Personal Wealth Management / Market Analysis

About Those Falling Commodity Prices

Some say falling oil and metals prices are a sign global demand is sinking, but a closer look suggests the truth is much brighter.

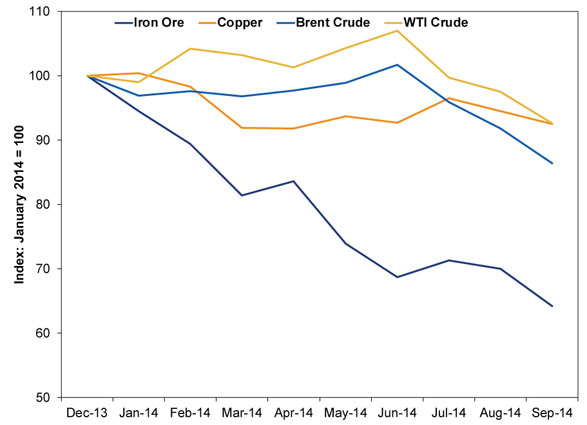

Here is a scary story you may have heard this month: Commodity prices are tanking as Asia's demand for crude oil and industrial metals dives, signaling a global economic slowdown. It has appeared, with varying degrees of detail and hyperbole, here, here, here, here, here and here. Some infer bad things from charts like Exhibit 1. Others use anecdotal evidence and rhetoric. We don't think either approach-or the thesis-matches reality, however. Take a deep data dive, and you'll see a far more boring, benign reason for falling prices: Supply is up way more than demand, which isn't plummeting (contrary to widespread belief).

Exhibit 1: Select Commodity Prices Year-to-Date

Source: FactSet, as of 10/20/2014. We deliberately excluded nickel from this even though it features heavily in the rest of this article, because Indonesia's new export ban monkeyed with the price severely this year. It is way up, which doesn't fit with the scary downward lines the media is hyping.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors.

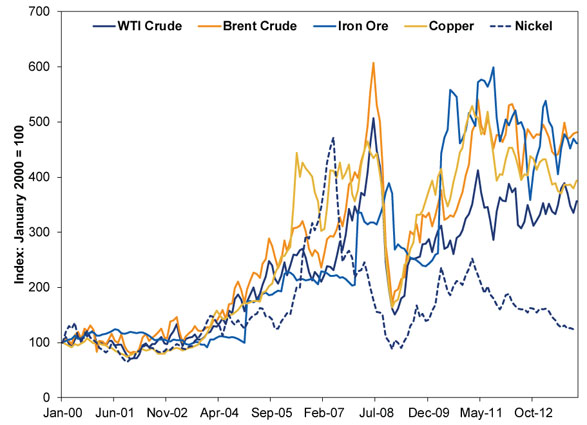

Our story begins over a decade ago, when commodity prices started a years-long rise some call a "supercycle." China, Brazil and India were booming (along with much of the developing world). Their massive infrastructure buildouts drove demand for industrial metals sky-high. Burgeoning development and wider prosperity spurred oil demand. If you were in the Materials business, life was good.

Exhibit 2: Select Commodity Prices, 2000 - 2013

Source: FactSet, as of 10/20/2014.

Prices broadly tanked in late 2008, at the financial crisis's depths, but they bounced quick and stayed high into 2011, before they started pulling back. Even though the global economy was still growing at an ok rate. This is your first clue falling commodity prices are not synonymous with a falling global economy.

