Personal Wealth Management / Market Analysis

A Historical Look at Inflation’s Impact on Market Returns

Is inflation really as bad for future market returns as some folks fear?

While most focus recently flipped to trade, tariffs and Trump, Treasury yields still garner a lot of attention. Yields have climbed this year, coinciding with worries of higher inflation. After all, inflation expectations play a big role in bond yields, so some experts think fixed income investors are anticipating higher prices to come. An offshoot to this forecast: the fear higher inflation will also end up weighing on future stock market returns. All the hand-wringing seems off, in our view. For one, short-term bond market volatility doesn’t mean yields are destined to keep rising and stay higher. Plus, history shows higher inflation doesn’t crimp stocks—they can do fine in high inflation and low inflation environments alike.

After the BLS released January CPI—which included the fastest month-on-month rise in five months—experts started debating if and when higher inflation would start hurting equity markets. Questions ranged from what will happen if Treasury yields breach 3% to whether stock investors will jump to the “safer” returns of fixed income. Philosophically, we have qualms with these worries. Despite Treasury yields’ recent uptick, we don’t see interest rates jumping higher and staying there this year. While inflation expectations do influence yields—if investors anticipate higher inflation to come, they will demand a higher premium to account for the hit to their purchasing power—inflation still looks benign for the foreseeable future. For one, inflation is still overall low even after the pickup in Treasury yields. The Fed has hiked short rates five times since December 2015, and while forecasting future hikes is a speculative endeavor, rate hikes are anti-inflationary. They tend to give investors the perception the Fed has contained inflation risks—thus limiting premium demand.

Plus, the Fed’s hiking short rates alongside benign long rates leads to a narrower spread between the two. The result: a flatter yield curve, which dampens banks’ eagerness to lend. This weighs on money supply growth, and if there isn’t as much money chasing a limited number of goods and services, inflation generally stays benign. As for the fear investors will leave stocks for slightly higher bond yields? This is a rerun of the “Great Rotation” myth—the notion bond investors pursued stocks in the search of higher yield. However, this fallacy assumes leaving an asset class for another hurts the one being sold. But remember: For every seller, there is a buyer (and vice versa), so money going in and out between different asset classes effectively cancels. Moreover, fund flows mostly contradicted the notion that some Great Rotation ever happened.

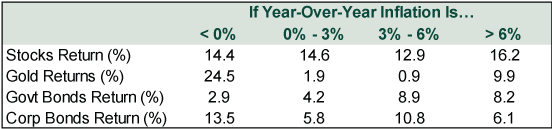

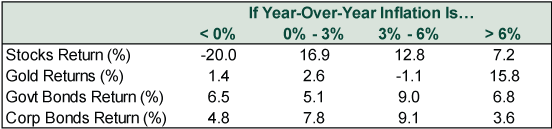

Besides these fundamental issues, history shows the rate of inflation doesn’t impede stock returns. Exhibits 1 and 2 present the median forward 12-month return and median trailing 12-month return for stocks, gold, government bonds and corporate bonds when CPI was growing or contracting at four different annual rates: under 0%, from 0% to 3%, from 3% to 6% and greater than 6%. We started our timeframe in November 1973, around the time the US exited the gold standard and the precious metal started trading freely.

Exhibit 1: Median Forward 12-Month Returns

Source: FactSet and Global Financial Data, as of 2/27/2018. Bloomberg Barclays US Aggregate Government – Treasury Total Return Index, Bloomberg Barclays US Aggregate Credit – Corporate – Investment Grade Total Return Index, Gold London PM Fixing ($/ozt) price in USD, and S&P 500 Total Return Index. All returns monthly, November 1973 – January 2018.

Exhibit 2: Median Trailing 12-Month Returns

Source: FactSet and Global Financial Data, as of 2/27/2018. Bloomberg Barclays US Aggregate Government – Treasury Total Return Index, Bloomberg Barclays US Aggregate Credit – Corporate – Investment Grade Total Return Index, Gold London PM Fixing ($/ozt) price in USD, and S&P 500 Total Return Index. All returns monthly, November 1973 – January 2018.

On a forward basis, stocks have been the top performing asset class—often by a wide margin—with one exception: inflation below 0%. Even this exception has some notable caveats. Inflation fell below 0% for only 13 months from November 1973 – January 2018. The bulk of these instances occurred in 2009—when gold was amid a big bull market and stocks’ current run-up was just getting started. This also accounts for stocks’ big -20% trailing return when inflation was under 0%, which reflects the financial crisis and last bear market.

One additional nugget to consider: Conventional wisdom argues gold is a great hedge against inflation. Yet gold’s forward-looking outperformance happened only in a period of deflation—prices falling, not rising. On the high end of the spectrum—inflation of 6% or more—gold bested both corporate and government bonds, but badly lagged stocks. Based on the trailing numbers, when higher inflation rolled around, gold’s best performance historically was already behind it. That seems to miss the purpose of a hedge.

Regardless of the inflation environment, though, stocks have frequently done well on a forward-looking basis. That isn’t to say stocks are impervious to rising prices—rather, that stocks typically rise more often than not, and inflation is only one of many economic factors influencing stock prices. That is still true regardless of whether prices are rising quickly or not. Keep this lesson in mind when media shrieks about inflation dinging future market returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today