Personal Wealth Management / Market Analysis

The Bond Market Is Still Liquid

Bonds still have plenty of buyers.

Recent headlines have touted the Bank of Japan (BoJ) and Japanese insurers selling Treasurys—on top of the Fed’s slowly unwinding its quantitative easing (QE) purchases—and worried about a dearth of buyers drying up liquidity in the critical US Treasury market.[i] Some argue it risks a crisis. But this isn’t the first time such worries have cropped up. And, like in previous times when bond market liquidity fears surfaced, we think they hold relatively little water. Mostly we see the pessimism of disbelief at work here, not rising financial distress.

There is a long-running worry that bond markets might become illiquid—when selling can adversely affect the price, making it hard to exit a position—at the most inconvenient time, sending rates spiking and precipitating a financial crisis. Just when you want to take your money out, you can’t—at least not without a steep haircut. Evaporating demand and thin trading can cause bond prices—which move inversely to yields—to go haywire. When this happened in March 2020, it spurred Fed intervention. Or more recently across the pond, UK government bond volatility motivated the Bank of England to suddenly intervene.

Today, many argue the ground is shifting. The Fed isn’t buying Treasurys anymore—and it is unwinding the portfolio it amassed under its QE bond purchase program as assets mature. Meanwhile, the BoJ is selling down its Treasury reserves to support the yen. Without big central bank buyers to “backstop” the Treasury market, supply is (supposedly) starting to overwhelm demand, risking soaring yields—and plummeting prices.

Potentially driving the situation to a head: If the BoJ steps away from currency intervention and joins the rest of the world’s major central banks in raising rates. This in turn could make Japanese investors’ time-honored “carry trade”—borrowing at Japan’s low, low rates in yen, converting the proceeds to dollars and buying higher-yielding Treasurys for fun and profit—less fun and profitable. Ending this flow would (supposedly) be the nail in the coffin for global Treasury demand. Japanese insurers cutting their Treasury positions are allegedly an early indication of this.

A bit of perspective, though, defangs the fear, in our view. Let us do a little scaling to cut it down to size. Japan’s selling—or other big international Treasury holders doing so—isn’t new. China and Russia, for example, have substantially reduced their exposure in recent years without any untoward consequences. Chinese outflows left Japan as the biggest foreign Treasury holder with $1.2 trillion.[ii] But now even it is selling, having slashed $100 billion in holdings over the past year. Is $100 billion big? It may seem like it, but considering the Treasury market’s size—$24.4 trillion—it is a rounding error.[iii] Japan’s Treasury outflows are relatively tiny. Even in the unlikely event it sold all its holdings, at just 4.9% of the total, it wouldn’t be huge.

Now, Japan’s Treasury reductions have coincided with rising US rates. But Japanese fund flows didn’t drive them—for every seller, there is a buyer. What matters is what price they are willing to part with and pay, respectively. That, in our view, stems mostly from inflation, inflation expectations and the extent of rate hikes—bond markets’ main drivers everywhere. Yesterday’s inflation report underscores this, as yields plunged on the news.

The same logic goes for the Fed’s $95 billion monthly runoff—$60 billion in Treasurys and $35 billion in mortgage-backed bonds. The Fed currently holds a little over $8.1 trillion in total assets, down from its spring peak of around $8.4 trillion.[iv] Of this, $5.5 trillion is in Treasurys. That $60 billion runoff rate means about 1% of its initial Treasury holdings leave the Fed’s balance sheet monthly, a gradual start to a more than seven-year wind down if completed fully. It means that the stock of debt not owned by the Fed or federal government rises around 0.3% a month. Not only is this pace glacial, it is pre-priced. The Fed telegraphed its intentions well in advance, and while this could always change (see March 2020), we have seen this movie before—without a Treasury market crisis.

Meanwhile, consider: Daily Treasury trading volume averaged $574 billion in October and $622 billion year-to-date through then.[v] Well over half a trillion in turnover every day swamps the figures pundits concerned about bond market liquidity are talking about. Then, too, Treasury issuance (including new offerings to replace maturing bonds) has averaged over $1 trillion a month this year—and the auctions have been consistently oversubscribed. While they have consisted mostly of T-Bills (short-term paper funding government for one year or less), demand for longer-maturities has been—more or less—strong.

