Personal Wealth Management / Market Analysis

On Rising Rates and Stocks

Our take on the recent jump in long-term Treasury yields—and their likely impact on stocks looking ahead.

Thursday, US 10-year Treasury yields continued a recent jump higher, hitting 1.49% at the close—their highest level in a year.[i] Many blame this jump for the day’s -2.5% S&P 500 selloff—and worry there is more to come.[ii] But in our view, this is an extremely hasty conclusion to reach. For one, we don’t expect yields to end 2021 much higher than current levels, and they may even give up some of the recent rise. But even if they do climb from here, the idea this is automatically a problem for stocks is bogus logic.

First, stay cool. Short-term volatility is part and parcel of even the best bull market years. Getting carried away and extrapolating recent rate-and-stock swings forward is a common investing error too many folks make. Yes, last August, 10-year Treasury yields hit a record low 0.5% before rising to 0.9% at 2020’s end.[iii] Yes, consensus expectations were for another small rise in 2021, with the median forecast eyeing a 1.2% 10-year yield at year end.[iv] Yes, rates are above that level now. But projecting much more from here based on this move is risky business.

Part of the reason why: The recent jump looks mostly like a sentiment-based move—one unlikely to last or extend from here. We don’t see a sudden, material change in bond supply and demand fundamentals. On the supply side, there is currently a dearth of long-term Treasury issuance. Although Uncle Sam’s borrowing exploded in 2020, more than 80% of its record-breaking $21 trillion worth of debt sales were for one year or less and over 90% for five years or less.[v] Some speculate this will reverse with the government selling more longer-dated bonds. But judging by the Treasury Borrowing Advisory Committee’s recommended financing tables for Q1 and Q2, issuance is set to stay concentrated at the short end for the foreseeable future.[vi]

Meanwhile, demand for long-term Treasurys remains plentiful. The last 10-year Treasury note auction on February 10 sold $41 billion worth of debt at 1.155%, slightly lower than January’s auction and with a bid-to-cover ratio over 2.4, meaning it was more than twice oversubscribed—same as last month.[vii] While many point to a 7-year Treasury auction as a likely culprit for Thursday’s rate pop—as the bid-to-cover was well below the recent trend—it was still over 2.0 and only one data point. We don’t think it constitutes a trend. Consider: Developed market sovereign yields outside America are mostly below zero. Any high-quality bond in positive territory, therefore, is likely to attract buyers. Moreover, the Fed continues snapping up long-term Treasurys in secondary markets for its quantitative easing (QE) program—a steady demand source amid dwindling supply. Despite commonplace chatter arguing the recent up move amounts to a 2013-esque “taper tantrum,”[viii] it has given no indication QE is about to stop.

