Personal Wealth Management / Economics

The Fed’s Balancing Act

The Fed is signaling well-ahead balance sheet reductions may be coming and, as with rate hikes and QE tapering, this should prove benign for markets.

No need for a fancy dismount. (Photo by ssj414/iStock.)

Once upon a time, monetary policy was simple: The Fed met periodically, voted on overnight interest rates, and the New York Fed bought and sold stuff to keep rates as close to that target level as possible. But then came 2008 and "unconventional" monetary policy-quantitative easing, or QE, whereby the Fed bought a smorgasbord of long-term assets in an effort to reduce long-term interest rates and juice growth. Since 2013, the Fed has been trying to get back to "normal"-first by tapering (and eventually ending) QE, then by hiking short rates a smidge. Now they're preparing to take another step back from all their monkeying about by gradually reducing their long-term asset portfolio. And on cue, people are worried the economy can't survive without artificial life support. Yet, like the rate hikes and QE taper, another round of monetary policy normalization shouldn't disrupt the bull market. Rather, getting back to normal could do wonders for sentiment, giving investors' animal spirits a lift.

QE was born on Black Friday 2008, when the Fed first announced it. Over the next six years, the policy added $3.7 trillion in US Treasury bonds and mortgage-backed securities to the Fed's balance sheet.[i] While the Fed progressively slowed its bond buying in 2014-the dreaded taper[ii]-and then stopped QE altogether that October, they have since been reinvesting the proceeds of maturing bonds, keeping all of this supposed stimulus on their balance sheet. Now Fed people are signaling they will start reducing it at some point in the hazy future.

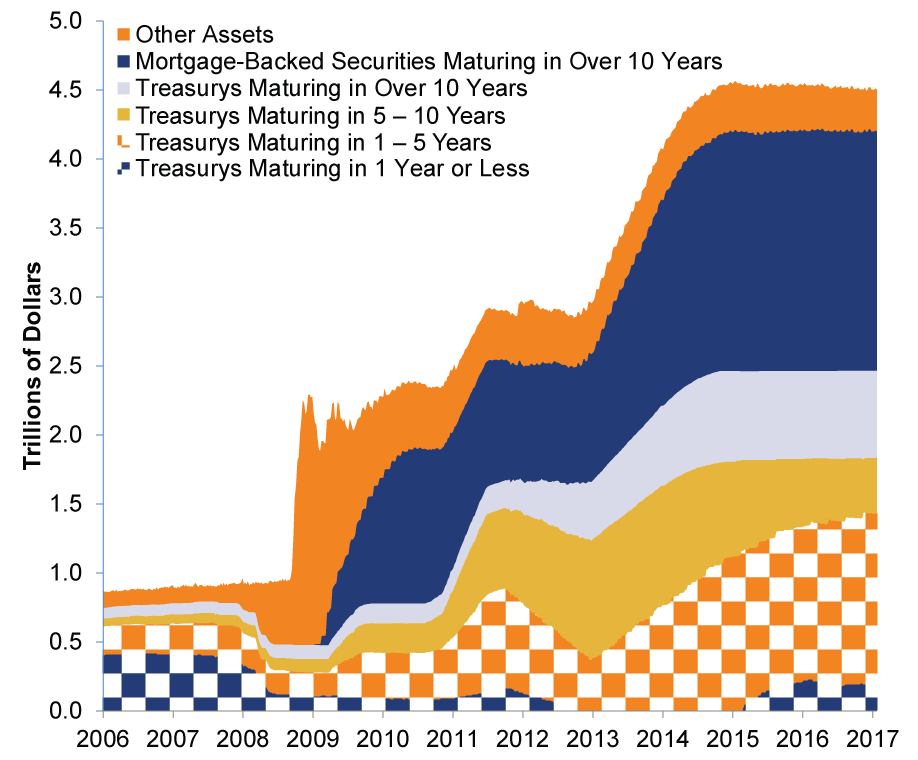

Exhibit 1: Feeling Bloated

Source: Federal Reserve, as of 1/27/2017, Factors Affecting Reserve Balances of Depository Institutions - Maturity Distribution of Securities, Loans, and Selected Other Assets, 1/4/2006 - 1/25/2017.

Worries abound over what happens when the Fed shrinks its balance sheet. Perpetually perplexed pundits fear removing support would collapse money supply, spike long-term interest rates, destabilize financial markets and/or wallop economic growth. Some have played around with Excel to make the Fed's balance sheet resemble stocks' rise since March 2009, implying that as goes the balance sheet, so goes the S&P 500-perpetuating the myth that QE alone drove stocks up. In reality, as we've explained several times, QE flattened the yield curve and likely hurt far more than it helped, making stocks' rise a "despite QE," not "because of QE" phenomenon.

All these concerns remind us of the outcry when the Fed was jawboning about the first rate hike in 2015 and QE tapering in 2013. None of their fearful forecasts bore fruit, and markets fared fine. We see no reason why this time is any different.

The Fed Might Run off, but Investors Shouldn't

While sudden huge shifts in monetary policy-including swift balance sheet changes-raise the potential for errors, the Fed has long preferred a measured approach. For one, while it's impossible to know when it will happen, the jawboning allows markets to start slowly getting used to the idea, sapping surprise potential. It also looks like "gradual" is the watchword within the Fed. Officials speaking out favor placing the Fed's (immense) bond portfolio in "run off" mode. Rather than sell existing securities, the Fed would just stop reinvesting the proceeds as their bond portfolio matures. By simply doing nothing,[iii] the Fed can gradually reduce its balance sheet in a stable, predictable manner. The above chart is basically your run-off timeline.

