Personal Wealth Management / Market Analysis

Debunking the Junk Funk

Is the high yield bond market giving clues about stocks' future?

Does junk bonds' funk mean stocks are sunk? Some suspect so, as the US high yield corporate debt (i.e. junk bonds) market's recent sell-off has prompted speculation other assets-namely stocks-are about to go on a bumpy ride. Folks fret bonds are sending a warning signal that stocks are turning a blasé eye toward. However, we don't believe bond markets possess any special insight over equity markets-both look forward and discount widely known information. Though short-term volatility can hit any sector, region and/or market for any (or no) reason, in this case, one fundamental driver seems to be behind junk bonds' bumps: falling energy prices. While those may hit some individual firms, we don't think the macroeconomic or broad market impact is big enough to end the bull market. Or even totally negative.

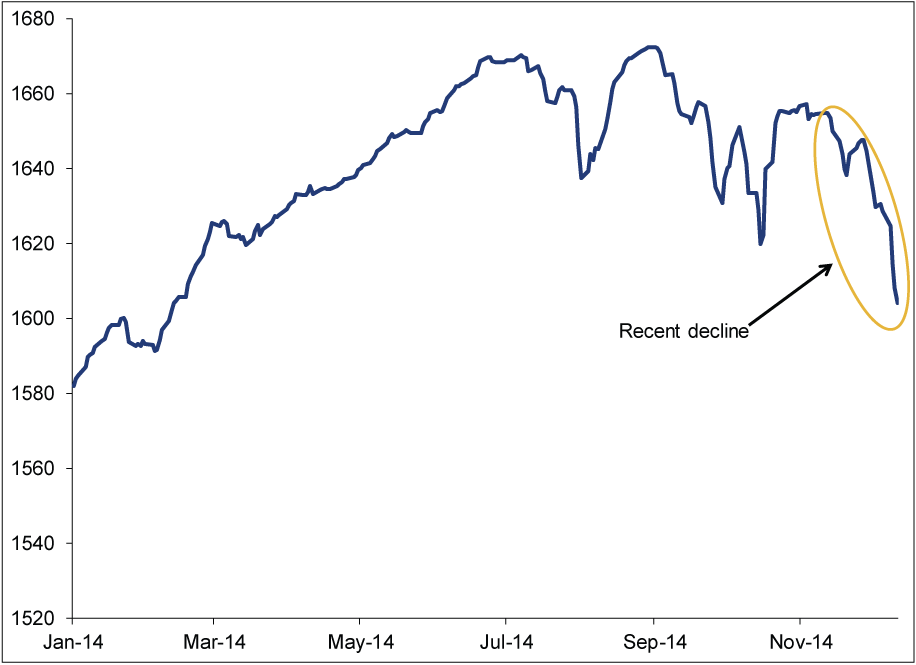

Junk bonds have had a nice run since the financial crisis ended, with one gauge-the Barclays US High Yield Index-rising more than 160% from its 2008 low through the end of 2013. 2014 was off to another nice start, adding 5.7% through September 1. But since then, junk bonds have hit some tougher sledding, falling 4% through December 11, with most of the decline coming recently. Here is a chart.

Exhibit 1: Barclays US High Yield Index YTD

Source: FactSet, as of 12/12/14. Barclays US Aggregate Credit Corporate High Yield Index, 12/31/2013 - 12/11/2014.

The dip is not lost on the media, who've rather predictably responded with headlines like these:

- "Junk-Bond Contagion Fears Rise as Oil Extends Drop."

- "Oil-Driven Junk-Bond Selloff Spreads as Risk Gauge Climbs."

- "Fed Bubble Bursts in $550 Billion of Energy Debt: Credit Markets"

- "Junk Bonds Breaking 5-Year Support: Stocks to Follow?"

Some pundits fret equity investors are ignoring the clear warning signal bonds are (allegedly) sending. The rationale (a familiar one) is: Since corporate bonds and stocks possess similar drivers, it seems logical to expect them to move similarly. Which is true to a large extent, but it doesn't make one predictive of the other's moves-no asset class is more insightful than another. All markets price in widely known information, at roughly the same time, to varying degrees.

