Personal Wealth Management / Market Analysis

Canary in the Coalmine?

A certain auto company’s layoffs aren’t a leading economic indicator.

Editors’ Note: MarketMinder does NOT recommend individual securities. The below simply represent a broader theme we wish to highlight.

We don’t normally delve into company-specific items in this space, but this week, a story about a venerated American company has gone viral, sparking worries its woes foretell worse to come for the US economy. That news: GM’s announcement of factory closures and layoffs—tragic and painful news for those impacted. Headlines claimed this was bigger, though—that US manufacturing growth had peaked and the expansion was on the wane. Lost in the hoopla is the fact the firm is dealing with company- and industry-specific issues that likely have little to do with the broader economy. This highlights a timely and timeless lesson for investors: Beware anecdotal evidence writ large.

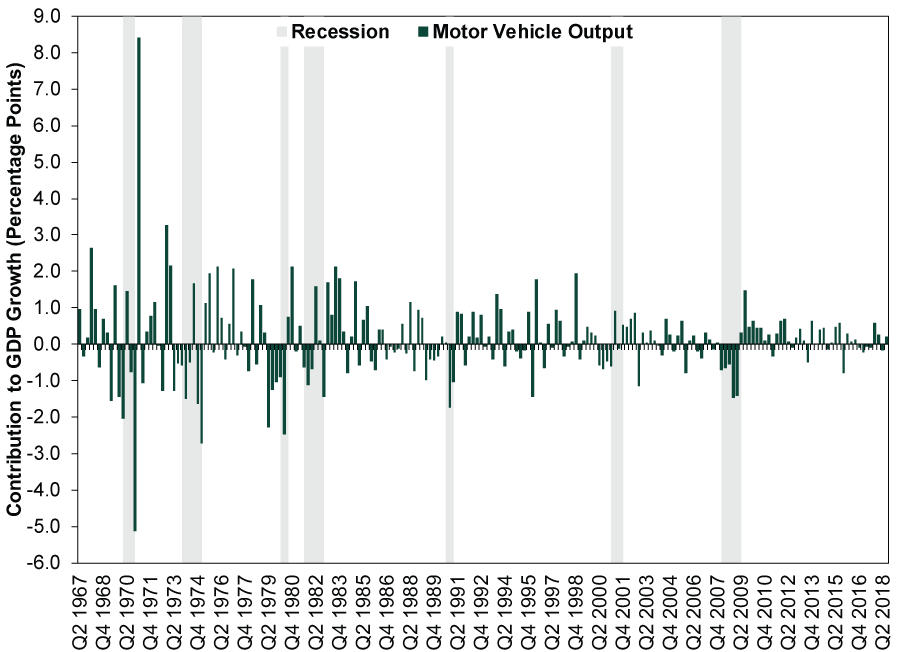

We won’t dwell on GM’s struggles, but in short, it is presently undergoing a global restructuring. It isn’t closing plants and ceasing production immediately because it is in deep trouble. Rather, it is planning to shut plants that produced low-selling models like Chevy’s plug-in Volt and large-sedan Impala after next December. If anything, this is a statement about the difficulty of marketing electric cars when oil is cheap and shifting consumer tastes. Yes, its sales decline coincided with a broader slide in auto sales, but as Research Analyst Luke Puetz explained here last month, auto sales usually taper off in a maturing economic cycle. Moreover, motor vehicle output is less than 3% of GDP.[i] As Exhibit 1 shows, it often wobbles during expansions. So we have a hard time seeing how one can draw sweeping, forward-looking conclusions from a couple of plant closures scheduled for a year from now.

Exhibit 1: Auto Output Doesn’t Drive the Economy

Source: Federal Reserve Bank of St. Louis, as of 11/27/2018. Motor vehicle output’s contributions to real GDP growth, seasonally adjusted annualized rates, Q1 1967 – Q3 2018. Recession dating from the National Bureau of Economic Research.

It is completely, totally normal for individual companies to hit speedbumps during an expansion. Even old, well-known names like GM. Intel laid off 12,000 workers in 2016. Readers over age 25 might remember Apple nearly failing in the go-go late-1990s. Marvel Comics nearly went bust a couple years before that. Merck had a big spot of trouble in the mid-2000s due to the Vioxx scandal. Netflix hiccupped badly in 2011 with a botched business plan. None of these were signs of things to come any more than GM—or, for that matter, Toys ‘R’ Us and Sears are today. Sometimes a glitch is just a glitch. Yes, troubles as we’ve seen at GM do sometimes come in waves, but that usually happens after a recession has started—in other words, cascading corporate problems are a symptom of a downturn, not a cause.

When bad corporate news comes out during a burst of market volatility, it is easy to draw connections. But coincidence isn’t causality. Layoffs like GM’s are a constant, regardless of economic conditions. No month in recorded history has featured zero layoffs.[ii] Jobless claims have never hit zero. The lowest month for layoffs and firings, September 2016, still saw over 1.5 million folks lose their jobs.[iii] It is awful for those impacted, especially if they can’t find new work right away. But it is simply not an economic driver or leading indicator.

Mistaking one-off developments for trends is an error, regardless of the subject matter. It is easy to hold one poster child up as evidence of widespread issues. That is a common tactic throughout the media these days, in financial and sociological news alike. But GM doesn’t seem like a harbinger of US recession any more than Germany’s contracting GDP in Q3 is a sign of a global pullback. The world is always full of blips and noise. Recognizing these for what they are is a critically important skill for investors to develop.

[i] Source: US BEA, as of 11/27/2018.

[ii] This statement is accurate whether you choose to base it on the narrow Challenger, Gray and Christmas planned layoff data (which date back to January 1993) or the Federal Reserve’s broader Job Openings, Layoffs and Turnover data, which start in December 2000.

[iii] Source: Federal Reserve Bank of St. Louis, as of 11/27/2018. Layoffs and discharges: total nonfarm, September 2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today