Personal Wealth Management / Market Analysis

An Autumn Update on US Housing

Does residential real estate’s weakness portend trouble for the economy?

Will trouble in the US housing market spill over into the broader economy? Some analysts worry rising mortgage rates—tied to the Fed’s rate hikes—will leave would-be buyers unable to seal the deal, leading to an oversupply of new homes. That will then cause housing prices to crash—with alleged worrisome consequences for the US economy. However, while housing market data don’t look great, we don’t think a US recession is assured to stem from housing—and here is why.

Your first clue housing doesn’t drive the economy: the latest GDP report. Despite residential investment’s -26.4% annualized plunge in Q3, its worst reading since Q2 2020, headline GDP rose 2.6%.[i] Residential investment’s -1.4 percentage point detraction didn’t negate positive contributions from personal consumption expenditures, business investment and net trade.[ii] Now, GDP isn’t an all-encompassing economic snapshot, but in our view, its Q3 growth despite residential real estate’s big drop speaks to housing’s broader economic impact—or lack thereof.

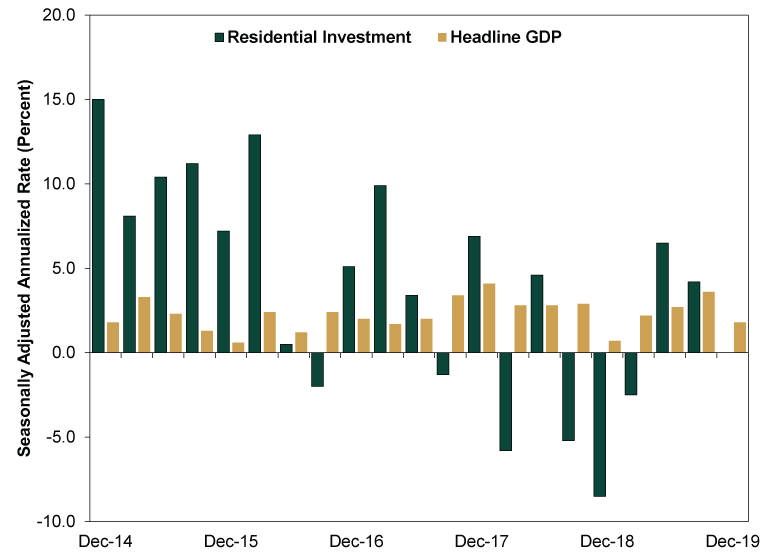

While real estate often gets eyeballs, it is a volatile subcategory that comprises about 3% of GDP—thereby lacking the scale to be a meaningful economic swing factor, in our view. Recent pre-pandemic history shows residential investment’s big swings (positive or negative) didn’t drive headline GDP. (Exhibit 1)

Exhibit 1: Real Estate’s Swings Didn’t Mean Much for GDP

Source: FactSet, as of 10/27/2022. US GDP and residential fixed investment, seasonally adjusted annualized growth rates, quarterly, Q4 2014 – Q4 2019.

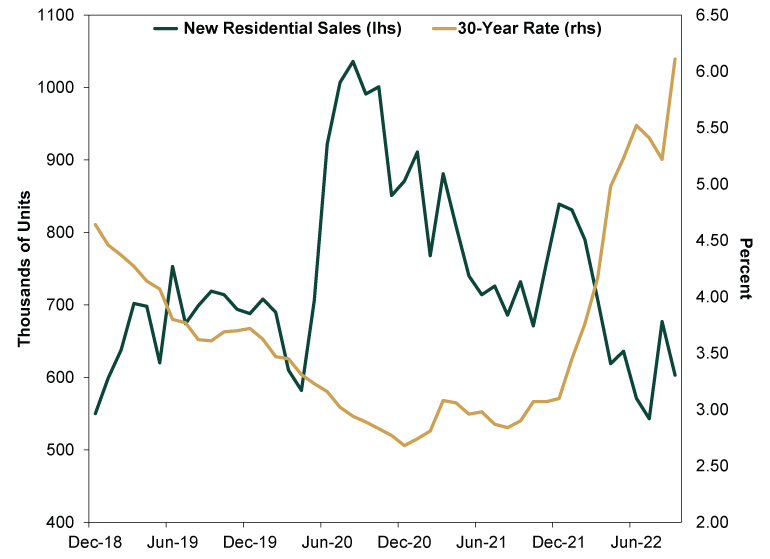

Moreover, a well-known factor is weighing on residential real estate: rising mortgage rates. Per the latest Freddie Mac survey, the average 30-year fixed-rate mortgage rose from 6.94% last week to 7.08% this week, a 20-year high. That is also up from 3.14% a year ago, and Freddie Mac’s gauge is in line with other widely watched trackers.[iii] Mortgage rates’ climb has weighed on demand, as the latest data point to sliding new home sales: September new single-family homes sales were at a seasonally adjusted annualized rate of 603,000 per the US Census Bureau, down -10.9% from August and -17.9% from September 2021.[iv]

Exhibit 2: Rising Mortgage Rates, Slowing Home Sales

Source: FactSet and Freddie Mac, as of 10/27/2022. New residential sales, seasonally adjusted annualized rate, monthly, and monthly average commitment rate on 30-year fixed-rate mortgage, December 2018 – September 2022.

