Personal Wealth Management / Politics

About That Tax Reform Bill …

Like all tax changes, this one creates winners and losers but shouldn’t have much market impact in either direction.

Editors’ note: Our political commentary is nonpartisan and aims to assess policies’ potential market impact only. We favor no political party or politician and believe political bias is a dangerous investing error.

After weeks of Congressional debates, horse-trading and “still too early to speculate about all this,” it is finally time—time for us to talk in depth about Congress’s final tax reform package. The bill passed after a parliamentary snafu forced a second House vote, and President Trump’s signature seems a foregone conclusion. Who wins? Who loses? Should folks do anything special in 2017’s final days to game the changes for 2018? How much of an economic boost should investors really expect? We will dive in below, but the big takeaway is this: Tax changes aren’t a material market driver. Cuts aren’t bullish (or bearish). Hikes aren’t bearish (or bullish). Markets are very good at pricing in widely expected developments, and Congress has been debating this stuff for months. We’ve had a rough blueprint of the current plans since early November, when the House passed its tax bill. To say markets haven’t priced it yet is to say markets aren’t efficient at all—a fundamental misunderstanding, in our view. We aren’t dismissing any of the tax changes, which will impact people and businesses. But these micro impacts, if you’ll pardon the jargon, just don’t have the surprise power necessary to sway markets in either direction.

We feel compelled to stress that last point because we continually encounter claims like this: “[Investment bank/market guru] believes only 40% of the eventual lift expected from these changes has been priced into the market so far, suggesting a big boost for equities once the ink is dry on the bill.” Here is what that statement means in practice: “Even though everyone knows what the tax changes will be, they haven’t fully impacted stock prices yet because markets are waiting for arbitrary things like signatures and calendar page turns.” If you still think this is plausible, here is what it would imply at the human level: “I know what the tax changes are going to be, and I’ve bought some stocks as a result, but I’m waiting until after they take effect to do the rest of my buying, even though nothing material is going to change between now and then. It just seems like the thing to do, for reasons I can’t articulate, and I don’t care if other people try to get in front of all this and drive prices higher for me.” We know people aren’t always fully rational, but this brand of illogic is fantastical. In reality, markets move very, very quickly. People have already spent months using the market as a voting machine to register their feelings about tax reform. There is nothing new to weigh now.

As for your personal finances, whether you will be better or worse off under the plan largely depends on how much you make, where you live, whether you own a home, your filing status, whether you have children, and several other things. In other words, talk to your tax advisor.

