Personal Wealth Management / Market Analysis

Finding the Green Shoots in China

Recent Chinese credit data point towards future growth—a positive for the global economy.

China released a spate of economic data over the past week, including everyone’s favorite stat: GDP. Less noticed but more relevant for forward-looking markets and investors, in our view: recent credit data. March’s numbers are early evidence the government’s stimulus efforts may be starting to bear fruit—a positive development for global growth.

On the headline front, Q1 GDP expanded 6.4% y/y, repeating Q4’s growth rate and slightly beating forecasts of 6.3% (and, predictably, triggering a round of speculation over the data’s accuracy). Other figures released Wednesday topped estimates, too. March retail sales rose 8.7% y/y (consensus: 8.4%), while industrial production jumped 8.5% y/y (consensus: 6.0%). These numbers suggest China’s economy may be starting to stabilize after last year’s sharper-than-expected slowdown, although it will take a few months longer to confirm a trend.

In our view, any stabilization will depend on private firms’ ability to access credit as officials continue trying to ease the pain of last year’s crackdown on the shadow banking sector. In China, large, state-owned banks dominate the financial sector. They have historically preferred lending to state-owned enterprises, leaving small-to-medium-sized private businesses (SMEs) out in the cold. In the recent past, regulators encouraged private lenders to fill this need—causing the shadow banking industry to balloon. However, off-balance-sheet debt also skyrocketed, stirring fears of economic instability. As Research Analyst Scott Botterman wrote last year in his analysis, “Scaling a Wallop Potential: Chinese Shadow Banking”:

Accordingly, officials have begun unwinding the shadow banking sector and moving this type of activity back into traditional financial markets. Though the aim is fostering stability, it could create some unintended consequences as the new regulations phase in ahead of the June 2019 deadline.

One of those unintended consequences: Private SMEs, China’s main economic engine, got disproportionately knocked as their primary source of capital evaporated. With SMEs unable to access capital, growth slowed more sharply than anticipated throughout 2018. That slowdown had a global effect, knocking manufacturers and exporters with strong China ties—notably those in the eurozone and Japan. In response, China unleashed several fiscal and monetary stimulus packages late last year to boost domestic growth.

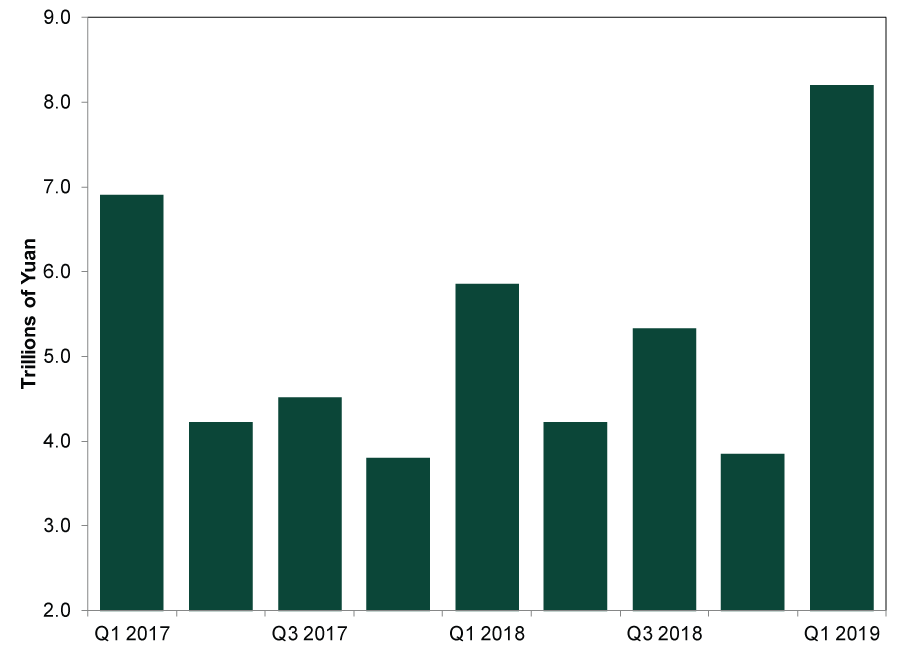

March credit data indicate the government’s efforts may have begun bearing fruit. New yuan loans hit 1.69 trillion in March—exceeding expectations of 1.2 trillion. Outstanding yuan loans rose 13.7% y/y, the quickest rate in three years and up from February’s 13.4% rate. M2 money supply growth accelerated to 8.6% y/y from February’s 8.0%, indicating money is moving through the economy. New total social financing (TSF), a broad credit gauge, hit 2.86 trillion yuan—a big increase from February’s 703 billion. That puts Q1 2019 new TSF at about 8.2 trillion yuan, dwarfing recent quarterly TSF amounts. (Exhibit 1)

Exhibit 1: New Total Social Financing, Q1 2017 – Q1 2019

Source: FactSet, as of 4/16/2019. Social Aggregate Financing to the Real Economy, Flows, quarterly, Q1 2017 – Q1 2019.

Though credit data have picked up, it is too early to know whether the money has made its way to where it is needed the most—the private sector. Some analysis suggested January and February’s credit boom still left many private firms out in the cold. One noted that, “… banks extended 1.913 trillion yuan of new long-term corporate loans in January and February, Wind data shows, about 4% less than in the same period a year earlier.”[i]

However, recent policy announcements brighten the outlook. The government is prioritizing lending to SMEs—indicating as much at this year’s National People’s Congress meeting. Policymakers have announced several programs aimed at channeling credit to small businesses. The China Banking and Insurance Regulatory Commission set a 30% growth target for loans to SMEs for large banks—a jump from 2018’s 21.8%. Per Fisher Investments research, hitting this goal would equate to adding about $400 billion worth of loans to SMEs—close to the contraction in shadow banking assets last year. The government has also implemented small business tax cuts, and the PBOC recently said it would help increase smaller banks’ lending capacity while also working to find ways to lower SMEs’ financing costs. These should all help channel money to private SMEs, though it may take a few months to consistently show up in the data, as measures like this typically work at a lag. Still, the green shoots in total lending are encouraging. The more money sloshing around China’s economy, the more that should filter through to SMEs.

Yet nothing here is new for forward-looking stocks. Global manufacturing weakness has dominated financial pundits’ takes for most of early 2019. It is likely priced in, sapping negative surprise power. Should reality turn out better than expected and China’s private sector recovers—benefiting foreign manufacturers—that could easily exceed dour expectations. That queues up a bullish upside surprise and is another reason to own stocks this year, in our view.

[i] Source: “China’s Entrepreneurs Are Left High and Dry Despite a Flood of Credit,” Shen Hong, The Wall Street Journal, 4/1/2019. https://www.wsj.com/articles/chinas-entrepreneurs-are-left-high-and-dry-despite-a-flood-of-credit-11554111004

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today