Personal Wealth Management / Market Analysis

Rising US Unemployment Isn’t a Recovery Dealbreaker

Having 22 million Americans newly out of work is awful, but unemployment isn’t a forward-looking market indicator.

US jobless claims have surged in the aftermath of the coronavirus shutdowns, with about 22 million workers displaced in just four weeks. Many portray this as a further bearish development for stocks, arguing it is a sign consumer spending and other economic drivers will worsen. This is an understandable theory, but we don’t think it passes muster.

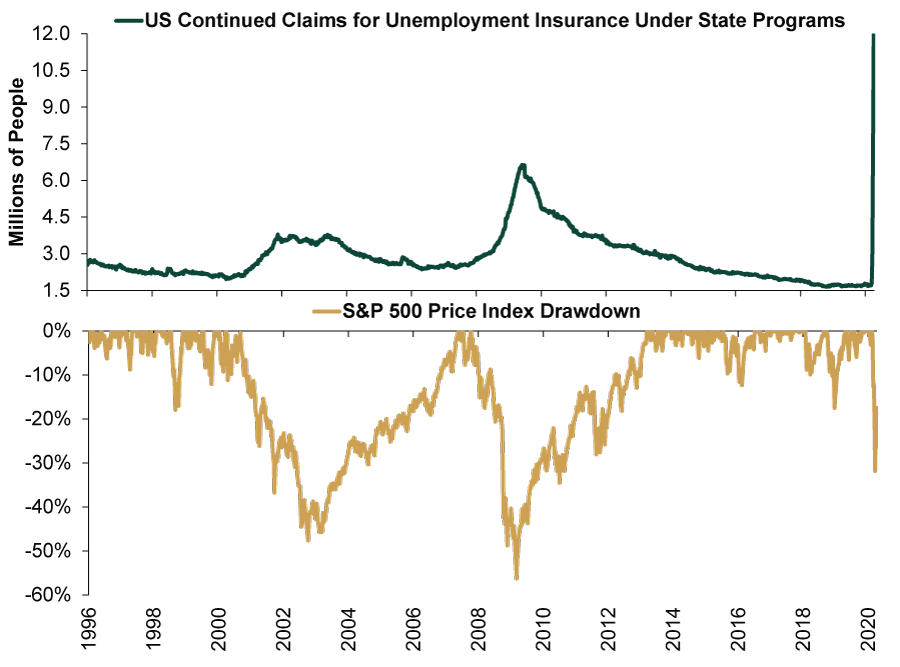

Exhibit 1 shows US continued jobless claims alongside drawdowns in the S&P 500. As it shows, the labor market is a lagging indicator for stocks. While the US unemployment situation is ugly and a tragedy for those affected, the S&P 500 fell -33.9% from February 19 to March 23, the lowest point in this bear market to date.[i] The Russell 2000 Index, which tracks US small-cap stocks, fell -40.8% over the same stretch.[ii] These big declines arrived before jobless claims began surging—stocks seemingly anticipated the awful fallout.

Exhibit 1: US Continued Jobless Claims (through 4/4/20) and the S&P 500

Sources: Bureau of Labor Statistics and FactSet, as of 4/16/2020.

This isn’t to say the bear market is over or stocks can’t fall more—short-term swings and precise market cycle turning points are unpredictable. But the driver for any future major drawdown is much likelier to be future deterioration in the economic outlook relative to today’s expectations, not the backward-looking surge of jobless claims. Labor market indicators such as jobless claims and payrolls are some of the most widely watched data points on Wall Street. They also tend to result from economic trends, not cause them. So if you are inclined to be bearish in response to recent labor market deterioration, consider asking yourself if you really know something that other investors don’t.

As for the many commentators asking where a recovery will come from if tens of millions of people are out of work and cutting discretionary spending, this situation is sadly often the case when a bear market and economic recession end. Investors who can recall the early days of the 2009 – 2020 bull market and economic expansion may recall loads of “jobless recovery” headlines. That theme is common in early bull markets. Stocks usually resume rising first, in anticipation of better days to come, as signs emerge that things aren’t quite as bad as the worst-case-scenario many envision. Then economic indicators turn. The catalyst for this usually isn’t consumer spending, which tends to be much more stable during a recession than many presume, as most spending goes toward necessary goods and services, not entertainment and just-because shopping. Rather, the turnaround usually comes from businesses’ resumed willingness to take risk and invest. That helps jumpstart demand, eventually creating a need to add workers to payrolls.

This time, consumer spending likely falls much farther than usual since so much of it is off limits. That argues for a quick rebound for the many workers who haven’t suffered layoffs or paycuts to return to normal spending activity once stores and non-essential services reopen. Plus, many of the jobless claims filed these last four weeks were for temporary unemployment—people furloughed without pay while their stores and offices were forced to close. If the current disruptions end soon, many of those people will likely return to work and resume earning quickly.

While it may seem to make sense that a recovery cannot develop with so many people unemployed, almost every recovery begins with a high unemployment rate. Stocks don’t require an all-clear flag to rise. Usually, all they need are relative improvements versus present expectations.

[i] Source: FactSet, as of 4/16/2020. S&P 500 price return, 2/19/2020 – 3/23/2020.

[ii] Ibid. Russell 2000 price return, 2/19/2020 – 3/23/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today