Personal Wealth Management / Economics

The Return of the Chinese Hard-Landing Ghost Story

Recent Chinese data have stirred “hard landing” fears—is it different this time?

Throughout 2018, financial media speculated over whether China’s long-dreaded economic “hard landing” would finally occur. Though it doesn’t appear to have happened last year, many are convinced the seeds of trouble have been sown and are starting to sprout—with December’s contractionary manufacturing data just the beginning. However, we recommend stepping back and adding context to the most recent releases. Though Chinese economic growth is slowing, both data and squishier reads suggest a hard landing isn’t underway.

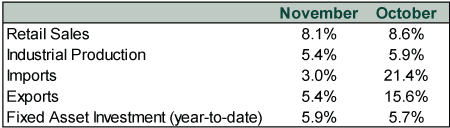

The most recent release of monthly data showed widely followed metrics continued slowing. (Exhibit 1)

Exhibit 1: China’s Recent Economic Data

Source: China’s National Bureau of Statistics, as of 12/31/2018. All figures year-over-year unless noted otherwise.

That isn’t all. Chinese industrial firms reported falling profits for the first time in three years. Most recently, the official and Caixin manufacturing purchasing managers’ indexes (PMIs) hit 49.4 and 49.7, respectively, in December. PMI readings below 50 indicate the majority of surveyed firms contracted.

While the data seemingly confirm a hurting Chinese economy, consider some recent history. Industrial profits last declined in December 2015. That coincided with a stretch in late 2015 – early 2016 when both manufacturing PMIs spent months below 50. However, industrial weakness was more or less deliberate. It reflected China’s well-telegraphed effort to transition from heavy industry-led growth to a consumption- and services-driven economy. More importantly, several months of contractionary manufacturing PMIs didn’t beget a broader “hard landing.” Chinese GDP has been slowing for years—without causing a global recession. This long-running trend isn’t a surprise.

Some argue this time is different since the “trade war” with the US is supposedly causing the slowdown. It is possible looming new tariffs pulled some activity forward as firms sought to ship merchandise before the duties took effect, resulting in even slower growth in their wake. November Chinese exports slowing to 5.4% y/y after growing at a double-digit rate for most of 2018 could reflect this activity.[i] However, the most recent US data show a meaningful uptick in imports of goods from China from April – October—despite tariffs taking effect in July and September.[ii] We need more data to confirm whether this is a blip or a trend, but thus far, those fearful trade war projections seem wide of the mark.

Rather than the trade tiff, we think China’s slowdown is more related to the government’s efforts to get control over the shadow banking realm last year. Policymakers prioritized moving activity from the shadow banking sector to traditional financial markets. However, that disproportionately knocked medium- to small-sized businesses, which major state-run banks historically shunned. To soften the blow, regulators have stepped in with targeted stimulus measures. China’s central bank cut the Reserve Requirement Ratio several times last year and did so again on Friday, incentivizing banks to lend. The government also lowered taxes for individuals and boosted local infrastructure investment. However, these measures’ impacts hit at a lag, so their benefits won’t show up in the data immediately. We also don’t know how effective they will be. It is possible rules adopted as part of the shadow banking crackdown end up preventing money from going where it is most needed.

Regardless of the “why,” many experts reckon the data are worse than reported. Chinese data are always under scrutiny—with indexes even tallying underwear sales in hopes of pinpointing economic health. Doubts about official Chinese economic data’s accuracy are understandable, especially when the national government makes seemingly arbitrary moves—like unexpectedly shutting down one local government’s data-tracking efforts. However, skepticism shouldn’t be reserved solely for Chinese data. This logic applies to any country’s numbers to varying degrees—even the US. All economic datasets have imperfections and limitations.

China’s official government numbers aren’t our only source of information. Other countries and private companies collect data, too, and these readings are positive overall. Based on our analysis of several recent earnings calls, companies with business ties to China are confirming that despite slowing growth, demand remains solid (with Apple being the obvious exception, and one people read waaaaaaaaaaaaaaay too much into, in our view, particularly since other company reports make it seem product-line or industry-specific). For example, some Consumer Discretionary firms are reporting strong demand for luxury products. Many Health Care companies continue investing heavily in China. Tech-related hardware firms still have a positive long-term outlook toward the country, despite projecting weaker growth in the short term. While firms acknowledge trade tensions and tariffs have weighed on sentiment, companies also haven’t made wholesale changes to their supply chains—many of which took years to develop. Overall, business looks solid, even if growth isn’t gangbusters. If the economy were indeed crashing, we wouldn’t have to wait for the National Bureau of Statistics to confirm it—multinational firms with China ties would be broadly warning already.

Worries about China’s economy—and how it will impact the world—have persisted for years. You need only go back to January 2016, when volatile Chinese markets triggered claims that domestic stocks were warning the world of imminent trouble for the world’s second-largest economy. Yet those dire forecasts were wrong. It may seem different today because of trade war chatter, but in our view, this is a different flavor of the same “hard landing” fears. The data and comments from business leaders active in China don’t seem to support the theory, and in our view, a Chinese economic collapse remains more fiction than reality.

[i] Source: General Administration of Customs for the People’s Republic of China, as of 12/28/2018.

[ii] Source: US Census Bureau, as of 12/28/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today