Personal Wealth Management / Market Analysis

The Fed Hikes Again, But the Thrill Is Gone

Hike and pause or no, a broader look at the recent past shows the Fed likely isn’t a threat to stocks’ climb.

Shocking no one, the Fed hiked its benchmark rate by another 25 basis points (0.25 percentage point) today, bringing the fed-funds target range to 5.0% – 5.25%. The world had largely already penciled that in, which may be why a slight tweak to the Fed’s statement grabbed most attention, fueling suspicion that it is done for now. As always, we wouldn’t read into it. But whether the Fed is done or keeps hiking, we doubt it means much for stocks.

In past statements, the Federal Open Market Committee (FOMC, the cadre that makes monetary decisions) has included this language: “The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” This time, the first of those two sentences was gone, while the second returned with some slight modifications. Even though it referenced the potential for future tightening, the absence of the “some additional policy firming may be appropriate …” bit is ratcheting up expectations that the era of rate hikes is over.

Maybe it is. Back in the 2004 – 2006 tightening cycle, 5.25% was the peak fed-funds rate. In his post-meeting presser, Fed head Jerome Powell also acknowledged that the tighter credit conditions following the failures of Silicon Valley Bank, Signature Bank and now First Republic had done some of the FOMC’s work for them. “We won’t have to raise rates quite as high as we would have if this had not happened.” But also, it is entirely possible they keep going. Powell reiterated the Fed’s time-honored mantra that decisions are data-dependent. The statement stressed that point, too. Who knows how the 11 FOMC members will interpret the data arriving between now and June’s meeting. Or even what data they exactly emphasize or disregard, and what they think said data should do. Or how that will all evolve by July’s meeting and beyond. The Reserve Bank of Australia just hiked again after pausing in April. Anything is possible, and you can’t predict it in advance.

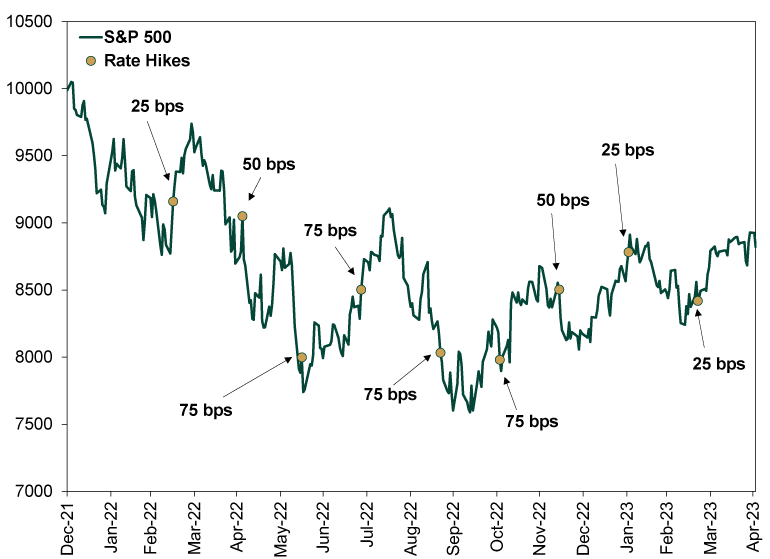

Whether or not the Fed has more rate hikes to go, we see good reason to believe stocks won’t much mind. As Exhibit 1 shows, they have risen alongside rate hikes for over half a year now—even with the yield curve inverted. The S&P 500 may be down since rate hikes began in March 2022, but only by -3.7%, and they are up since the first 75 basis-point hike last June.[i] Another hike or two wouldn’t much change overall banking conditions, considering that even with their recent increase, most deposit rates remain well below fed-funds. Movement on that front seems tied more to overall market conditions than what the Fed does.

Exhibit 1: Rate Hikes Don’t Have Pre-Set Market Impact

Source: FactSet and Federal Reserve, as of 5/3/2023. S&P 500 total return index, 12/31/2022 – 5/2/2023.

This is true outside America as well. The Bank of England was the first major central bank to start hiking rates on December 16, 2021. Since then, the MSCI UK Investible Market Index (IMI) is up 18.6% in dollars and 8.8% in pounds.[ii] The European Central Bank was late to the party, starting on July 21, 2022. MSCI’s eurozone index is up 25.0% in dollars and 16.1% in euros since then.[iii]

The investing world is stuck in the perception that rate hikes fueled last year’s bear market, and they probably did contribute to the deep pessimism that weighed on markets (along with inflation, oil prices and a host of others). Perhaps the fact the early hikes came as part of a giant Fed and central bank U-turn on inflation added to their surprise. But returns since last summer arguably tell a different story, one of stocks’ resilience and ability to get over widespread fears. It is time more investors started noticing.

[i] Source: FactSet, as of 5/3/2023. S&P 500 total return, 3/16/2022 – 5/2/2023.

[ii] Source: FactSet, as of 5/3/2023. MSCI UK IMI return with net dividends in USD and total return in GBP, 12/16/2021 – 5/3/2023.

[iii] Ibid. MSCI EMU Index returns with net dividends in USD and EUR, 7/21/2022 – 5/2/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today