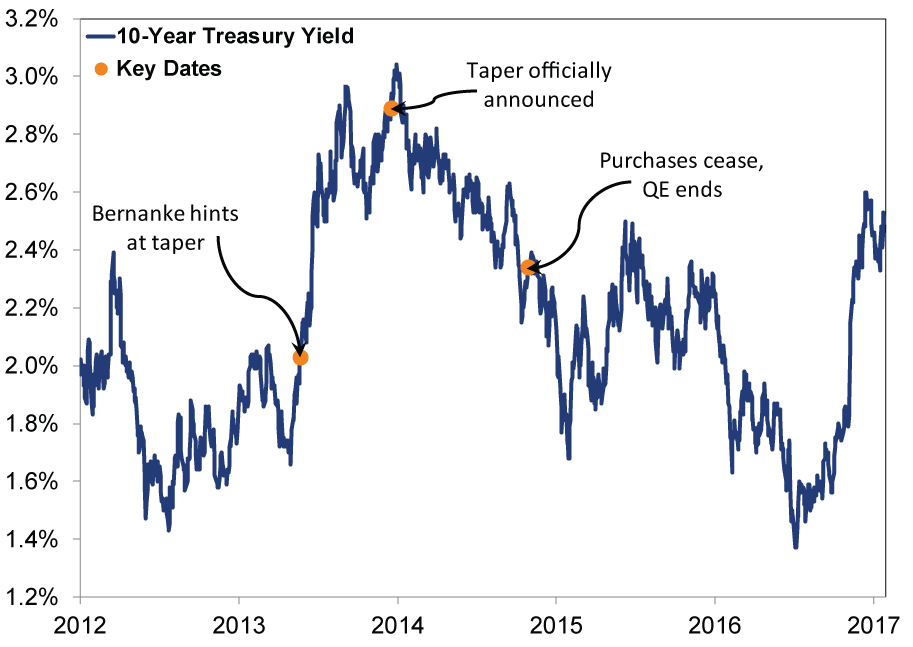

Balance sheet unwinding fears seem like a direct-to-video sequel of QE taper fears. Back in May 2013, people went nuts when Ben Bernanke first hinted the Fed might taper QE sooner rather than later. Pundits were convinced the economy would fall apart without monetary support, and global markets with them. The Fed announced the actual taper in December 2013, started reducing bond purchases in January, and finished winding down in October 2014. Markets did not melt down. Treasury yields rose in the run up to the taper announcement-proving once again that markets discount widely expected events-but fell throughout the taper. 10-year yields-which move opposite prices-fell from 2.9% on Taper Day to 2.3% at the taper's end (see Exhibit 2).[iv] From there through July 2016, yields declined to a record low, even though the Fed wasn't buying $45 billion in Treasury bonds each month. Other central banks were still doing QE, reducing long rates globally, and driving demand for relatively higher-yielding Treasurys. The S&P 500 gained 10.7% between Bernanke's May 22 speech and the actual taper announcement on December 18-the period known as "taper talk."[v] It gained another 11.4% during the taper itself, and is presently up 21.6% since the Fed bought its last bond.[vi]

Exhibit 2: Rorschach Taper

Source: St. Louis Fed as of 1/27/2017.

The global supply and demand picture hasn't really changed since then. If the Fed were to stop reinvesting proceeds of maturing bonds tomorrow, we suspect other investors would be delighted to snap them up. The world is still awash in $9 trillion of negative-yielding debt. We suspect a large portion of those holders enviously eye positive-yielding Treasuries, if more than two times oversubscribed bid-to-cover ratios at Treasury auctions are any indication.

Demand for US Treasurys is broad and multifaceted. The Treasury market is the biggest and most liquid in the world, where "safe assets" used for trade, collateral and capital requirements are a hot ticket. Treasurys are the bedrock asset of the global financial system. Barring a misstep, the Fed slowly shrinking its balance sheet will likely prove benign. Markets should have no problem absorbing the loss of a buyer, even if it's the world's largest Treasury holder. Banks, pension funds, foreign governments, other institutional investors and individuals are all eager buyers. Long rates aren't guaranteed to shoot up. They may even fall a smidge, depending on what global markets look like when the time comes.

Instead of fearing what the media says may happen when the Fed puts yet another wonky instrument back in the toolbox, consider what may happen when, for the third time, worries are proven wrong. When there are few, if any, ways left to credit the Fed for the bull market, people might finally realize monetary policy has little role in stocks' ascent and the economy doesn't need Fed stimulus. As they take this next step and the economy and markets don't implode, confidence should get a nice boost, making investors ever more eager to bid up stocks.

One way to view the past decade economically is as a vast, if sometimes harrowing, experiment in monetary policy. While we've seen what it can do, we've also seen its limits, as central banks pushed boundaries and failed to deliver. Seeing those limits, central bankers are sensibly starting to step away, which we can all be thankful for.

[i] Source: Federal Reserve, as of 1/27/2017.

[ii] Not tapir.

[iii] Monetary policy we're in favor of!

[iv] Source: St. Louis Fed as of 1/27/2017. QE officially ended 10/29/2014.

[v] Source: FactSet, as of 1/26/2017. S&P 500 Total Return Index, 5/22/2013 - 12/18/2013

[vi] Ibid. S&P 500 Total Return Index, 12/18/2013 - 10/29/2014 and 10/29/2014 - 1/25/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today