Personal Wealth Management / Market Analysis

Is China Experiencing the World's Biggest Credit Bubble?

Nope-and here is why.

China credit bubble concerns are one of the oldest, most recycled false fears of today's bull market. Bubble-warning headlines from seven years ago could run today with minimal changes. However, despite numerous examples of Chinese credit not being properly allocated-a side effect of the government's centralized control-no bubble has burst yet. Unless a massive negative surprise creates a wallop or euphoria creeps back into markets, the likelihood a Chinese credit bubble pops and roils the economy-with ill effects spreading globally-in the immediate future is low, in my view.

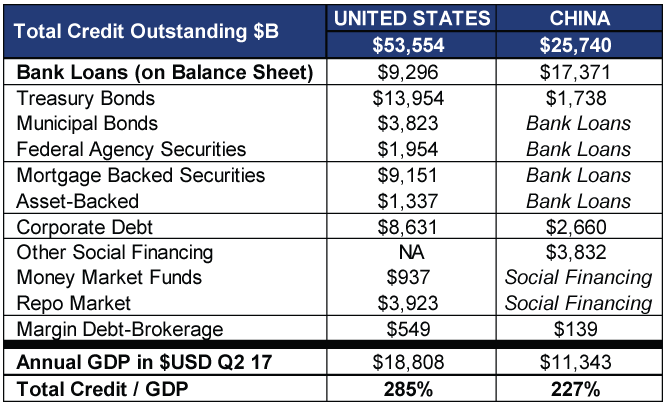

To understand why Chinese credit bubble fears are overwrought, investors must first understand some critical differences between how credit works in China's centralized, government-steered economy and a typical free market economy (like the US). China's Communist Party exhibits heavy control over economic areas like capital flows, currency strength, interest rates and money supply. This desire for control-particularly over money supply-means China relies on banks to provide the majority of credit access (67% compared to 17% in the US[i]). In comparison, entities in the US have more options thanks to America's deep, robust capital markets (e.g., bond, asset-backed security, short-term commercial paper and repo markets).

While bank-driven credit gives the government more control over money supply, Chinese banks must make loans that capital markets would typically underwrite in the US. For example, Chinese banks make lots of loans to the government, but in the US, the federal government can issue Treasurys while states and cities float muni bonds. Also in the US, mortgage and asset-backed securities comprise a nearly $11 trillion market-in China, this secondary market doesn't exist. China's bank dependency inflates the size of those institutions' balance sheets, making them look scary and bubblicious. However, aggregating the total outstanding credit-the sum of all debt from capital markets and loans-for China and the US gives a better apples-to-apples comparison. When scaled to GDP, China's total outstanding credit is actually lower than the US's. (Exhibit 1)

Exhibit 1: Aggregate Credit Outstanding Between the US and China

Source: FactSet, Securities Industry and Financial Markets Association, China Ministry of Finance, US Federal Reserve System, as of 8/30/2017. Types of credit are approximations using similar (though not identical) credit vehicles to facilitate comparison.

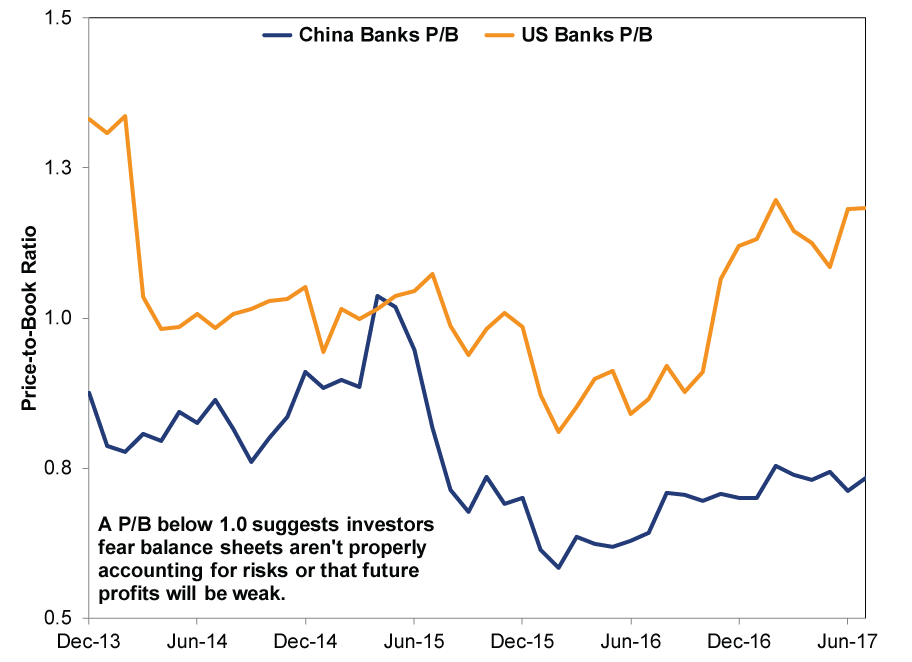

Because of the centralized control over lending and Chinese banks, the government decides what constitutes a bad loan. This has fueled rampant investor concern that the bad assets on Chinese bank balance sheets aren't what they seem. While we agree some assets may be questionable, the market sees this, too. Consider valuations of the "Big Four" publicly traded Chinese banks. Right now, Chinese banks' price-to-book ratios are cheaper than their US counterparts-a sign the market recognizes and has already discounted Chinese asset quality fears.

Exhibit 2: China Banks vs. US Banks (Price-to-Book Ratios)

Source: FactSet, as of 8/30/2017. MSCI China Banks (price-to-book value ratio) and MSCI USA Banks (price-to-book value ratio) from 1/31/2013 - 7/31/2017.

In my view, this isn't a sign to jump into China or its banks because they look "cheap." Rather, it signals fears about a Chinese credit bubble are overwrought. Despite some areas of froth, China's economy overall remains one of the world's fastest-growing, and the government remains committed to economic stability-especially this year, given the political power transition with the 19th Party Congress. While bubble fears may continue percolating as they have for years, I suggest investors pop those false fears.

[i] Source: US Federal Reserve System and China's Ministry of Finance. Data accessed 8/30/2017. Percentages reflect data as of July 2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today