Personal Wealth Management / Market Analysis

The Big Fed News That Surprised Next to No One

Fed hikes. World moves on.

They did it! The Fed, we mean—they finally raised the fed-funds target range by a quarter point Wednesday, in perhaps the most telegraphed monetary policy decision of all time. And in response, stocks fell … and then jumped, taking the S&P 500 from about flat on the day an hour and a half before market close to a 2.2% full-day rise.[i] If that isn’t a sign markets already priced the Fed’s action and moved on, we don’t know what is.

Now, don’t read into that short-term wiggle—it reeks of algorithms and traders teeing off on the news. It is just the funky goings-on that stock markets experience daily. Trying to interpret one hour’s worth of movement is bad for your mental health and highly unlikely to yield any useful conclusions. More importantly: Stocks pretty clearly took the news in stride, when all was said and done. We think that is the right reaction. Moving the target range from 0.0 – 0.25% to 0.25 – 0.5% is not exactly draconian tightening. With 10-year Treasury yields also up in recent days, it doesn’t much flatten the yield curve. Interbank liquidity should remain abundant. Annoyingly, savings and checking account rates will probably remain pitiful, as banks are flush with deposits—they don’t need to attract more. Anyone looking at a long-term chart of the fed-funds rate would be hard pressed to even see the change.

Some argued the rally was one of relief that the Fed is still focused on containing inflation despite some stirring fears that the economy is weakening. There, too, we won’t try to interpret two hours’ worth of sentiment, but conceptually, it falls flat. Today’s elevated inflation rate comes from factors outside the Fed’s control. A rate hike won’t increase oil and gasoline supply, straighten out supply chain kinks, fabricate semiconductors or achieve peace in Ukraine. It probably won’t even tamp down demand. At these levels, it is pure symbolism. On the bright side, as we discussed earlier this week, many of those inflation drivers are already sorting themselves out, which points to the inflation rate moderating over the foreseeable future regardless of what the Fed does. But we have a hard time believing the market’s collective wisdom really views the Fed as moving the needle on prices today.

Surprises move markets most, and nothing about Wednesday’s decision was a surprise. From futures to long-term bond yields to mortgage rates, markets have already priced in significant Fed tightening this year. The Fed itself has been hinting at this for months. Pundits have discussed it ad nauseam for even longer. Whatever power a single fed-funds target rate hike has to sway stocks was spent long ago as investors anticipated today’s “news.”

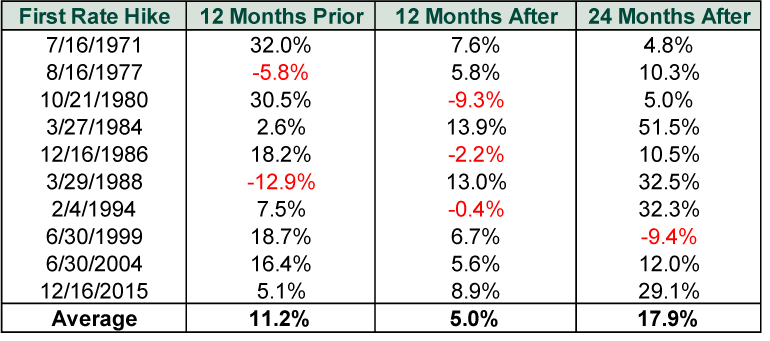

Of course, this is a single day amid a volatile stretch in markets—and it is always faulty logic to draw large conclusions from such short-term swings. But the underappreciated reality is that Fed initial rate hikes aren’t bearish even over more material time periods. (Exhibit 1)

Exhibit 1: S&P 500 Price Returns Before and After Initial Rate Hikes

Source: FactSet, as of 1/5/2022.

“Don’t fight the Fed” is snappy, fun and alliterative, but it is a myth. There is nothing auto-bearish about rate hikes. Fed policy is just one small input into how the huge and complex US economy operates. So, like any other policy move or economic development, you must consider it in the context of economic conditions broadly. In our view, that logic will hold whether we are talking about rate hike number one or seven of this tightening cycle.

[i] Source: FactSet, as of 3/16/2022. S&P 500 price index intraday movement and daily return on 3/16/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today