Personal Wealth Management / Economics

No Foolin’

Lately, we’ve seen claims stocks’ rally is a Fed-fueled bubble—but strong earnings and other fundamentals show that’s not the case.

As markets globally have neared or surpassed previous highs in recent weeks, we’ve seen a flurry of articles suggesting the rally isn’t legit—instead, naysayers argue, it’s a bubble fed by QE funny money. Even some Fed governors subscribe to this theory, according to the January 29-30 meeting minutes: “Some [participants] noted that further asset purchases could foster market behavior that could undermine financial stability.” (That’s Fed-speak for “bubble.”)

A quick look at the Fed’s balance sheet should put these jitters to rest—as shown in Exhibit 1, most of the QE money is parked back at the Fed as excess reserves. Idle cash tends not to inflate bubbles.

Exhibit 1: Federal Reserve Assets and Liabilities

Source: Thomson Reuters as of 01/15/2013, US Federal Reserve, from 09/09/1992 to 01/09/2013.

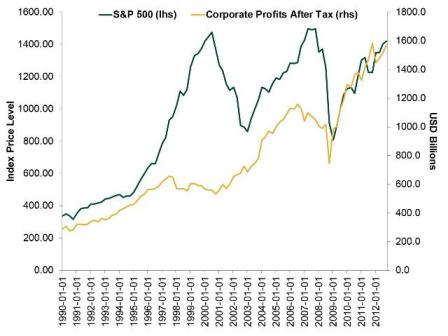

Fundamentals, not easy money, have propelled stocks since this bull market began in March 2009. One big example: For the bull’s duration, stock prices have moved almost in lockstep with after-tax corporate profits. (Exhibit 2. HT: Dr. Mark J. Perry.)

Exhibit 2: S&P 500 Price Level vs. After-Tax Corporate Profits

Source: St. Louis Federal Reserve. S&P 500 Stock Price Index (Quarterly) and Corporate Profits After Tax with Inventory Valuation Adjustment and Capital Consumption Adjustment, seasonally adjusted.

Considering a stock is no more or less than a slice of ownership in a publicly traded company, we’d rationally expect a strong correlation between prices and profits in a healthy bull market. Bubbles typically happen when we see the opposite—when high stock prices are disconnected from fundamentals. This was the case at the turn of the millennium, when profits didn’t support the rapid rise in equities. Then, at the tech bubble’s height, many investors were paying a premium for loss-making firms that lacked viable business models. That’s simply not happening today—the tight spread between earnings and stock prices would seemingly imply still-skeptical investors aren’t placing much of a premium on future earnings. They typically do as bull markets mature, only getting to extremes at the very end. Yet today, with valuations still near historic lows, investors are getting profitable companies on the cheap.

Q4 earnings underscore this. According to Thomson Reuters’ most recent estimate, with 494 S&P 500 companies reporting as of March 28, earnings per share grew an estimated 6.3%—the 13th straight quarter of growth.i 69% beat expectations, well above the long-term average of 62% and the past four quarters’ average of 50%. Recall, earnings growth slowed last year as firms struggled to beat tough year-over-year comparisons. Businesses were still plenty profitable, but the growth rate from previous all-time highs was understandably muted. Now, however, it seems they’ve perhaps passed the hump. And not just because they’ve cut costs—top-line revenues also grew nicely in Q4, at an estimated 3.6%. Contrast that with Q3, when earnings eked out 0.1% growth while revenues pulled back -0.8%, and it seems clear an already-sturdy corporate America’s gotten even stronger in recent months.

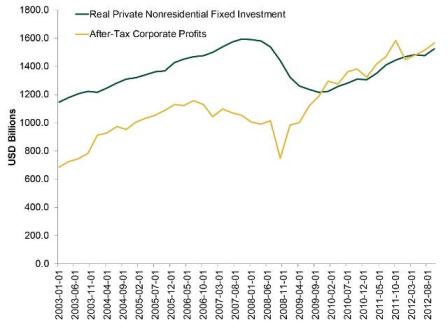

Importantly, firms are reinvesting much of these earnings—profits are rising hand-in-hand with business investment. (Exhibit 3)

Exhibit 3: Real Non-Residential Fixed Investment vs. After-Tax Corporate Profits

Source: St. Louis Federal Reserve. Private Nonresidential Fixed Investment, seasonally adjusted in chained 2005 US dollars, and Corporate Profits After Tax with Inventory Valuation Adjustment and Capital Consumption Adjustment, seasonally adjusted.

This allows firms to continue investing and expanding without depleting corporate cash balances, which remain at record highs. It also lets them buy back shares and make strategic cash-based acquisitions, both of which support higher prices. With earnings expected to keep growing in 2013, stock prices have plenty of fodder for future growth.

This is despite the Fed, not because of it—as we’ve written, QE is contractionary. It flattens the yield curve, diminishing banks’ net interest margins and reducing their incentive to lend—hence why the money’s not circulating. That firms are finding ways to invest and grow anyway is a testament to the private sector’s strength. And that many fail to recognize this and instead credit the Fed for stocks’ rally is just one more sign negative sentiment is detached from reality.

i Source: Thomson Reuters, “This Week in Earnings,” March 28, 2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today