—the office, at home, Bora Bora ... even at the races. Still, Sell in May rears its head every year, and for various reasons even financial pros recommend following it—with surprisingly few neigh ... er ... naysayers.

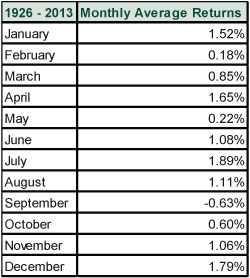

Perhaps because, since 1926, summer months (May through October) historically averaged lower returns than the winter (November through April): 4.1% versus 7.4%, respectively.i But we fail to see the logic here. Summer was lower, but both were positive. Breaking the figures down further show there is little historic weakness in summer months over time:

Exhibit 1: Monthly Average Returns

Source: Global Financial Data and FactSet, as of 5/1/2014. S&P 500 Total Returns 12/31/1925-12/31/2013.

Only September is negative—and even that is skewed by 2008 and the Great Depression—and July (the middle of summer) has the best returns, contradicting Sell in May’s thesis. February, the second-weakest month on average, falls during that supposed winter sweet spot. Plus, markets rise far more often than not—and even slower growth compounds over time. Nor are those months predictably slow. The averages might skew lower, but those averages are still made up of many extremes. If Sell in May worked, everyone would do it! And it would lose its comparative advantage. You’d have to start selling in April, March, February, etc., to stay ahead of the crowd—until you’re perhaps invested in the month of November only.

Usually, a good many pundits are content to roll their eyes at this seasonal myth every May. This time, though, many seem to think this year it’ll work. A prevailing argument is we’ve gone an above-average time between corrections, so we’re overdue and summer is when it’ll strike. But time doesn’t determine when corrections come—it’s not unusual to see multiple years go by without a correction. There is no law of averages saying we must have one tomorrow. We might get one! But it’s impossible to say. Corrections are driven by sentiment and can start (and end) at any time for any reason—they’re completely unpredictable. Even if you manage to avoid a drop, it still requires near-perfect market timing (which no one has) to capitalize by hopping back in to catch the upside. If you sell in May because a correction might happen—and then it doesn’t—the opportunity cost could be big.

The other argument is a twist on one we’ve heard a few times this year: 2014 is a midterm year—supposedly bad for stocks, which will falter ahead of the contest. It’s true four of the last six midterm years didn’t have great returns in May through October. But that’s mostly happenstance: 2010 had a summer correction. 2002 was in the middle of a bear market. 1998 featured the Russian Ruble Crisis. And 1990 was in the middle of another bear. These drops had their own unique, fundamental causes. That they happened to overlap, in full or in part, with the summer season is coincidental, not causal. Full year returns, too, show midterm years aren’t inherently negative: 2010 was up (+15.1%), 2002 down (-22.1%), 1998 was up a lot (+28.6%), 1994 flattish (+1.3%), and 1990 down a little (-3.1%).ii Midterm years are just more variable—and usually up during second terms when gridlock is high, like today. Not a reason to sell in May.

So calendars and past corrections aren’t predictive, and midterms aren’t a guaranteed headwind—what does that mean for summer 2014? We can’t say. In the short term, markets are often too irrational to forecast—they’re driven by reactions and emotions, which are inherently volatile and all over the map. But getting seasonally defensive isn’t a guarantee for higher returns and it likely doesn’t help with longer-term goals, which should always be the aim when making investing decisions.

Investors usually do best keeping their eyes on the horizon—their long-term goals and what’s likely in markets over the next year or so. Sell in May encourages focusing on short-term performance—that may or may not even happen—and investing according to fear and fallacies, not fundamentals. Both are proven to hurt investors’ long-term returns, and not just because of extra trading commissions and taxes. Exiting markets, especially in a strong bull market, can lead to big opportunity costs—missing out on gains you may need down the road. None of the reasons pundits point to today are fundamental or unique or credible enough to outweigh that.

i FactSet and Global Financial Data, as of 5/2/2014.

ii Source: Global Financial Data, Inc. as of 2/19/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today