Yet given the Fed’s rate hikes this year, higher mortgage rates aren’t shocking. They are also unsurprisingly denting demand, as buying a home has become less affordable for many. In response, home prices are also down, as sellers have to cut list prices in order to attract buyers with newly stretched budgets. While an imperfect indicator, the S&P/Case Shiller Home Price National Index has fallen on a monthly basis the past two months, including August’s -1.3% drop.[v]

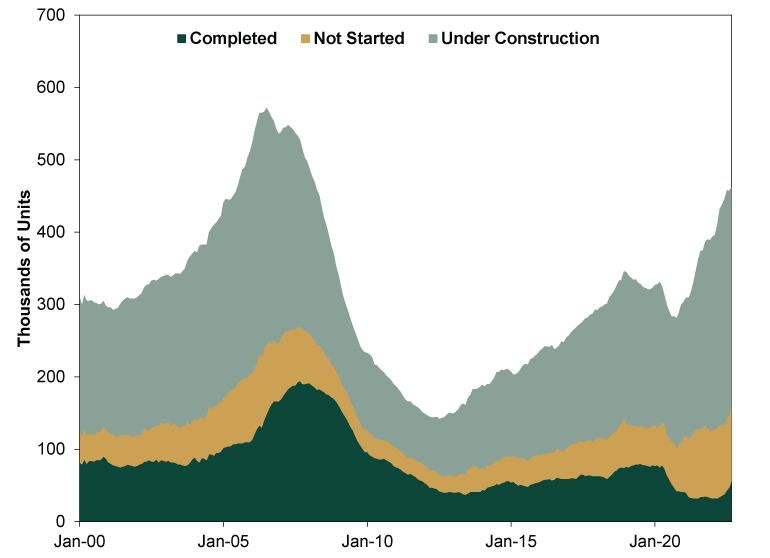

But does this weakness mean a broader housing crash? Not necessarily. In our view, it is premature to compare today’s environment to the mid-2000s, which culminated in 2006’s peak. Supply, though up, remains short of those peak levels. Take new home inventory. Supply has jumped in terms of homes under construction and homes not yet started, but completed units for sale are still below pre-pandemic levels. (Exhibit 3) Builders may choose to pause or push back construction depending on their anticipated supply and demand dynamics—so a huge influx of new supply from here isn’t assured.

Exhibit 3: A Look at New Housing Inventory

Source: US Census Bureau, as of 10/27/2022. New privately owned houses for sale by stage of construction, January 2000 – September 2022.

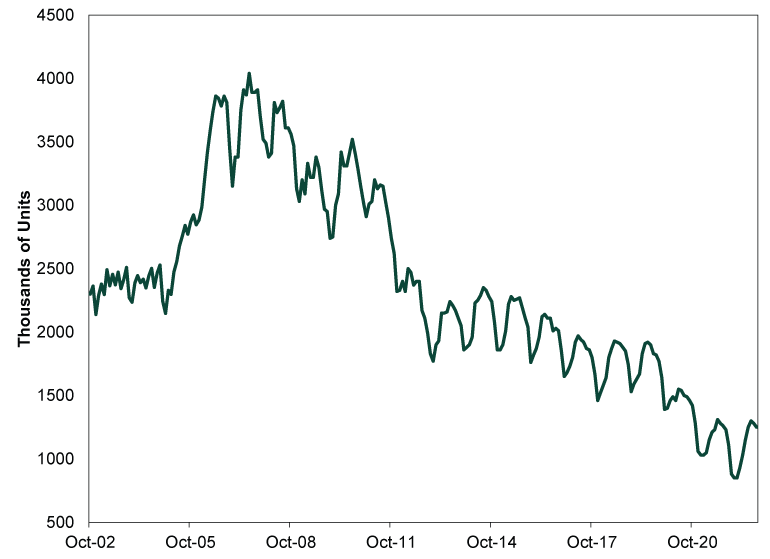

Moreover, existing home inventory remains historically low—another sign supply hasn’t exploded like it did in the mid-2000s.

Exhibit 4: A Look at Existing Homes Inventory

Source: FactSet, as of 10/27/2022. National Association of Realtors inventory of existing homes for sale, not seasonally adjusted, October 2002 – September 2022.

Note, new housing construction is real estate’s primary contribution to GDP. In our view, the decline in housing investment reflects the latest shifting supply and demand dynamics—which have already started showing up in GDP. If the big recent housing declines haven’t driven deep GDP declines at this point, it seems unlikely to us that they will in the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today