Personal Wealth Management / Market Analysis

Led Zeppelin

The dreaded Hindenburg Omen flashed Friday, but evidence shows little reason to fear this technical indicator.

The Hindenburg goes down in flames in 1937. Markets today likely don’t do the same. Photo by Central Press/Getty Images.

No word conjures visions of disaster quite like Hindenburg—exploding airship! Great balls of fire! So it’s no wonder investors got jittery when the technical indicator known as the Hindenburg Omen flashed Friday—no one wants the market to crash like the ill-fated zeppelin. However, evidence overwhelmingly shows this indicator has little predictive power, and fundamentals suggest stocks aren’t nearing a crash—this bull market has room to run.

For those unfamiliar, the Hindenburg Omen claims a crash is nigh if: the NYSE’s 10-week moving average is rising, at least 2.5% of the exchange’s companies hit 52-week highs on the same day another 2.5%-plus hit 52-week lows, the new highs aren’t more than twice as high as the new lows, and fewer stocks are rising. Or, more simply, if the market overall is rising, but company performance diverges and market breadth is narrowing, the rally’s supposedly out of balance and thus out of gas.

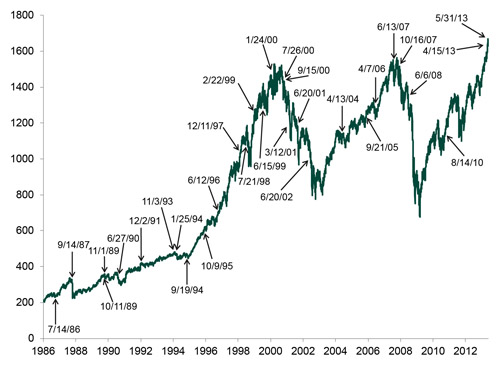

The Omen has flashed at previous peaks and during bear markets. But it’s also given many more false reads than accurate. As shown in Exhibit 1, which shows all Hindenburg Omen flashes and the S&P 500 Price Index since 1/1/1986, only 7 of its 28 pre-2013 signals were accurate.

Exhibit 1: S&P 500 and the Hindenburg Omen

Sources: St. Louis Federal Reserve; “The Recent Hindenburg Omen Observation,” Robert McHugh, Safe Haven; The Wall Street Journal; as of 5/31/2013.

A 25% success ratio is hardly compelling. But the timing of the false reads further skewers the Hindenburg’s credibility. For instance, it flashed in August 2010, before about six months of gains. It also flashed in April 2006, 18 months before the bull market ended, and numerous times during the 1990s—a phenomenal time for long-term growth investors to be in stocks. Simply, the Hindenburg Omen’s not reliably predictive, and on balance, basing portfolio decisions on it alone would be folly—you might miss some downside, but you’d miss even more upside, and you’d likely not know when to reinvest.

That’s true, in our view, of all such indicators, positive or negative—Golden Cross, Death Cross, Stick Sandwich, Bullish Homing Pigeon, Force Index (don’t use it, Luke) and more. All are backward-looking and claim some pattern of recent price movement dictates future returns. But markets don’t move on what they’ve just done—they’re forward looking. Stocks today likely don’t care that 90 NYSE stocks hit new highs and 156 hit new lows on Friday after weeks of gains. Markets care about what’s to come—namely, whether reality exceeds investors’ expectations.

Looking ahead, there likely remains plenty of room for reality to surprise to the upside. Sentiment’s turned optimistic in recent weeks, but it’s muted optimism and not universal—reality appears largely underappreciated. Future expectations seem cautious at best, and fear’s still prevalent. Many fret the Fed’s potential QE wind-down, believing QE’s the only thing supporting stocks—even though evidence overwhelmingly shows otherwise. There’s also chatter about rising interest rates hurting high-dividend stocks and a small recent uptick in mortgage rates choking off housing—both false fears, in our view, given the many drivers favoring blue chips globally and the fact mortgage rates remain near generational lows.

Meanwhile, corporate earnings keep rising, businesses are investing and buying back stock, banks are profitable and perhaps starting to lend a bit more, and the global economy remains in a sweet spot of fine growth and tame inflation—all bullish. That sentiment is only cautiously optimistic and fear persists suggests these positives aren’t yet fully reflected in stocks.

That’s not to say markets rise in a straight line from here—short-term wiggles are always possible, Hindenburg Omen or no. But overall, it seems highly unlikely stocks drop like a lead zeppelin. More likely, this bull market keeps chugging along

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today