Personal Wealth Management / Market Analysis

Are July’s Business Surveys Normal?

Why the latest PMIs may not be as troubling as headlines think.

Has a summertime swoon arrived? July business activity contracted in major developed economies, including the US and eurozone, per the latest surveys. We aren’t Pollyanna about today’s global headwinds, but it is critical to ask whether any of this information is surprising to markets—and in our view, the answer is no. Despite all the headline handwringing, July’s purchasing managers’ indexes (PMIs) don’t reveal much new on the economic data front—stocks likely reflect this weakness to a large extent already.

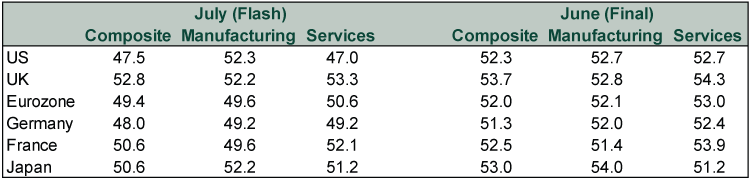

As Exhibit 1 shows, S&P Global’s July “flash” PMIs weakened across the board from June and missed expectations.

Exhibit 1: The Latest PMIs<

Source: FactSet, as of 7/22/2022.

PMIs below 50 indicate contraction, so unsurprisingly, headlines focused on the US and eurozone. The US July composite PMI, which aggregates services and manufacturing output, contracted for the first time since June 2020. Moreover, the sub-50 services PMI spurred slowdown concerns since the sector comprises the lion’s share of US output. Across the Atlantic, the eurozone composite PMI fell below 50 for the first time since February 2021. Those forecasting regional economic struggles trumpeted July’s dip in manufacturing and services new orders—a forward-looking indicator since today’s orders are tomorrow’s production. Manufacturing new orders in particular were down a third straight month. The alleged takeaway from July: Global growth is losing momentum as pent-up services demand fades amid rising prices, and the eurozone appears to have an even higher likelihood of entering recession.

Now, we think it is important to analyze the data objectively, and July’s flash PMIs highlighted some well-known weak spots. For example, elevated inflation has dominated headlines globally, with consumer price measures in the US, UK and eurozone at multi-decade—even record—highs. Higher prices weigh on households and businesses, forcing them to make do with less or cut expenses. As the German July flash PMI noted, “… inflation … was a notable feature behind the worst performance of private sector activity since the height of the first pandemic wave in the spring of 2020.”

But looking more broadly, July PMIs parallel recent economic data, which have been mixed. In early June, we observed an emerging trend in European economic data—a divergence between “soft” data (e.g., PMIs) and “hard” data (e.g., industrial production). While PMIs were broadly expansionary, industrial production and retail sales had many setbacks. Now PMIs are mixed, and it is possible hard data could worsen.

However, we counsel investors to keep some context in mind. One, hard data come out at a lag. The latest eurozone industrial production and retail sales data cover May, and July figures won’t arrive until September. Even if they confirm weak July PMIs, it will be old news by then, long priced in by forward-looking stocks. Two, monthly data can be volatile, so extrapolating July’s figures forward is a mistake, in our view.

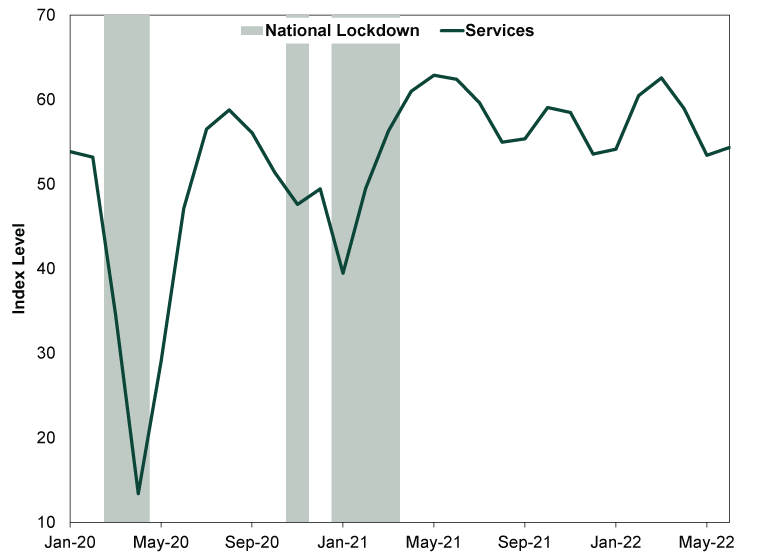

Moreover, July’s PMI weakness may actually be a return to normal. Economic data globally have followed a well-known trend during the pandemic: Lockdowns roil output, but once they ease, the data jump as economic activity returns. However, the subsequent boom doesn’t last for long, and activity eventually slows—as illustrated by the UK services PMI over the past two-and-a-half years.[i] (Exhibit 2)

Exhibit 2: UK Services PMI, January 2020 – June 2022

Source: FactSet, as of 7/26/2022. S&P Global services PMI for the UK, January 2020 – June 2022. Readings above 50 imply expansion.

Taking a longer view, the latest PMIs may not be warning signs of economic trouble, but rather, a return to growth trends that dominated before COVID. That era’s slow growth was just fine for stocks.

Now, we acknowledge myriad headwinds accompany and complicate a return to normal. It is possible ongoing developments (e.g., Europe’s energy crunch) weigh on growth and may even drive some individual country or regional GDP contractions. But stocks are already behaving as we would expect if a shallow recession were in the offing. If the data confirm a mild downturn, the negative surprise power would likely be next to nil, in our view—stocks have been digesting the myriad forecasts of a recession tied to inflation, high energy prices and other widely discussed headwinds for a while. Unless a much larger-than-expected downturn lurks—which doesn’t look likely to us right now—the global economy’s fundamentals aren’t in as dire straits as broadly discussed. That “less bad” outcome can boost stocks if expectations are as low as they are right now.

[i] We use the UK services PMI for two reasons. One, COVID restrictions disproportionately impact services, which has more people-facing industries. Two, the UK government implemented three national lockdowns between early 2020 and early 2021, providing multiple examples of lockdowns’ big, but fleeting, economic impact.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today