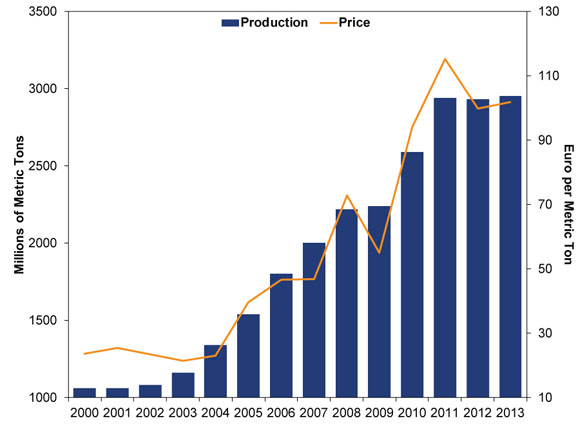

So why are they down? Simple: Supply is up! When prices were high, miners and oil producers had a huge incentive to ramp up production to take advantage. Most expected Emerging Markets to keep the pedal to the medal, so producers figured they'd still reap huge rewards once those new mines and wells came online. But, as happens sometimes, they largely overshot. Supply jumped far higher than demand.

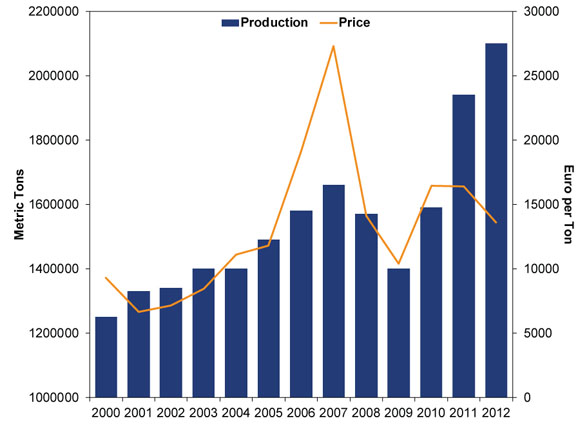

Exhibit 3: Iron Ore (Annual Global Production and Year-End Price)

Source: FactSet, as of 10/20/2014.

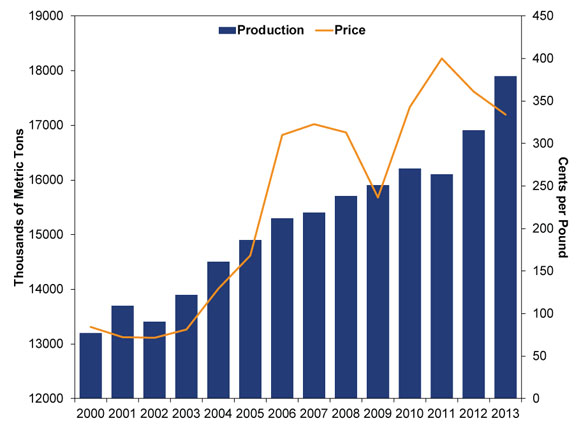

Exhibit 4: Copper (Annual Global Production and Year-End Price)

Source: FactSet, as of 10/20/2014.

Exhibit 5: Nickel (Annual Global Production and Year-End Price)

Source: FactSet, as of 10/20/2014.

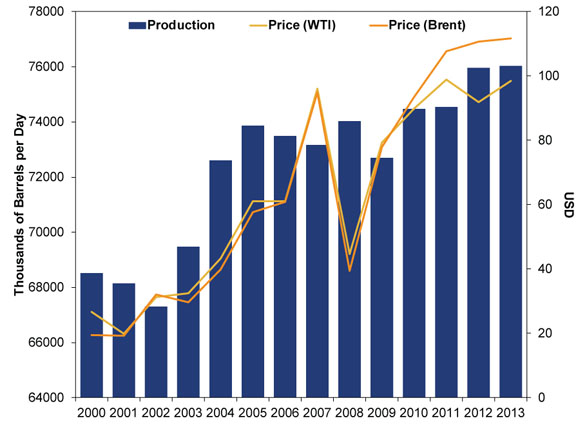

Exhibit 6: Crude Oil (Annual Global Production and Year-End Price)

Source: FactSet, as of 10/20/2014.