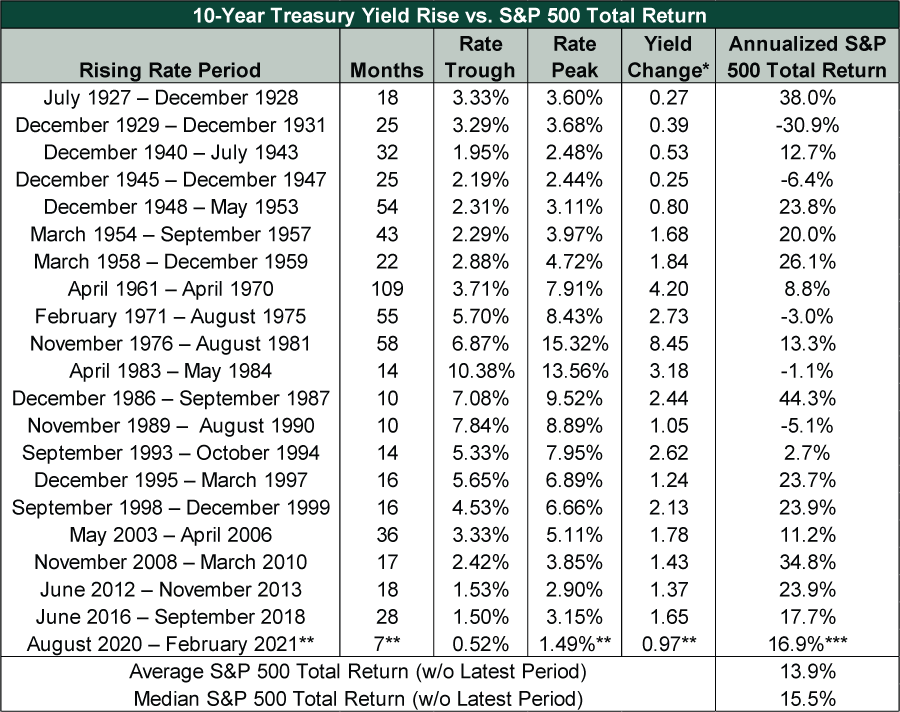

At any rate,[ix] rising bond yields don’t automatically upset markets. Exhibit 1 shows 10-year Treasury yield increases lasting at least seven months (like the current upturn in rates) and the S&P 500’s annualized total return during those periods. There are a few times when rising bond yields coincided with stock market downturns, most notably the Great Depression’s onset. But overall, rising yields have historically coincided with rising stocks. That holds even when those moves have been one or multiple percentage points. Recent volatility notwithstanding, that has been true since 2020’s low as well.

Exhibit 1: Rising Long Rates Typically Don’t Upset Stocks

Source: Multpl.com and Global Financial Data, Inc., as of 2/26/2021. 10-year Treasury yield and S&P 500 total return index, January 1926 – February 2021. *In percentage points. **So far. ***Not annualized.

Some of these rate upturns start or end in bear markets, like the November 2008 – March 2010 one, which began nearly a year into the financial crisis and ended a year into a new bull market. Similarly, February 1971 – August 1975’s move started in the wake of one downturn and persisted through the entirety of another—and well into the ensuing recovery. But therein lies the point: Obviously, a long-term interest move wasn’t related to cyclical shifts.

This time may be different, but it is far from clear Treasury yields’ recent rise augurs ill for stocks. In our view, bond movements don’t necessarily have any impact on them. Stocks move mostly on how well corporations’ 3 – 30 month future earnings reality is likely to match prevailing expectations. Bond yields may have some influence on earnings’ outlook—particularly for rate-sensitive sectors—but there generally isn’t a huge overlap overall and on average. Besides, rising rates very often signify an improving economy, which is usually a good thing for stocks. This is why they are uncorrelated assets. Both can move together, or separately, for their own fundamental and independent reasons.

Although we think bond market fundamentals will likely keep a lid on long rates this year, that isn’t to say they won’t rise ever. One potential longer-term risk we think investors should be aware of: If long rates keep rising, it could steepen the yield curve much further. That would be worth watching for its impact on lending and velocity—how fast money changes hands economy wide—which could lead to higher inflation. Higher inflation itself may be a fine thing. But it raises the likelihood the Fed reacts—and possibly errs and overreacts, ending this expansion. We don’t think that is a risk for stocks in the here and now—more like one potential way this bull market could eventually end. In the meantime, as history shows, stocks’ direction doesn’t generally depend on where bond yields go.

[i] Source: FactSet, as of 2/26/2021.

[ii] Ibid.

[iii] Source: Federal Reserve Bank of St. Louis, as of 2/26/2021. 10-year Treasury yield, 8/4/2020 – 12/31/2020.

[iv] Source: FactSet and Fisher Investments Research, as of 1/12/2021.

[v] Source: SIFMA, as of 2/26/2021.

[vi] Source: Treasury, as of 2/3/2021. TBAC Recommended Financing Table, Q1 and Q2 2021.

[vii] Ibid., as of 2/10/2021. 10-year Treasury note auction results, 2/10/2021.

[viii] In which people (wrongly) feared the Fed would stop buying bonds after some nebulous comments by then-Fed head Ben Bernanke.

[ix] Literally!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 20 - July 242026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today