Personal Wealth Management / Market Volatility

As Recession Fears Swirl, the Global Economy Grows

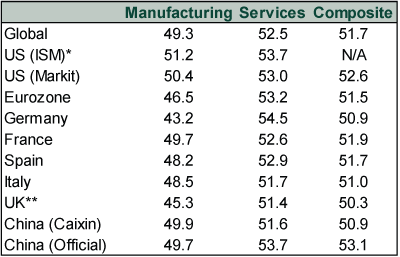

July PMI data tell the story of the global expansion in a nutshell.

Amid a volatile market stretch, worries about the global economy are running amok—including the dreaded “r” word: recession. Some economists think the likelihood of a US recession is up. Others see weak German industrial numbers and presume recession looms for Europe’s economic powerhouse. A few even project worldwide trouble. In our view, those concerns are overwrought. Recent data show continued global growth—despite pockets of weakness.

Our evidence: July purchasing managers’ indexes (PMIs). PMIs are business surveys covering major economic sectors like manufacturing and services. Businesses report their activity in a given month, and PMI aggregators crunch the numbers on how many respondents grew. Readings above 50 indicate more firms expanded; those below 50 suggest more contracted. While these monthly reports are a timely snapshot of broad economic conditions, they don’t share the magnitude of growth—or provide the level of detail “hard data” reports like GDP illustrate. With that said, July’s PMIs were consistent with the general theme of this year’s economic data: Heavy industry data were soft, but services expanded.

Exhibit 1: Around the World in July PMIs

Source: FactSet, IHS Markit, Institute for Supply Management, and National Bureau of Statistics of China, as of 8/7/2019. *In addition to services industries, US ISM’s non-manufacturing PMI also includes industries like agriculture, construction and mining. **The UK’s composite “All-Sector” PMI includes construction along with services and manufacturing.

Globally, industrial data have shown slowing in 2019, driving worries about a manufacturing “recession”—commonly defined as two or more consecutive quarters of contraction. While pundits are quick to blame “trade war” fallout, the manufacturing pullback stems mostly from other factors, in our view. China’s private sector weakness—spurred by last year’s shadow banking crackdown—hurt companies selling into China, notably in Asia and Europe. In Europe, auto production still hasn’t rebounded to early-2018 levels after the hit from last year’s change in EU emission standards.

Brexit uncertainty has been a notable headwind, too. UK businesses built up an inventory glut in anticipation of a potential no-deal Brexit scenario—pulling manufacturing activity forward, as well as imports from EU nations. UK trade data show EU imports rose ahead of March 29 (the original Brexit date) before plunging in April—and they have floundered since. After politicians pushed the original Brexit deadline back to Halloween, firms were left with a supply overhang, crimping production in subsequent months—likely a big factor behind the UK’s minor Q2 GDP contraction as well. The UK’s Office for National Statistics estimated inventory change subtracted about two percentage points from Q2 growth (after boosting Q1).[i]

Despite the manufacturing headwinds, major economies haven’t fallen off the rails. Outside the UK, countries reporting Q2 GDP—including the US, China and eurozone members France, Spain and Italy—expanded. The primary reason: Services comprise the lion’s share of GDP for the world’s biggest economies. While manufacturing weakness gets attention, services have quietly chugged along throughout this expansion. July PMIs seem like further evidence of this.

Exhibit 2: Services Dominate Major Economies’ GDP

Source: FactSet, European Central Bank, US Bureau of Economic Analysis, UK Office for National Statistics, National Bureau of Statistics of China, Economic and Japanese Cabinet Office—Economic and Social Research Institute, as of 4/18/2019. Eurozone manufacturing share of GDP includes construction. GDP growth rates as of 8/9/2019. *Annualized unless noted otherwise.

In our view, the global economy is faring better than many appreciate—and should continue to—despite less-than-stellar factory data. July manufacturing PMI New Orders subindexes remained in contractionary territory—perhaps a sign industry’s rut will persist for a while longer. But many July services PMI New Orders topped 50, pointing to further growth in major economies’ biggest sectors. In our view, recession worries amid underappreciated economic growth highlight the sizable gap between sentiment and reality—a sign the bull still has plenty of wall of worry to climb yet.

[i] Source: UK Office for National Statistics, as of 8/12/2019. Q2 GDP contribution from adjusted inventory change. https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/gdpfirstquarterlyestimateuk/apriltojune2019#large-movements-in-net-trade-and-gross-capital-formation-for-the-second-consecutive-quarter.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today