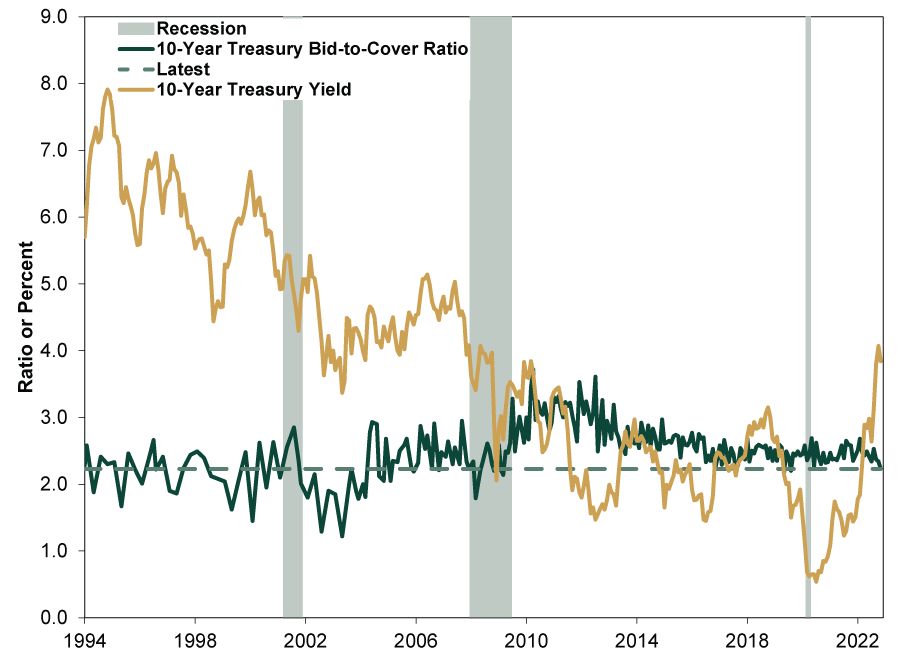

Take Wednesday’s $35 billion 10-year Treasury issuance, for instance. Coverage decried an “ugly” and “absolutely awful” auction because it drew a yield of 4.14%, an increase of about 3 basis points (0.03 percentage points) from 4.11% before the sale.[vi] This was as demand measured by the bid-to-cover ratio—the amount of bids received versus those accepted—hit 2.23, the lowest since August 2019. (Exhibit 1) Yet 10-year yields closed the day at 4.12%.[vii] A modest downtick in demand at one auction—or several—says little about yields’ direction. After all, the 1990s’ lower bid-to-cover ratios didn’t prevent rates from dropping during the decade. When all is said and done, demand for new Treasurys is regularly double the available amount and still frequently above 1990s levels.

Exhibit 1: Treasury Auctions Consistently See Bids Over Twice the Amount Offered

Source: Treasury and FactSet, as of 11/10/2022. 10-year Treasury bid-to-cover ratio and yield, January 1994 – November 2022.

In other words, the bond market seems plenty liquid to us. And that is in a period when bonds have overall been in a bear market. Mushrooming liquidity fears show sentiment continues to badly underrate reality—a positive development for markets. Perhaps, just perhaps, as reality likely disproves the notion Treasury liquidity is a huge risk now, people can get over this fear for the longer run.

[i] “Japan’s Waning Appetite for Treasurys Fuels Anxiety on Wall Street,” By Sam Goldfarb and Megumi Fujikawa, The Wall Street Journal, 11/8/2022. “Analysis: Nagging U.S. Treasury Liquidity Problems Raise Fed Balance Sheet Predicament,” Gertrude Chavez-Dreyfuss, Reuters, 11/8/2022. “Wall Street’s Alchemists Turbocharged Wild Swings in Treasuries,” Justina Lee and Liz McCormick, Bloomberg, 11/8/2022.

[ii] Source: US Treasury, 11/9/2022. Major Foreign Holders of Treasuries, August 2021 – August 2022.

[iii] Source: US Treasury, 11/9/2022.

[iv] Source: Federal Reserve Bank of New York, as of 11/9/2022. System Open Market Account Portfolio, 4/13/2022 – 11/2/2022.

[v] Source: Securities Industry and Financial Markets Association, 11/9/2022.

[vi] “Numbed Treasury Market Takes an Ugly 10-Year Auction in Stride,” Elizabeth Stanton, Bloomberg, 11/9/2022. “U.S. Treasury’s $35 Billion Auction of 10-Year Notes Was ‘Absolutely Awful,’ Says Bleakley’s Boockvar,” Staff, MarketWatch, 11/9/2022.

[vii] Source: Treasury, 11/9/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Chart of the Day: Oil’s Substitution Effects, Illustrated2026-06-03

-

Economics Rising Credit Card Delinquencies in Context2026-06-02

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today