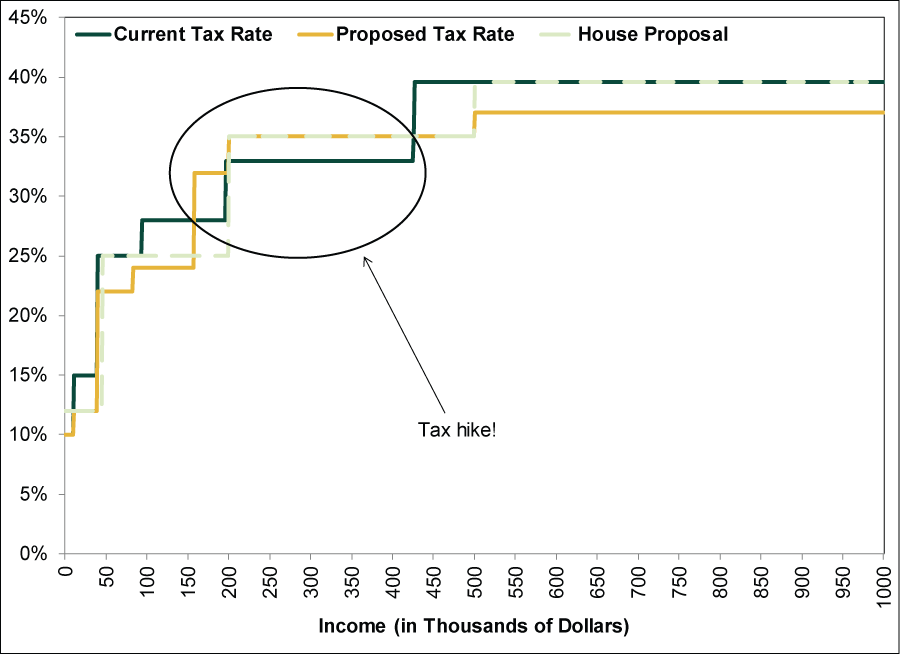

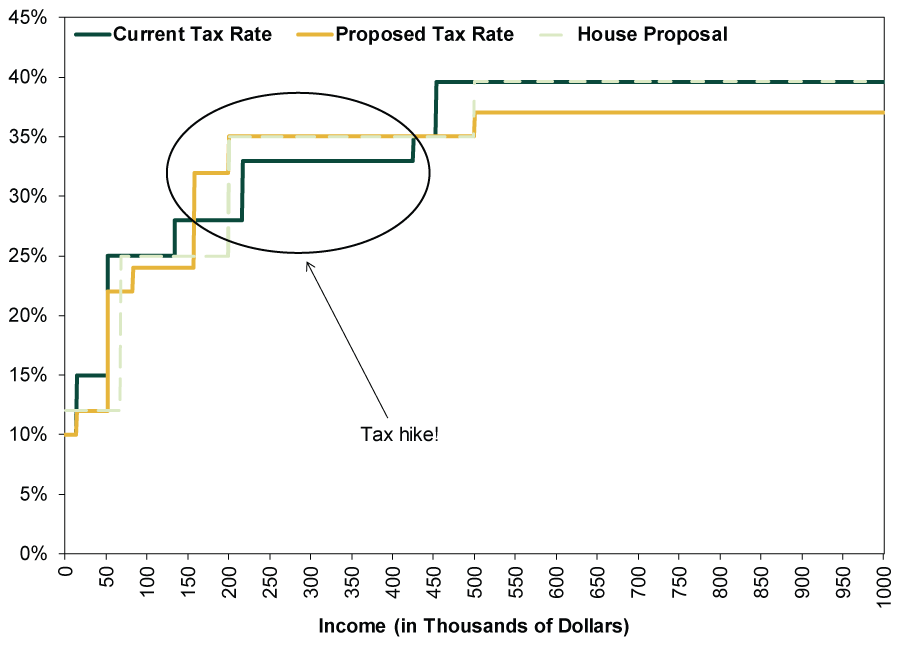

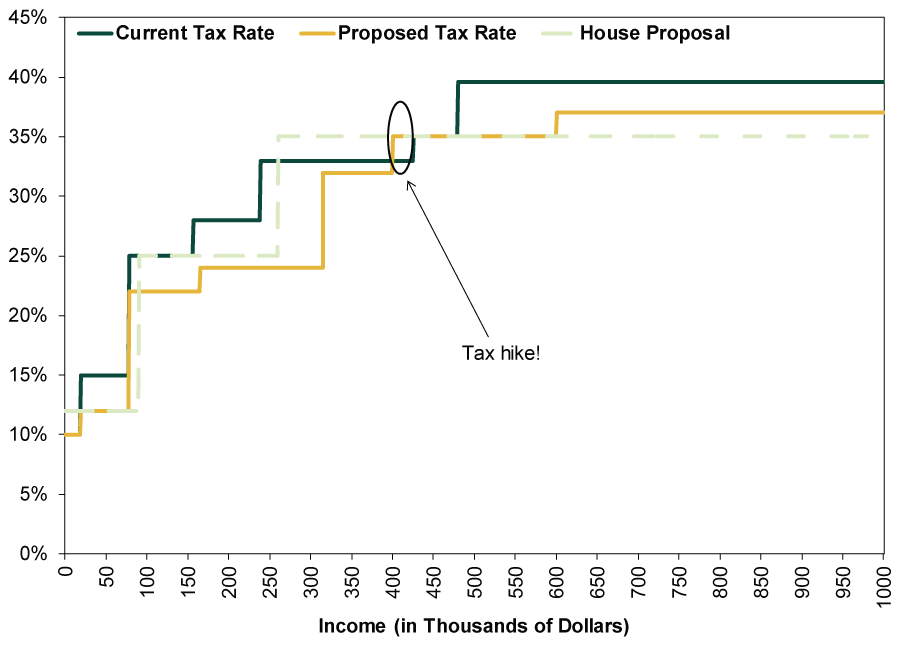

About the best we can say, at a general level, is that the pending bill creates winners and losers. Exhibits 1-3 show how income tax rates will change for single filers, heads of household and joint filers. For extra perspective, we showed how the final plan compares to the House’s bill. For many people, it cuts tax rates. But not for everyone. While the compromise bill reduces tax rates across the board, it also reduces the income threshold for some of the higher tax bands, hitting individuals making between $157,000 and $427,000 with a tax hike. Heads of household lose most of their filing advantages (and see a similar tax hike in that mid/upper income range), but joint filers get tax cuts across the board unless they make between $400,000 and $424,000.

Exhibit 1: Income Tax Changes for Single Filers

Source: Tax Foundation, as of 12/19/2017.

Exhibit 2: Income Tax Changes for Heads of Household

Source: Tax Foundation, as of 12/19/2017.

Exhibit 3: Income Tax Changes for Joint Filers

Source: Tax Foundation, as of 12/19/2017.

