Personal Wealth Management / Market Volatility

Enjoy the Calm, but Don’t Forget Volatility

Stocks inevitably encounter rough patches; we don’t know when, so the time to prepare mentally is now.

In late April and again in early July, we showed you that markets have been relatively calm in 2021, despite an ocean of fearful headlines. That relative calm has continued through today. Now, that long quiet period doesn’t mean stocks’ smooth stretch is about to be shattered. Volatility can strike or vanish at any time for any or no reason. But we do think getting acquainted with this year’s lack of volatility relative to the norm can help you mentally prepare for whenever markets do hit turbulence.

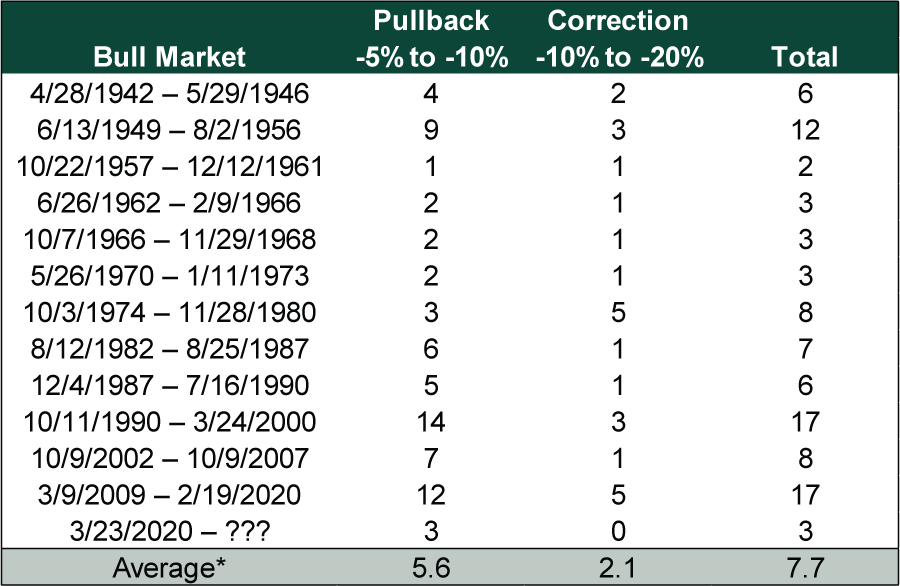

So far in 2021, the S&P 500 has had no pullbacks—declines from a prior high—exceeding -5%.[i] Although there is great variance among bull markets, as Exhibit 1 shows, the 12 postwar bull markets (before the current one) have averaged about 8 sizeable declines each. By magnitude, there are typically a handful of -5% to -10% pullbacks and a couple of -10% to -20% corrections. There are always outliers, but as the current bull market wears on, it would be unusual not to see more volatility and pullbacks.

Exhibit 1: Frequency of Pullbacks Exceeding -5%

Source: Global Financial Data, Inc. and FactSet, as of 9/1/2021. S&P 500 price index, 4/28/1942 – 8/31/2021. *Not including the current bull market.

Another way to see this is to slice the data annually. With 95 pullbacks and corrections since 1942, that is about 1.5 per bull-market year on average. Again, having none this year—so far—is notable, though it says nothing about their likelihood going forward. Still, in our view, there is no time like the present to think through the investment implications of negative volatility returning: how it might knock you off course and what you should do to avoid potentially counterproductive portfolio moves.

While they are regular occurrences, substantial pullbacks draw reams of attention—and pundits’ explanations about why more trouble must lie in store. But letting this influence your portfolio decisions generally isn’t beneficial. If you can identify a bear market—a typically lasting, fundamentally driven decline exceeding -20%—early enough, taking action can help, allowing you to sidestep negativity and buy back in at lower levels later. (More on this to come.) But sentiment-driven wiggles are much more common. Timing them is flawed strategy, in our view. You would be selling after a decline, locking in losses in fear of further bigger declines later. Those may come, perhaps offering momentary comfort, but think of your time horizon—the period you need your portfolio to reach your investment objectives.

If your time horizon is more than a few years (and we think equity investors should have longer time horizons than this), moving to the sidelines can set your financial goals back. You might miss upside, if you time your reentry incorrectly, which can jeopardize longer-run returns. In our view, this is an unnecessary risk. Sentiment-driven market moves—including periodic volatility, pullbacks and corrections—are usually short-lived next to bull markets’ long-term upward trend. Stocks’ long-term returns include all of them. Staying invested through occasional dips is generally the way to go, in our view. But we recognize in the moment, it can be extremely hard! This is why we think it helps to go through past episodes once in a while and envision the correct course through them.

