Personal Wealth Management / Economics

The Media’s Inflated Take on Inflation

Rising prices in September aren't evidence of a crisis averted.

We just passed October's halfway point, and you know what that means! Yes, Halloween is less than two weeks away, but also, the US Bureau of Labor Statistics just released the latest Consumer Price Index (CPI) numbers.[i] Yippee! Those numbers show prices rose at their fastest pace in nearly two years, and if the financial punditry's reaction is any indication, this is more treat than trick[ii]-defanging deflationary doom demons. For investors, however, note that a fundamental shift hasn't occurred-only the media's portrayal of the news has changed.

Here are those sweet September numbers: CPI rose 0.3% m/m, up from August's 0.2% and the fastest monthly rate since April. On a year-over-year basis, CPI was up 1.5%-the swiftest since October 2014. Though the headline number usually gets the, well, headlines, there are other iterations to consider, too. "Core" CPI, for example, strips away volatile food and energy prices that can dramatically skew the headline figure (more on this later), and in September, this measure inched up 0.1% m/m (2.2% y/y).

Before you wonder how the Fed will interpret all this, we should note Janet Yellen and friends emphasize the personal consumption expenditures (PCE) price index. That isn't to say the Fed ignores the CPI, they just aren't their primary gauges. We won't know September's PCE numbers until month-end, but August's PCE price index rose 0.1% m/m (1.0% y/y), while core PCE gained 0.2% m/m (1.7% y/y).

For their part, the media reaction has been pretty positive toward this one month of data. Some even described it as an early Christmas present for central bankers[iii] because it means those scary deflationary forces remain at bay. Joy! The data say things are going to be ok! However, we find that optimistic reaction a bit odd considering we already know the culprit for recent deflation: plunging energy prices. Here are some charts.

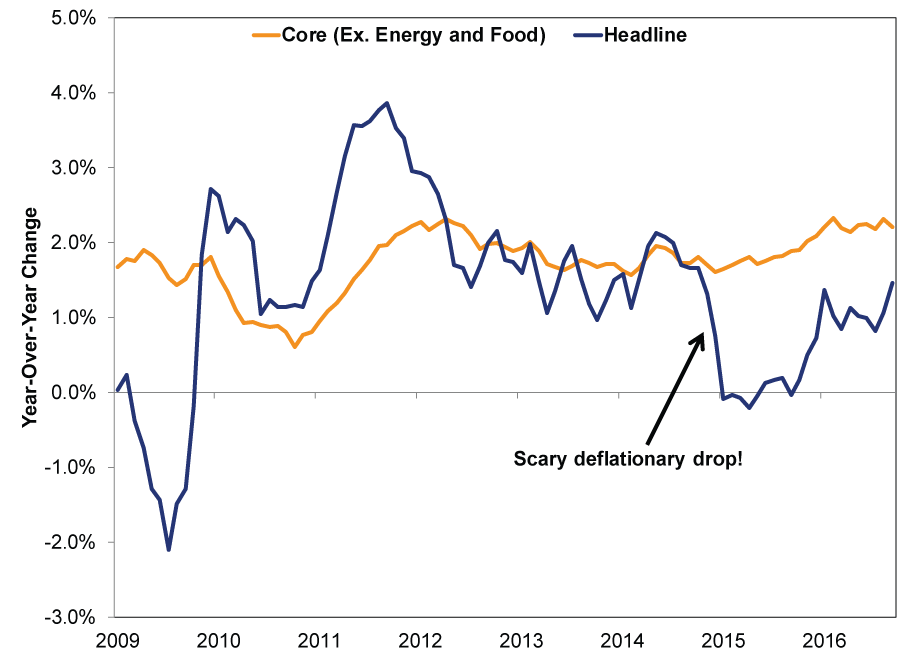

Exhibit 1: Headline CPI Vs. Core CPI During the Current Expansion

Source: St. Louis Federal Reserve, as of 10/18/2016.

Core CPI has been pretty stable for the past several years. Headline CPI, not as much. Why? Check out what energy prices have done.

