Personal Wealth Management / Market Analysis

Momentum and Other Fake Market Forces

When headlines predict big short-term moves, long-term investors should stay cool.

Well folks, November is upon us, and 2013 is winding down—and if you believe the headlines, stocks look set to cruise to the best annual return since 1997. Sounds great! But to us, these headlines suggest it’s time for a friendly reminder: Short-term moves up or down aren’t predictable or timeable with any degree of certainty or repeatability. Over the foreseeable future, we expect this bull market to keep climbing on strong fundamentals, but that doesn’t mean it’s straight up in the near term—corrections are always possible for any reason (or even no apparent reason). So when headlines hype potential big, quick moves in either direction, it’s important for long-term investors to keep a level head and think longer term.

Before diving deeper into the pitfalls inherent in these wildly bullish November and December forecasts, though, a word on sentiment: These headlines aren’t a sign of euphoria. Some suggest stocks will rise through year-end, then tank when quantitative easing taper terrors and US budget bickering return to the fore. Others say stocks lack fundamental support—it’s all a bubble. And plenty of skepticism remains. In our view, it’s all just short-term noise. A truly bullish media wouldn’t put such a short time limit or so many caveats on their positive projections. This is temporary, tentative enthusiasm at best—plenty more wall of worry remains. This bull has room to run, for many fundamental reasons.

These drivers, however, don’t include most of the reasons headlines today say stocks are set to rise for the next two months. Some, for example, say it’s simply because November and December are historically great for stocks, with a combined mean return of 6%. Sorry folks, but like their namesake, Santa Claus rallies aren’t real. They’re seasonal mythology, like, “Sell in May and Go Away,” the “January Effect” and September and October as “financial hurricane season.” None held true this year, and their occasional correctness is mere coincidence—calendar pages hold no sway over stocks. Markets don’t care what day it is. Regardless of the season, they’ll swing on sentiment in the near term and weigh fundamentals in the longer term.

The other oft-cited reason for a rocking year-end is equally thin: momentum. In other words, stocks will rise because they’ve been rising. But that isn’t how stocks work! Data overwhelmingly show stocks aren’t materially serially correlated. Past price movement doesn’t dictate future returns. If a stock rises 10 days in a row, its next day’s return is always a coin flip. The same holds for broad markets no matter how long or allegedly powerful the trend in question. Gravity applies to real objects—not stocks. Ditto for momentum—it isn’t a market force. Stocks in motion don’t automatically stay in motion—Sir Isaac Newton’s first and second laws don’t apply to markets. He thought they did! And he lost a fortune.

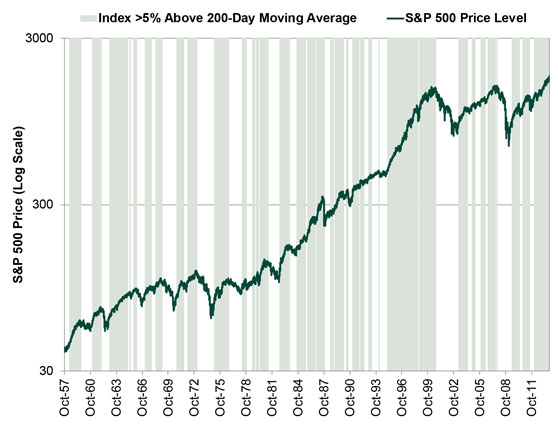

The alleged technical rationale for the momentum argument doesn’t make it any more powerful. According to a handful of industry analysts, because the S&P 500 is more than 5% above its 200-day moving average, it’ll keep on running. Historically, however, the S&P’s relationship with the 200-day average hasn’t predicted anything—it tells you where stocks are today relative to the recent trend. Stocks have spent the majority of many bull markets well above the 200-day average! But as Exhibit 1 shows, they’ve also spent the first stages of many bear markets there. That stocks today are about 8.5% above the 200-day moving average doesn’t say one whit about where they’ll be in 30, 60, 180 or 365 days. It’s just an interesting observation.

Exhibit 1: S&P 500 and 200-Day Moving Average

Source: Federal Reserve Bank of St. Louis, Standard & Poor’s, Fisher Investments Research. S&P 500 Price Index shown from 10/15/1957-11/1/2013; 200-day moving average calculation uses S&P 500 price levels from 1/2/1957-11/1/2013.

Now, maybe stocks do have a smashing November and December! But it isn’t guaranteed. Bullish as we are looking into the mid to longer term, corrections are always possible, and we haven’t seen one in a while. A correction isn’t a certainty, but investors should always be mindful of the possibility.

More importantly, long-term investors should think long term and keep emotions at bay. Headlines like we’ve seen today too often prompt heat-chasing, which can distract folks from their long-term goals. Successful long-term investing takes discipline—turning off emotions and staying cool. The reason to own stocks today isn’t because they might look hot over the next month or two—if you’re a long-term growth investor, it’s because you likely need market-like returns (or close to it) to reach your goals, and over the next 12 to 18 months, stocks appear likelier to rise than not.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today