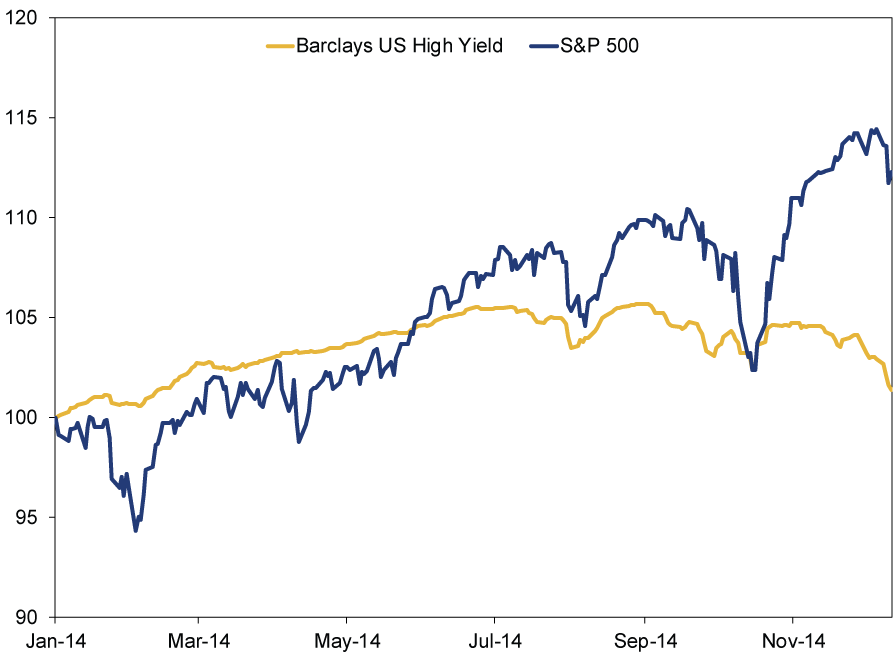

For instance, consider how bond and stock markets reacted to former Fed Chair Ben Bernanke's telegraph of the quantitative easing (QE) taper in May 2013. The 10-Year Treasury yield jumped up more than half a percentage point in a month, from 1.94% to 2.52%-a large jump considering the low level it rose from. The S&P 500 likewise bounced around following Bernanke's announcement, falling about 4% in the two weeks. Whatever is driving one market is known-and probably priced-in the others too, though how markets process that information (particularly in the short term) can vary. As Exhibit 2 shows, the S&P 500 and Barclays US High Yield Index seem to move more or less concurrently, though not to the same extent.

Exhibit 2: Barclays US High Yield vs. S&P 500 YTD (Indexed to 100)

Source: FactSet, as of 12/12/2014. Barclays US Aggregate Credit Corporate High Yield Index and S&P 500 Total Return Index, 12/31/2013 - 12/11/2014.

That said, much of the junk bond market's recent volatility seems driven by falling energy prices. Driven by fast-rising supply, West Texas Intermediate (WTI) crude prices have fallen nearly 45%, from $104.29 on July 30-the last time prices topped $100-to $57.49 today[i]. Because Energy companies' revenues and earnings tend to be highly price sensitive, this lower price environment likely weighs a bit on future profits.

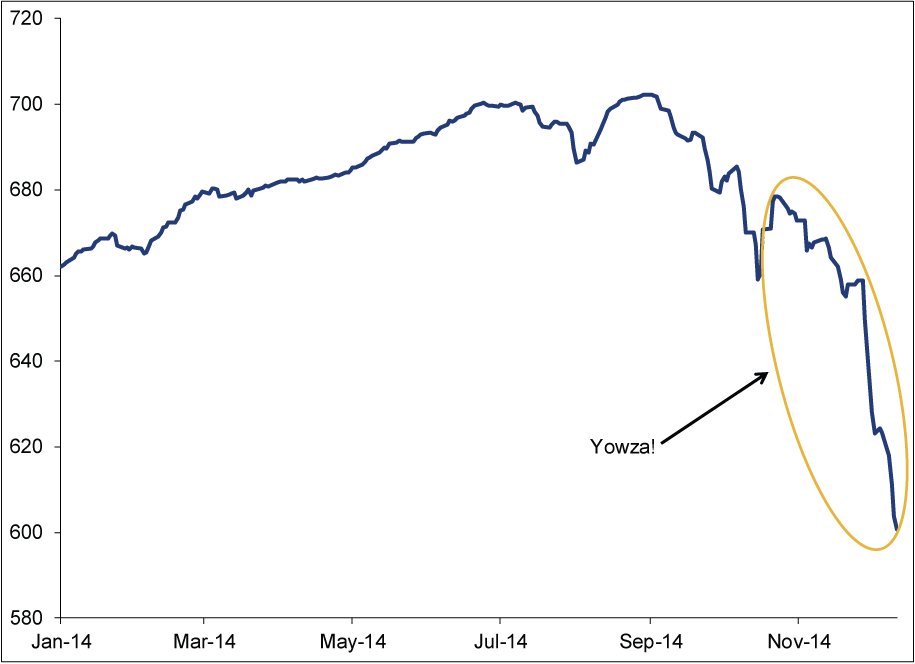

Why is this relevant? The Energy sector comprises about one sixth of the overall junk bond universe-so its recent decline (Exhibit 3) has an outsized impact on overall performance. In fact, only two-out of 13(!)-major industries represented in the Barclays US High Yield Index are down year to date (Exhibit 4). The biggest laggard by far: Energy, at -9.3%.