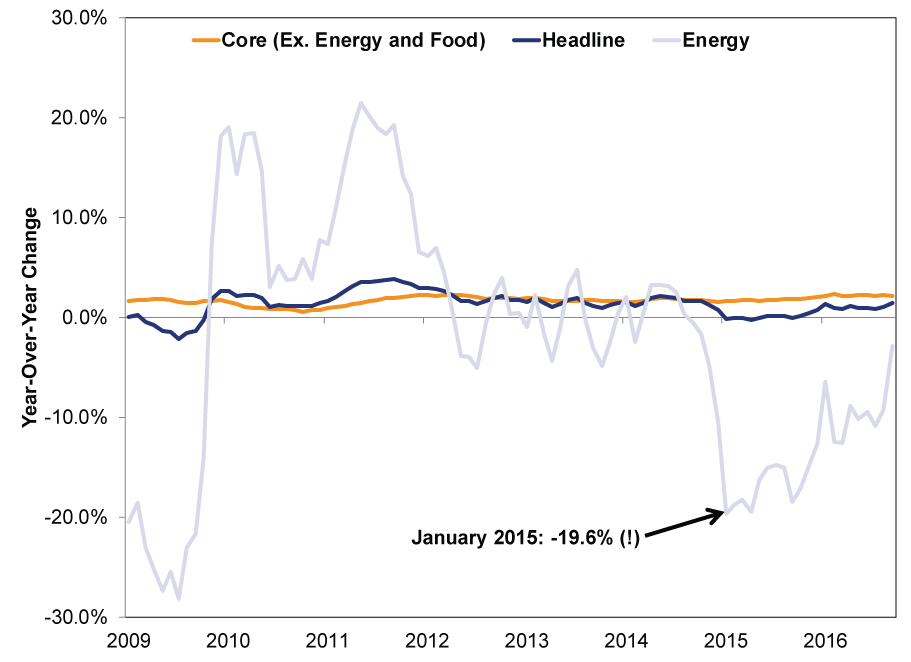

Exhibit 2: Headline CPI Vs. Core CPI Vs. Energy CPI During the Current Expansion

Source: St. Louis Federal Reserve, as of 10/18/2016.

As oil plunged starting in mid-2014, energy prices followed suit, weighing on headline prices. For astute MarketMinder readers, we know this isn't breaking news, but it's a good example of why core CPI exists-energy can be pretty darn volatile. As energy prices stabilized in recent months, their detraction from headline CPI eased, too.

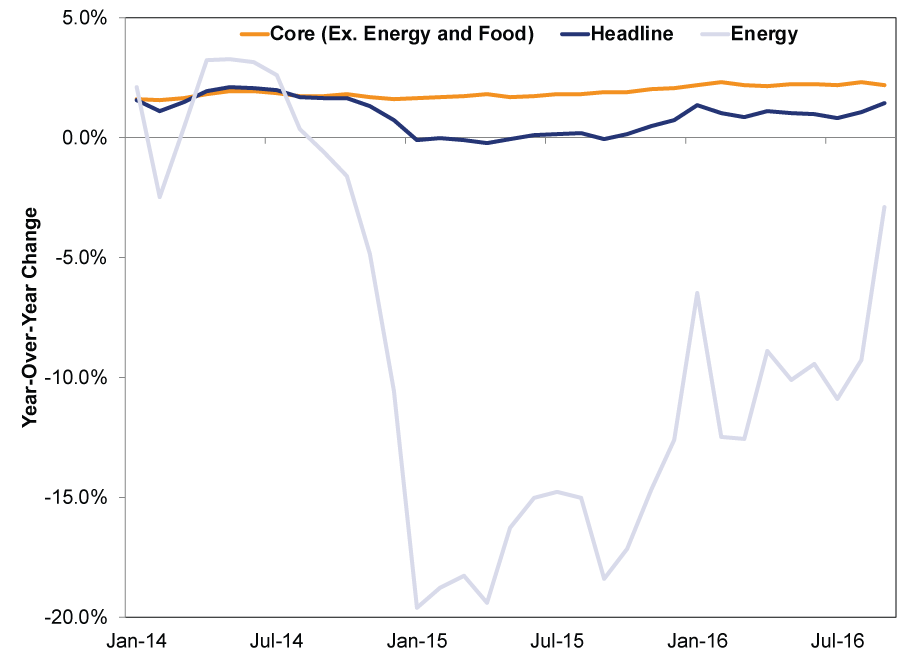

Exhibit 3: Headline CPI Vs. Core CPI Vs. Energy CPI Since 2014

Source: St. Louis Federal Reserve, as of 10/18/2016.

While September's CPI figures don't tell a radically new story about inflation, the media's coverage reveals its penchant for spin. Remember all those fears connecting low CPI reports to deflation a couple years ago? Most centered on Europe, but the occasional one speculated about a deflationary spiral wrecking global growth, impacting the US, too. Those fears were vastly overwrought, as we said at the time.

Though pundits aren't bemoaning rising prices at the moment, we do wonder when they'll start fretting the other side of the -flation coin: looming hot inflation[iv] that will whack consumers. It wouldn't surprise us if the narrative shifted that direction if headline CPI continues rising. We can already envision the headlines, as the same pundits who questioned why the Fed would raise rates when inflation was so low could very well blame the Fed for moving too slowly as prices pick up. Trying to have it both ways is a time-honored tradition. That said, fastflationTM fears aren't new, either. Lots of folks worried the Fed's quantitative easing program would lead to problems like hyperinflation. That didn't happen, but given how dour sentiment has been over the past seven years, swapping one false fear for another would be par for the course.

For investors, ditch the narrative and look at the numbers-nothing here looks particularly worrisome. Broad money supply is growing steadily and has been picking up for most of this year. Some noted that business lending fell slightly in August, but more recent numbers make this look more like a blip than the beginning of a worrisome trend. And now the latest CPI report shows inflation remains benign. How this impacts the Fed's decision-making, we can't say-nor will we venture a guess. But for investors, the evidence indicates the US economic situation is better than most appreciate. This has been the case for the entirety of this bull market, and so long as this gap between expectations and reality persists, we see no reason not to be bullish.

[i] We are certain this was your second guess.

[ii] And most definitely not a rock.

[iii] So does that mean Janet Yellen was naughty or nice? Wait, don't answer that.

[iv] Which we hereby dub "fastflation," covering higher-than-average inflation that isn't quite hyperinflationary. We must have a -flation for every season, you know.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today