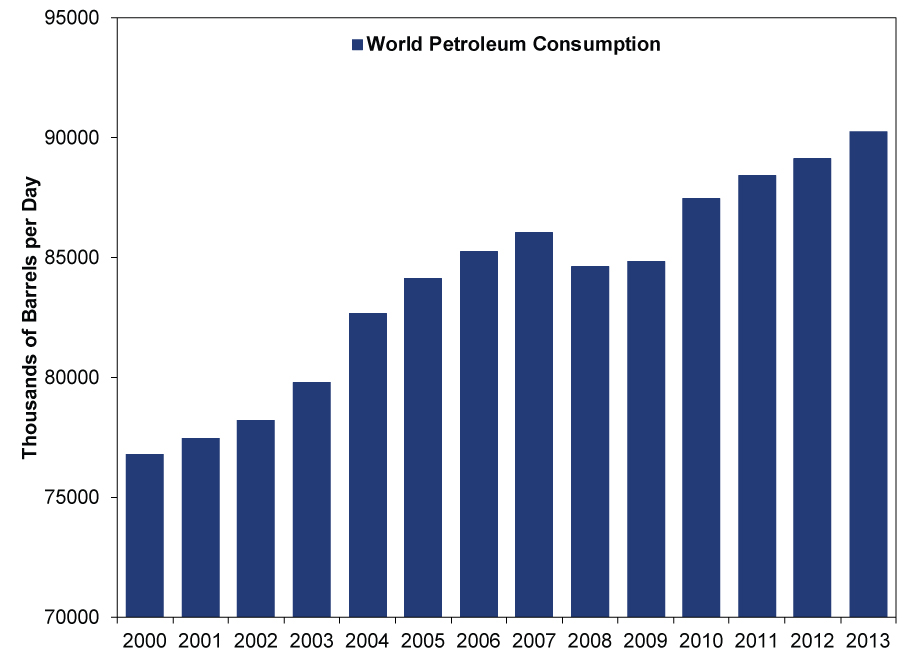

The good folks at Statista publish global annual copper consumption and China's seaborne iron ore imports, which account for about two-thirds of global iron ore demand. As you can see here and here, both are rising, albeit modestly. Stainless steel production accounts for about 65% of nickel consumption globally, and according to World Steel News, production is at all-time highs and rising. So is global oil consumption, as Exhibit 7 shows.

Exhibit 7: Global Oil Consumption

Source: US Energy Information Administration, as of 10/20/2014. Total petroleum consumption, 2000 - 2013.

So let's put this all together. Since 2011, we've had commodity prices in a choppy downtrend, supply jumping and demand rising more modestly. All coincided with a growing global economy despite some high-profile weak spots.[i]

In all likelihood, 2014 is a continuation of that trend. Full-year supply data won't be available until 2015, but the biggest Materials firms aren't cutting back-most still expect steady demand increases, and large firms have the economies of scale to weather lower prices. They've already made the heavy up-front investments, and long-term thinking (and logic) dictate they'll see them through. One large miner (reportedly on track to top production targets) recently scoffed at the notion they'd cut production. They're focused on the long term, not recent price swings.

Energy firms aren't cutting back either. The US shale fields are pumping apace, and OPEC hasn't dropped production to offset-Libya is coming back online, and Saudi Arabia decided keeping market share was more important than supporting prices. On the demand front, OECD monthly oil consumption is largely in line with 2013, and full annual global demand is expected to rise by about one million barrels per day in 2014 and another 1.2 million in 2015.

Now, none of this means recent price movement results solely from longer-term supply and demand fundamentals. Commodity markets see sentiment-driven short-term volatility, too. We wouldn't be surprised if that were a factor these days, particularly with hard-landing fears plaguing China once again. But dismal sentiment doesn't match reality-actual data, though wobbly by Chinese standards, show solid growth.

Whether the global economy picks up or slows a wee bit this year, we can't say-short-term economic swings are tough to forecast (see every global think tank's missed forecasts for evidence). But we do know, from experience, that a combination of rising commodity supply and demand are pretty darned consistent with a growing world, regardless of what prices do. In our view, rumblings to the contrary are just one more ghost story to accompany stocks' pullback.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] Like those six straight quarters of contracting eurozone GDP.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today