Personal Wealth Management / Market Analysis

As the Fed’s Dot Plot Thickens, Skip the Puzzlement

Forecasts are only ever opinions, and the Fed’s aren’t very clear.

Days after the Fed ratcheted rates higher again last Wednesday, chatter over policy moves continues, as stocks hover near new bear market lows. But most talk now isn’t about the hike itself—that wasn’t exactly a shock. Rather, consternation about where policy is heading has many fearing much more tightening to come, roiling sentiment. As evidence, they point to the Federal Open Market Committee (FOMC)—the Fed’s monetary policy decision-making body—boosting its dot-plot projections for rates’ “appropriate policy path” this year and next. But, in our view, while future policy moves could spur volatility, they don’t dictate market direction—and today’s dot plot doesn’t determine tomorrow’s hikes.

As expected, the Fed raised its fed-funds rate target range 0.75 percentage point for the third straight time to 3.0% – 3.25%. But this was mostly a forgone conclusion, with interest rates largely pre-pricing the move ahead of time. So instead, most observers focused on the unanswerable question: How high does the Fed think rates need to go to break inflation’s back? To suss that out, interested parties pored over reams of Fed prognostications released with its rate announcement—the quarterly Summary of Economic Projections (SEP). Bundled within it: a dot plot showing what FOMC participants think rates’ path should look like over the coming years. The midpoint of members’ latest guesstimates for this year jumped to 4.4% from the prior SEP’s 3.4% in June.[i] Next year, supposedly, the fed-funds rate will hit 4.6%, up from June’s thinking it would be 3.8%. So it might seem at least another percentage point of rate hikes are baked in.

But slow down. The dot plot’s evolution over the past year proves you can’t take these forecasts as gospel. In December 2021, the SEP’s dot-plot midpoint had rates ending 2022 at 0.9%.[ii] They were collectively expecting to barely lift rates at all this year. Three months later, March’s dot plot put the fed-funds rate’s 2022 close at 1.9%. Now it has more than doubled. We don’t see these projections as forward guidance in any useful sense. All they do is show the FOMC members’ evolving opinions. They underscore that even Fed officials can’t forecast what policy they think will be appropriate. And they decide the rates. If they can’t foretell future policy decisions, what chance do outsiders have?

Seemingly in recognition of forward guidance’s limitations—and forecasting’s difficulties generally—Fed head Jerome Powell forswore giving any in late July. Rather than provide specific direction on the likely size of the Fed’s next move—as he had at all 2022’s FOMC meetings thus far—he elected not to, stating that, “While another unusually large increase could be appropriate at our next meeting, that is a decision that will depend on the data we get between now and then.”[iii] He further noted, “We will continue to make our decisions meeting by meeting, and communicate our thinking as clearly as possible.” A month later at the Fed’s Jackson Hole central bank symposium, Powell slipped the hint: “July’s increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook.”[iv]

Although Fed officials take pains to remind people they are “data dependent,” not only is their forward guidance—when they offer any—provisional, they don’t always tell you what those provisions are. Even when they do, that can change on a whim, too. Remember when inflation was, in Powell’s words, “transitory?” It was until it wasn’t—or, more accurately, until Powell felt the word had outlived its usefulness. The thing here is that besides word choice unpredictability, what those words mean is open to interpretation, let alone whether they are even correct or not. Then, whatever Fed people say, you can’t rely on them doing anyway.

In any event, we don’t think you need to forecast Fed actions—or agonize over its projections. The Fed’s economic influence is much less than most think and typically hits with a lag of around 6 to 18 months. So for instance, inflation, inflation expectations and Fed responses to them so far have fed into higher borrowing costs—mortgage rates among them. As numerous articles point out, this is starting to stunt housing activity, which looms large in many folks’ minds. But what is its likely economic impact, really? Q2 residential investment was only 3% of GDP.[v] That is likely why the Atlanta Fed’s GDPNow estimate of Q3 output shows slight growth despite a forecast -24.5% annualized residential investment decline.[vi] Despite the common narrative around 2008, a housing downturn alone isn’t likely to drive a deep recession.