Exhibit 3: Barclays US High Yield Energy Index YTD

Source: FactSet, as of 12/12/2014. Barclays US Aggregate Credit Corporate High Yield Energy Index, 12/31/2013 - 12/11/2014.

Exhibit 4: Barclays US High Yield YTD Sector Returns

Source: FactSet, as of 12/12/14.

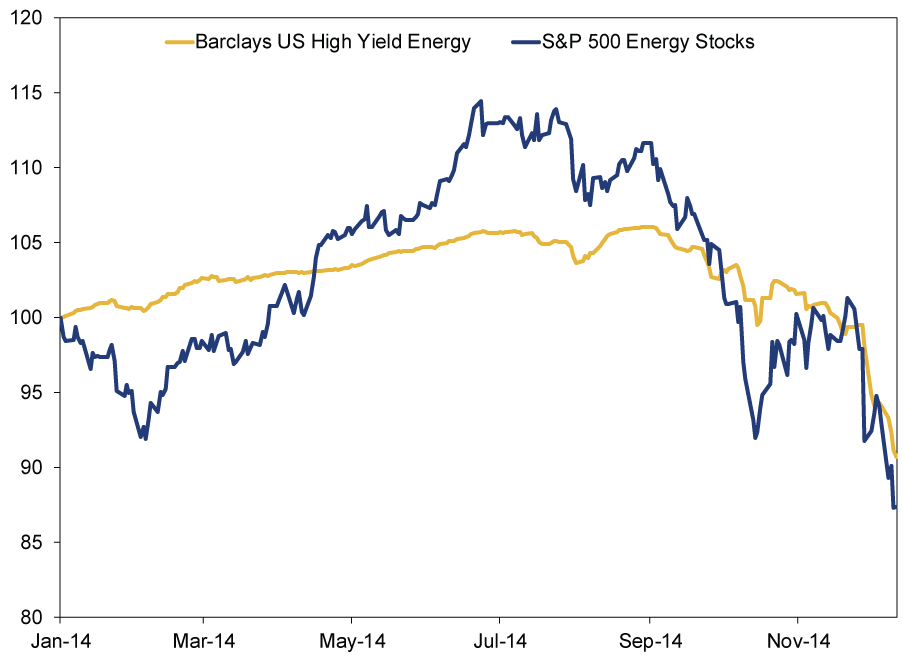

Falling oil prices haven't just hit the high yield bond market. Energy stocks have felt the crunch too!

Exhibit 5: S&P 500 Energy and Barclays US High Yield Energy (Indexed to 100)

Source: FactSet, as of 12/12/2014. Barclays US Aggregate Credit Corporate High Yield Index and S&P 500 Total Return Energy Index, 12/31/2013 - 12/11/2014.

Both bonds and stocks are pricing in this fundamental driver-but because Energy has only an 8% weight in the S&P 500-about half its weight in the Barclays High Yield Index-the implications are more widely felt there.

A separate fear sprouting from junk bonds' decline: Falling oil prices will drive much of the roughly $200 billion in Energy junk bonds to default, hitting banks and causing a financial crisis. In our view, this is overstated. Some firms may feel the pinch if oil prices stay low for a sustained period. Some may even default-it's possible. Yet that needn't trigger a wider panic throughout the US Energy sector (and high yield bond market at large).

For one, the industry is familiar with oil price volatility and accounts for it through hedging (e.g. using forward contracts to lock in higher prices for the near future). Consider: WTI prices fell 34% over five months in 2011. In 2012, they rose 27% in under three months. Oil's recent tumble may slow or shut down some operations, like exploratory efforts, but the industry at large isn't imperiled. Also, technological advances have made hydraulic fracturing more efficient and economical, and many firms can remain profitable if oil prices fall even lower. Plus, while oil prices are certainly a powerful input for Energy firms' profits, they are not the only factor. Many of the Energy firms folks fret have non-oil related earnings-like natural gas-and Henry Hub gas prices are up year over year, reducing some pressure.

So while rising yields for junk (specifically Energy junk) debt are a signal investors want more compensation for the risk, that doesn't mean the entire sector-let alone market-is in trouble. But even if it did, troubles in the $200 billion Energy high yield market are likely insufficient to quash the expansion and bull market. As we've written, lower Energy prices likely create some losers and some winners.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] Source: The Wall Street Journal. As of 12/12/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Quick Hit: The July Jobs Nothingburger2026-08-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today