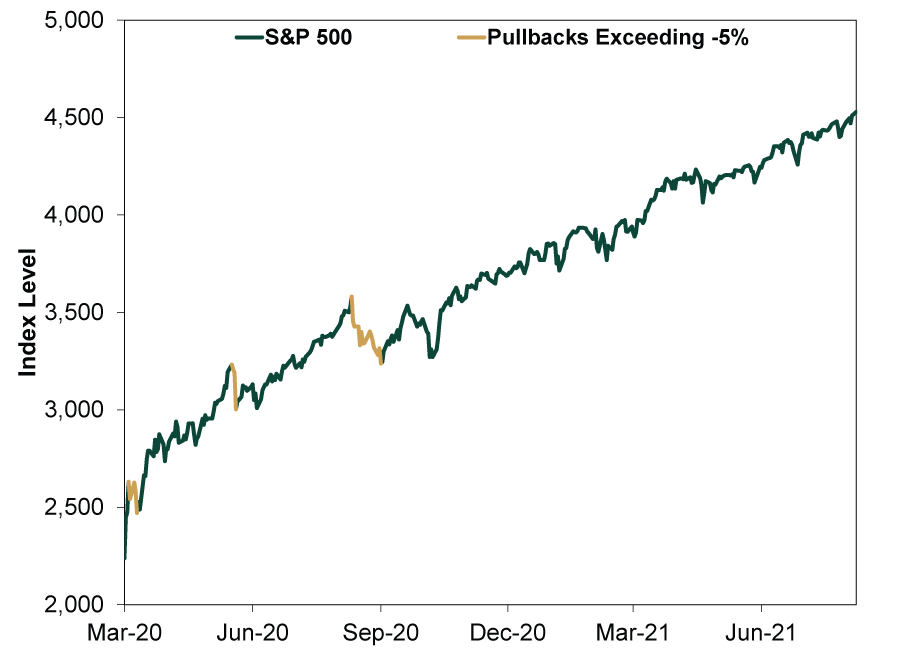

Consider a couple of recent bull market wobbles. The last big drop occurred last September, when the S&P 500 fell as much as -9.6%, tied to second-wave fears and election worries.[ii] (Exhibit 2) By mid-October, stocks had mostly recovered, but then they dropped almost as much by Halloween. After November’s vaccine progress announcements (and presidential election) stocks erased the decline.

Exhibit 2: Major Pullbacks During the Current Bull Market So Far

Source: FactSet, as of 9/1/2021. S&P 500 price index, 3/23/2020 – 8/31/2021.

