Personal Wealth Management / Economics

Taking Industrial America’s Temperature

Recent data from America’s manufacturers suggest conditions are better than feared.

Unemployment and consumer spending data out later this week are set to steal the spotlight—understandable, given consumer spending is over two-thirds of US GDP and unemployment’s (flawed) reputation as an all-telling barometer. Lost in the shuffle lately but still worth a check-in? Heavy industry. A review of recent manufacturing data reveals that, despite some mixed figures, factories overall are contributing to growth.

Let us start with the most timely figure, November’s S&P Global flash manufacturing purchasing managers’ index (PMI). It fell below 50—suggesting more respondents reported contraction than growth—with new orders also sinking. Is that a harbinger of worse to come? Perhaps, but it isn’t assured. Because PMIs measure only growth’s breadth, not its magnitude, manufacturing’s dip to 47.1 from October’s 50.7 doesn’t necessarily mean falling output.[i] If the majority of manufacturing firms surveyed see contraction, but the minority’s actual output is larger, growth could still occur overall—we will have to wait and see. It is also the first reading below 50 since June 2020, and we caution against drawing big conclusions from any one data point, for good or ill.

Meanwhile, regional PMIs representing a broad swath of Fed districts were mixed in November. (Note: Regional PMIs’ dividing line between contraction and expansion is zero.)

- New York’s Empire State Manufacturing Survey rose 13.6 points to 4.5, its first positive reading since July.

- In contrast, the Philadelphia Fed’s PMI fell -10.7 points to -19.4.

- Richmond’s PMI edged up from -10 to -9 and Kansas City’s ticked from -7 to -6. Still negative, but indicating a narrower swath of firms seeing contraction.

- To round them out, Dallas’s PMI fell -5.2 points to 0.8, barely positive, suggesting little change from October.[ii]

Beyond PMIs, the latest releases measuring actual output suggest Q4 business equipment investment and manufacturing production are off to a good start. While industrial production fell -0.1% m/m in October, reversing September’s 0.1% gain, this was largely a function of a -1.5% m/m drop in utility production, perhaps tied to weather.[iii] But manufacturing, the largest segment covered in these data, rose 0.1% m/m in October, its fourth straight monthly gain. Then, too, within manufacturing, commodity-oriented industries detracted the most. Wood, metal and mineral products shrank in durable manufacturing, while petroleum and chemical products contracted on the nondurable side. More than offsetting these pockets of manufacturing weakness: Higher value-added machinery and equipment rose strongly. This hints at business investment remaining firm after today’s revised Q3 2022 GDP report showed a 5.1% annualized climb.[iv]

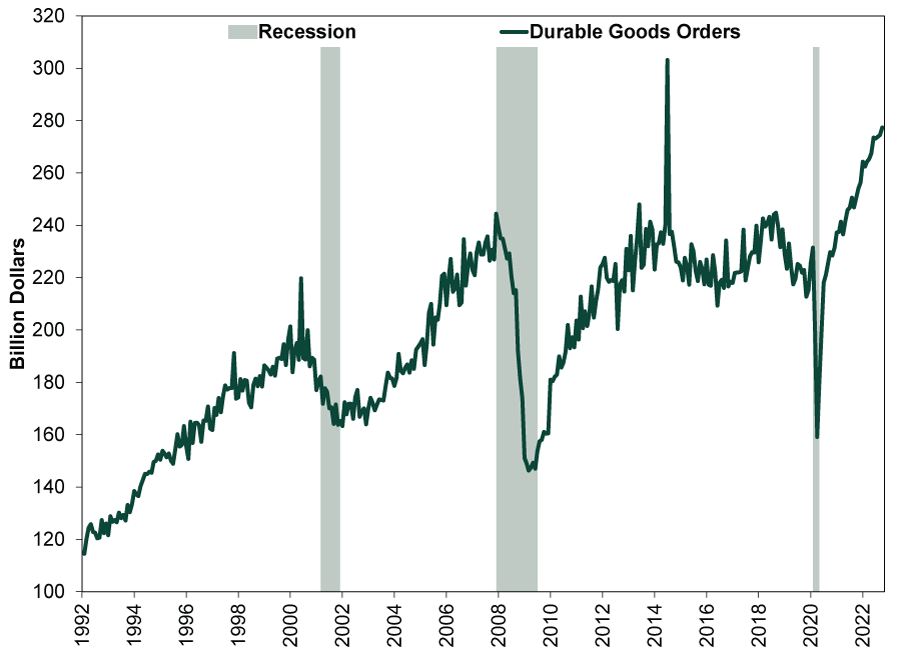

Looking ahead, October durable goods orders—a forward indicator of output—rose 1.0% m/m.[v] Nondefense capital goods ex. aircraft, which is less volatile and many use as a proxy for business investment, rose 0.7% m/m. As Exhibit 1 shows, though, headline durable goods orders haven’t been very volatile since reopening—they have shot higher. This may be partially due to inflation—durable goods orders aren’t inflation adjusted—but nonetheless, it suggests businesses continue spending on big ticket machinery and equipment.

Exhibit 1: Durable Goods Orders Making New Cycle Highs

Source: Federal Reserve Bank of St. Louis, as of 11/29/2022. Durable goods orders, February 1992 – October 2022.

These data don’t rule out the recession most observers expect. They are broadly mixed, like so many other data points these days. But they also aren’t categorically awful or recessionary. Now, one shouldn’t overrate manufacturing’s impact—for good or ill. It is just 11.3% of GDP.[vi] Yet we also think overlooking the data would be a mistake, particularly when economic sentiment is so broadly dour. In such scenarios, even small things going a little better than feared can be fuel for a recovery.

[i] Source: S&P Global, as of 11/23/2022.

[ii] Source: Federal Reserve Banks of New York, Philadelphia, Richmond, Dallas and Kansas City, as of 11/29/2022.

[iii] Source: Federal Reserve, as of 11/16/2022.

[iv] Source: Bureau of Economic Analysis, as of 11/30/2022.

[v] Source: Census Bureau, as of 11/23/2022.

[vi] Source: Bureau of Economic Analysis, as of 9/29/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today