A look at how monetary policy works also shows why the current rate hike campaign is overrated. The main way Fed policy transmits to the economy is through bank lending—but there has been an unappreciated disconnect here. Normally, when the Fed hikes its short-term rates, banks raise their deposit rates in near lockstep. But as you may have noticed, savings accounts are averaging 0.17% nationally—not close to 3%.[vii] This is important since the interest banks pay on their deposits represent their funding costs on new loans they make. The difference between what they take in from their lending rates and what they pay out on deposits is their net interest margin.

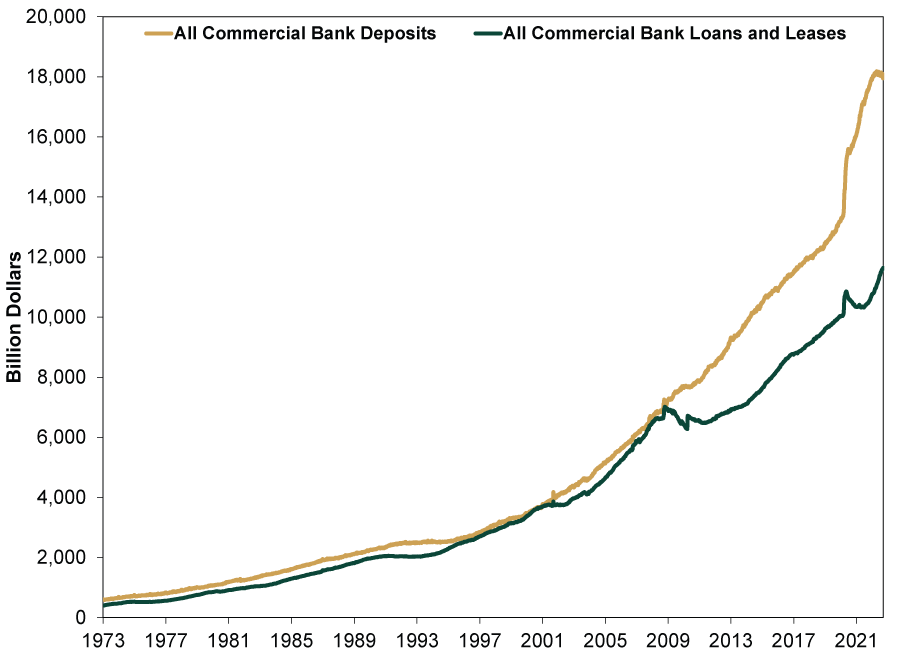

Why the disconnect between fed-funds and deposit rates? See Exhibit 1. Banks are flooded with deposits. They have more than they know what to do with and don’t have to compete to attract funds.

Exhibit 1: Banks’ Deposit Flood Short Circuits the Fed’s Main Policy Transmission Mechanism

Source: Federal Reserve Bank of St. Louis, as of 9/26/2022. Deposits and loans and leases in bank credit for all commercial banks, 1/3/1973 – 9/14/2022.

With banks’ funding costs still effectively zero and 10-year benchmark Treasury rates hitting new highs—they are at 3.9% today—net interest margins are widening.[viii] Greater loan profitability is an incentive to increase lending. This isn’t theoretical. Total bank loan growth accelerated to 11.3% y/y through September 14, just shy of its May 2020 11.6% pandemic-lockdown peak rate without any emergency government support.[ix] This could change, but as of now it seems quite inconsistent with a deep recession.

The Fed has some influence over the economy, but it is far from all-powerful. More often than not, we find it mostly befuddling—which is fine. We don’t think there is any need to decipher its decision-making twists and turns. However, reactions to those may be helpful divining broad market sentiment. Dour expectations in that regard lately suggests reality is probably better than widely perceived.

[i] Source: Federal Reserve, as of 9/21/2022.

[ii] Ibid.

[iii] “Fed’s Powell’s Absence of Specific Guidance Leaves Analysts to Fill the Gaps,” Ann Saphir, Reuters, 7/27/2022.

[iv] “Monetary Policy and Price Stability,” Jerome Powell, Federal Reserve, 8/26/2022.

[v] Source: Bureau of Economic Analysis, as of 9/26/2022.

[vi] Source: Federal Reserve Bank of Atlanta, as of 9/26/2022.

[vii] Source: Federal Reserve Bank of St. Louis, as of 9/26/2022.

[viii] Ibid.

[ix] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

-

Expert Commentary This Week in Review | Record Highs, US Jobs, Yen Intervention

2026-08-07

2026-08-07 -

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Politics The Tenth Question Facing Alberta2026-08-06

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today