Personal Wealth Management / Economics

Underappreciated—Not Underperforming

Recently released (and largely overlooked) economic data further illustrate the US economy’s underappreciated health.

In recent months, we’ve discussed many examples of a healthier US economy than is widely appreciated, like a strong private economy, a steadily expanding economy and healthy stock market gains. (For still more examples, see here, here, here, here and here.)Just in the last week, US housing and corporate earnings provided yet two more examples of the US economy’s underappreciated strength.

High-Rise Housing

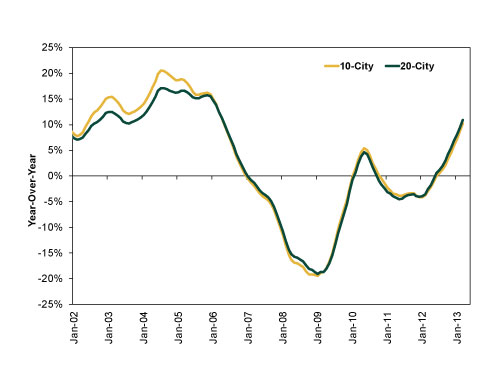

Housing continued improving in March, as the S&P/Case-Shiller Index—which tracks property values in 10 or 20 cities based on three-month averages—registered at 10.3% (10-city) and 10.9% (20-city), the highest for either since 2006. This particular index tends to lag, so improvements here mostly confirm improvements we’ve noted more broadly.

Exhibit 1: S&P/Case-Shiller Home Price Index

Source: Standard & Poor’s, Thomson Reuters, from January 2002 to March 2013, as of 5/18/2013.

While we consider this a positive, its effect on the larger US economy is likely limited. After all, housing’s a relatively smallish part of the economy. And it’s more likely overall US economic strength has created an environment in which businesses and individuals can funnel funds into attractively cheap housing, boosting the industry—not the other way around.

What we find more interesting is how easily housing’s improvement has been relatively dismissed after its previous weakness was lamented. For so long, many folks claimed housing was a huge negative for the larger US economy. We disagreed then as well. But, if weak housing was a big negative then, shouldn’t those same folks think improving housing is a big positive now?

They don’t, yet housing has been doing well and is poised for more growth. The number of houses on the market is near decade lows, and the number of homebuyers has been steadily rising, pushing prices higher. Borrowing costs are very low—the average 30-year fixed rate’s ~3.59%. Meanwhile, new and existing homes sales and building permit applications have also recently risen.

But hardly a peep more than a few technical reports announcing the data. To us, this indicates housing’s improvement is largely as underappreciated as the healthy economy that’s been providing it room to grow.

They’ve Earned It

Also largely underappreciated are US corporate earnings. As of May 24, 486 S&P 500 companies had reported earnings—66% of which beat analysts’ estimatesI. 66% may be less than the past four-quarter average of 67%, but it’s certainly better than the 63% longer-term average. In fact, Q1 earnings are expected to grow 5% y/y by the end of earnings season—solidly beating expectations.

5% y/y growth is pretty good this long into an expansion. And to us, US corporate earnings growth tells more about US economic health than headline GDP or unemployment—both of which are wonkily calculated. Sure, it’s not gangbusters or double-digits, but as the expansion matures, growth tends to slow down and get more differentiated. You see bigger, more quality firms having stronger, more stable growth. Which is one reason we continue to believe those super big firms should outperform the broad market—pointing to another area of the US economy poised for more growth.

In the end, US housing and corporate earnings are only pieces of the puzzle. But, taken with other continuously strong and/or improving metrics, the puzzle as a whole looks pretty healthy.

ISource: Thomson Reuters, “This Week in Earnings,” 5/24/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today