Personal Wealth Management /

Taper On, Lending Up

With geopolitical tensions dominating headlines, useful economic news is falling under the radar.

Ukraine stayed atop the headlines through the weekend as the world continued digesting the aftermath of MH17. But while folks focused on the movement of missile launchers and reports from the crash site, economic news on the home front fell under the radar. Like one report showing bank lending sped up in Q2, bringing more fuel for the economy. The world doesn't come to a halt when tensions rise and, while it's challenging, investors must not fall into the trap of exclusively staring at conflicts-doing so can invite a bearish mindset that's out of step with recent data suggesting more economic growth ahead.

Rising bank lending, accompanying the taper of quantitative easing (QE), likely catches many folks by surprise. Most presumed the Fed's bond buying-which depressed long-term interest rates-was hugely stimulative, supporting loan demand. So they feared the Fed pulling its support would sap the economy. Long-term rates would rise, loans would be more expensive, consumers would stop borrowing and stocks would lose their party punchbowl. Most folks didn't realize this punchbowl was laced with sedatives-QE didn't boost the economy. It slowed things down. In trying to lift demand, QE hurt credit supply and slowed bank lending. The same low long-term rates folks presumed would boost borrowers pinched banks' loan profits. Traditional banking is all about borrowing cheap at short-term rates and lending long-term at higher rates. The spread is profit, maturity-transformation manna. Folks can't borrow if banks aren't willing to lend!

Thus, the money from the Fed's bond purchases has largely accumulated on banks' balance sheets, where it does nothing but gather dust.[i] While the Fed boosted the monetary base with QE, broad money supply-the actual money circulating in the economy-didn't grow much because banks weren't lending. That is a necessary step for stimulus to, well, stimulate. But after the Fed alluded to slowing bond buying in May 2013, long-term rates started rising and by-year end they were up 1.01 percentage points.[ii] While they've pulled back some in 2014, they're still higher than before that initial announcement.

It seems banks are already responding favorably-lending is accelerating. Total US lending jumped at a 7.7% seasonally adjusted annual rate (SAAR) in Q2, following Q1's 5.5% rise and Q4 2013's 2.7%.[iii] For comparison, lending fell -5.7% in 2010, then rose a paltry 1.6% in 2011, 2.9% in 2012 and 2.3% in 2013. Loan growth is becoming more broad-based, too. For much of this expansion, commercial & industrial lending was the only category really kicking. But total household lending-mortgages, credit cards, auto loans, consumer loans and student loans combined-turned positive in Q3 2013. Real estate lending-commercial plus household-turned positive in Q1 for the first time since 2007. All of this credit drives investment and spending-it's a powerful force for growth. Publicly traded banks' Q2 earnings reports further illustrate this point, with both big and small banks boosting lending.

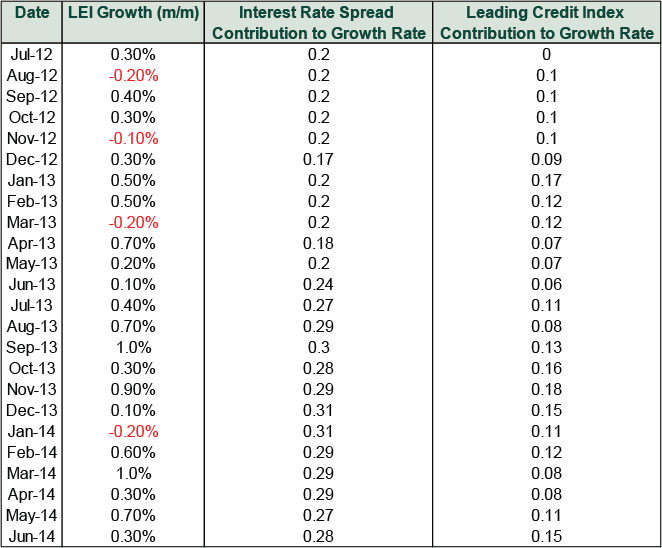

To see this in action, look no further than The Conference Board's Leading Economic Index (LEI), which includes the yield spread and a proprietary measure of credit availability, the Leading Credit Index. No recession in LEI's 55-year published history has started while the index was in an uptrend-and it's high and rising today. The Leading Credit Index and interest rate spread are two big reasons why. Their contributions to LEI are far higher than they were about two years ago, and it is no coincidence they started rising after last May. (Exhibit 1)

Looking ahead, lending has plenty of room to keep on rising-and every reason to do so. The Fed started reducing monthly asset purchases January, and they've chopped another $10 billion at each bi-quarterly meeting. As tapering continues and QE ends, interest rates should drift higher, widening the yield spread. With growth continuing and incomes on the rise, consumers' and businesses' thirst for credit should stay strong. Given more profitable lending, banks should be even happier to comply. And with very few eyeballs on loan growth, it's a decidedly underappreciated positive-the sort of happy surprise stocks love.

Exhibit 1:LEI Growth and Select Contributions

Source: FactSet, as of 7/21/2014. July 2012-June 2014.

[i]Ok, it also gathers 0.25% in interest, which leads to an alternate theory behind QE-that it was all a super-secret way for the Fed to boost balance sheets and help banks meet higher capital requirements.

[ii]Federal Reserve Bank of St. Louis, as of 7/21/2014. 10-Year Treasury Constant Maturity Rate, 5/22/2014-12/31/2013.

[iii] Federal Reserve, as of 7/18/2014. Seasonally Adjusted Annual Rate Quarterly Assets of Commercial Banks, Loans and Leases in Bank Credit.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today