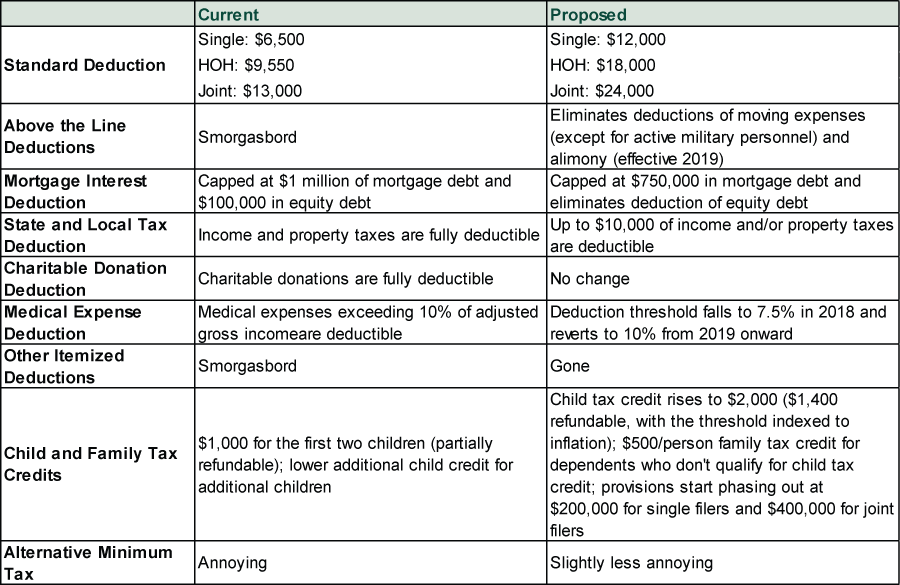

The kicker, of course, is that this refers to taxable income, which factors in your deductions. So even with tax rates higher on some incomes, there is still a chance folks in those ranges could pay less, depending on whether they itemize or use the standard deduction—this is why we said to talk to your tax advisor. Exhibit 4 shows how deductions would change under the GOP’s compromise bill.

Exhibit 4: Personal Income Tax Deductions

Source: Tax Foundation, as of 12/19/2017.

A couple noteworthy items to call out: The compromise bill allows folks to deduct up to $10,000 of state and local income or property taxes. The income part of this wasn’t in either the House or the Senate’s draft bills before, a source of significant consternation. Also, the Senate’s draft mandated the use of “first in, first out” taxation on securities, limiting investors’ ability to manage capital gains exposure. This was killed in the compromise bill. Additionally, the bill does include the repeal of the Affordable Care Act’s requirement that all Americans carry insurance, a matter sure to get lots of media attention.

For those whose deductions vanish at year-end or become less valuable once the pending changes take effect, it may be tempting to do a late-year scramble and take full advantage of the current system. We’ve seen some articles on how to do so, with this being but one example. Then again, as others have pointed out, the scramble may be overrated. Like, moving from a high-tax state to a low-tax state within the next 11 days probably isn’t feasible. Sooooooo, talk to your tax advisor.

As for the potential economic impact of potential income tax cuts, we think it is a stretch to expect some huge consumption boost. Yes, some households might have more after-tax dollars at their disposal, but that doesn’t mean they’ll spend their entire windfall. They might save it. Or invest it. Particularly since these tax cuts are set to sunset in 2025—that is the price the GOP had to pay for doing this on a partisan basis instead of passing it with 60 Senate votes. People, like businesses, are pretty good at gaming short-term tax changes.

Business tax reform is more extensive and complex. The headline corporate tax rate would fall to a flat 21%, and the corporate AMT would go bye-bye. But as with income taxes, Uncle Sam would make up for the lower headline rate by eliminating or reducing most of the deductions businesses use to avoid paying the infamous 35% current corporate tax rate—including capital investment depreciation, loss carrybacks and carryforwards and others. (See the Tax Foundation for more details.) Instead of taxing all international income at headline rates when repatriated, the plan adopts a territorial system—no blanket double taxation. However, a new “base erosion anti-abuse tax,” or BEAT, would ding firms who use transactions between foreign subsidiaries to reduce taxable income. The jury is still out on whether the final bill would inadvertently ensnare the $2.2 trillion repo market in BEAT, disrupting banks’ short-term funding, and banks are asking for guidance.

While some are enthusiastic about corporate tax cuts, we wouldn’t pencil in a huge investment surge. For one, given the measures taken to offset the reduction in headline rates, it is an open question whether businesses will save more from reduced tax burdens or a (somewhat) simpler tax code reducing accounting and compliance costs. Two, current after-tax income isn’t the sole driver of businesses’ investment decisions. Other factors loom larger in a long-term business plan, including demand, the economic outlook, expected return, interest rates (should they opt for debt financing), future taxation and others. Or, more simply, a business will build a new plant if they expect it to be profitable over time. If executives could be confident this corporate tax code will stick, with future profits taxed at 21%, it might help encourage long-term investments. But this sucker passed on partisan lines, making it easy for the next Democratic Congress to change it again along partisan lines. It is hard to plan when everything is in flux.

In our view, the most important thing about tax reform is that they did it. Not because it changes anything radically for the better, but because it is off their plate. Investors can move on from the debate and its associated uncertainty, which can help sentiment improve. Moreover, the GOP pretty much drained its political capital on this effort, the first “major” legislative achievement under the Trump administration. Without much public goodwill left—and with 2018 midterms creeping closer—lawmakers probably sit tight and do little of substance. The resulting gridlock should be bullish, keeping legislative risk low and giving investors one less thing to fear.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26 -

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today