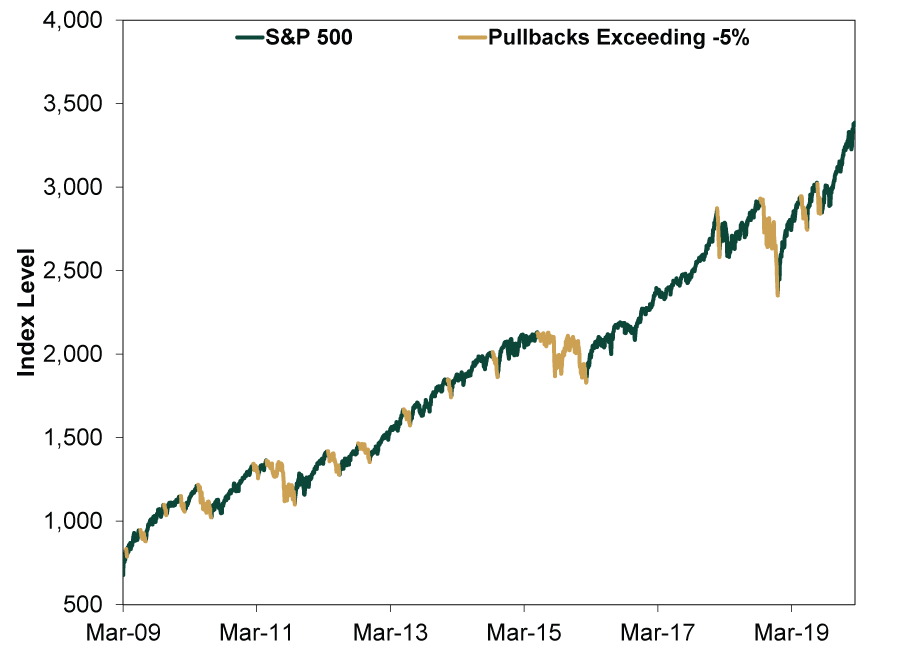

Before then, there was late-2018’s deep -19.8% correction (Exhibit 3), which pundits argued was caused by Fed rate hikes, rising bond yields, US-China trade tensions or weak economic data.[iii] Or or or. In our view, a raft of hedge fund liquidations was the primary culprit, which weighed on sentiment. But like all sentiment-fueled moves, it proved fleeting despite the magnitude. The best course of action? Soldiering through the fraught headlines and blaring alarms.

Exhibit 3: Major Pullbacks During the 2009 – 2020 Bull Market

Source: FactSet, as of 9/1/2021. S&P 500 price index, 3/9/2009 – 2/19/2020.

Most of the time, stocks aren’t making new highs day in and day out, even in the strongest bull markets. Look at any line graph of a bull market, and you will see it isn’t a straight ride up—it is jagged. Stocks always zig-zag. Just as the upward zigs during a bear market lull people into complacency, the downward zags during a bull market stoke fear. But how do you discern a bear market from a bull market correction, especially in the early innings? First and foremost, bear markets start one of two ways: either widespread euphoria inflates expectations and blinds investors to broadly worsening economic conditions, or a wallop coming out of the blue knocks the global economy into recession. Last year’s global lockdown was a wallop, one that caused a bear market in record time, too. The 2000 dot-com bubble was classic euphoria. In both cases, there is a wide gap where expectations overran reality. A bear market closes the gap and then some.

Early on though, before an identifiable cause is obvious, stocks may be zigging and zagging without clear direction. We find following a few bear market rules can help identify them—and avoid mistakenly identifying them:

- The 2% rule: Bear markets characteristically begin with rolling tops. At their start, they decline gradually, on average by -2% a month. Sharp, sudden dives, while scary, typically rule out a bear market, with last year being the exception.

- The three-month rule: Even if you suspect the bull market has peaked, wait three months before taking defensive action. Can you identify a fundamental cause few others see? Is the pace of decline gradual or swift? The first question is core to whether you have a reason to take action; the latter can help you discern typically swift corrections from normally gradual bear markets.

- The two-thirds/one-third rule: Ordinarily, about one-third of a bear market’s decline occurs during the first two-thirds of its duration. The most damage, around two-thirds of it, occurs in its final third.

Otherwise, as Fisher Investments’ founder and Executive Chairman Ken Fisher says: If it isn’t a bear market, it is a bull market.

The key for investors is being invested when stocks are forging higher—like now, when the S&P 500 is up 21.6% on the year.[iv] In our view, that means staying in the market during run-of-the-mill volatility—or corrections.[v] Being out when the market is up not only incurs opportunity costs—missed returns that could have improved progress toward your investment objectives—but mental ones as well. Missing upside can be just as painful as experiencing declines.

It can be beneficial to try and cut out part of bear markets’ downside, if you like, but even then—like last year showed—doing so isn’t necessary in order to reap stocks’ longer-term returns. In our view, investors’ biggest risk isn’t a bear market—much less pullbacks or corrections—but not attaining their financial goals. Achieving market-like returns to fund retirement and other expenses generally requires being invested in stocks the vast majority of the time.

Enduring volatility and pullbacks when they come is critical to long-term investing success. Better to absorb that lesson now to help withstand rocky patches when they inevitably occur.

[i] Source: FactSet, as of 9/1/2021. Statement based on S&P 500 price index, 12/31/2020 – 8/31/2021.

[ii] Ibid. Statement based on S&P 500 price index, 9/1/2020 – 9/23/2020.

[iii] Ibid. Statement based on S&P 500 price index, 9/20/2018 – 12/24/2018.

[iv] Ibid. S&P 500 total return, 12/31/2020 – 8/31/2021.

[v] One frequent reader has suggested we rename corrections “regressions,” as corrections wrongly imply the down move is somehow “correct” or “right.” We like the suggestion, although we doubt our ability to change the financial lexicon unilaterally.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today