Personal Wealth Management / Economics

The Fed’s Slimdown Is No SlimFast

The long-awaited balance-sheet unwinding has begun!

This person's diet plan was faster than the Fed's-and likely more impactful for stocks. Photo by Champja/iStock.

Well there you have it. In among the least-surprising central bank moves of all time, the Fed just announced it will begin unwinding quantitative easing (QE) next month, using the plan previewed in June. Unless you zoom in to about 1000x normal on a chart of the S&P 500, markets took the news in stride, which seems right to us. Not only was there zippo surprise power, but this is about the most gradual unwinding imaginable. This isn't Marriner Eccles jacking up reserve requirements in 1937 or Alan Greenspan inverting the yield curve in 2000. It is perhaps the slowest, most boring not-really-tightening of monetary policy in Federal Reserve history.

Usually Fed moves are unpredictable, but pretty much everyone saw The Great Balance Sheet Unwinding coming today. In June, the Fed said they'd probably start "normalizing" the balance sheet "this year." Many suspect Chair Janet Yellen won't make noteworthy moves unless she has a press conference scheduled, which took November off the table. December remained possible, but most Fed watchers expect a rate hike then, and Yellen is widely considered to worry about rocking the boat-so no "tightening" two'fer. That left September, and the good lady did not disappoint.

As they sometimes do on Fed Day, stocks took the smallest of dives in the minutes after the Fed's announcement. Between 11 and 11:30 AM PDT, the S&P 500 appeared to fall by 8 or 9 points-or about 0.36%.[i] That is a rounding error, not a drop. And by day's end it was over, with the S&P 500 finishing up a whopping 1.59 points on the day, or 0.06%.[ii] Another rounding error. 10-year US Treasury yields rose all of four basis points to finish the day at 2.27%, well below where they began the year.[iii]

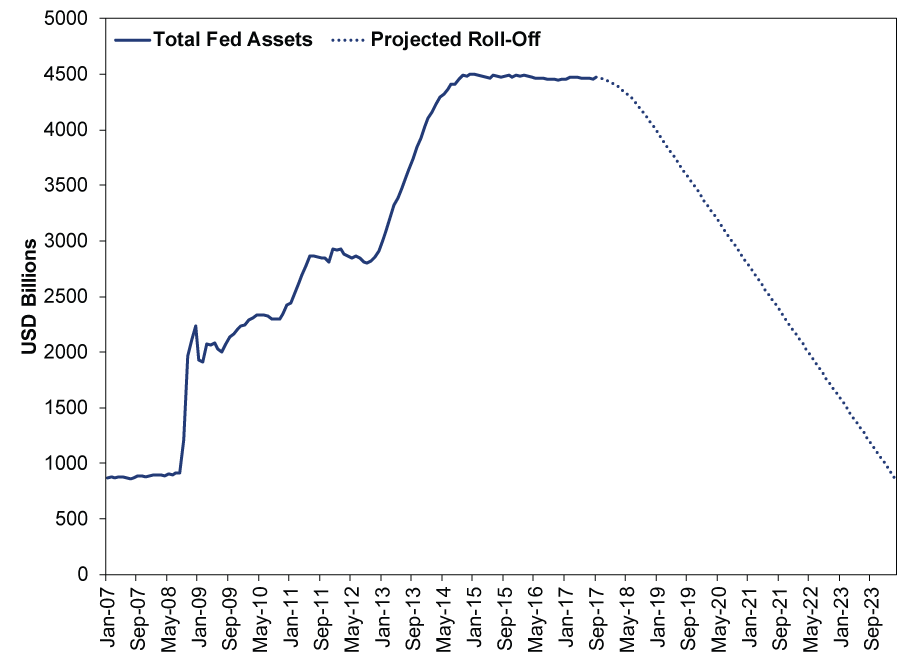

The sanguine non-reaction seems about right to us. As we've detailed a few times in recent months, both here and on our Headlines page, this is about the slowest balance-sheet unwinding the Fed could have concocted. Even if you believe QE was massive stimulus (SPOILER ALERT: we don't), you can't argue this amounts to suddenly yanking said stimulus. The Fed isn't selling assets. Instead, as bonds on its balance sheet mature, policymakers will gradually stop reinvesting the proceeds. In October, they'll let $10 billion go un-reinvested ($6 billion in Treasurys; $4 billion in mortgage-backed securities). They'll repeat that in November and December, then increase the roll-off to $20 billion monthly. They'll raise that cap by $10 billion once a quarter until it reaches $50 billion in Q1 2019. At that point, presuming they haven't changed course, they'll let the balance sheet shrink by $50 billion monthly until some unspecified point. By our math, if they keep at it, they'll be back at pre-QE levels sometime around St. Patrick's Day in 2024.

Exhibit 1: Balance Sheet Boredom and Straight-Line Math

Source: Federal Reserve Bank of St. Louis and Math, as of 9/20/2017. Total Fed Assets, monthly, January 2007 through September 13, 2017 and hypothetical extrapolation thereafter.

Now, as we've written here dozens of times, we aren't in the QE fan club, and we're keen to see it go the way of cassette tapes and the 8-track. When the Fed bought long-term assets, it reduced long-term interest rates and the yield curve spread. Since banks borrow at short rates (think: deposits, commercial paper and other bank funding activities) and lend at long rates (mortgages, corporate loans, etc.), the spread represents their potential profit. Shrink profits and banks lend less, which slows growth in a fractional reserve banking system like ours, where lending is the main engine of broad money supply growth. So we weren't surprised at all when lending sagged during QE and improved as the Fed first tapered, then ultimately stopped increasing its holdings.

We'd love to say shrinking the Fed's balance sheet will be massively bullish because it will let the yield curve steepen, but we can't. While it's fair to say the Fed's move will probably have some marginal impact on long rates, it is too small to do much. They'll still be buying some long-term Treasurys and mortgage-backed securities to replace maturing ones-just fewer than before. So maybe you get less Fed downward pressure on long rates, but this isn't some massive push higher. While that's a bit of a downer for those who would like to see the yield curve steepen, it should also placate widespread fears of higher rates and a bond market bloodbath. This is too incremental and slow to tip the scales.

It's also too well-known. Fixed income and stock markets move most on surprise-the gap between reality and expectations. The Fed's ultra-transparency here saps surprise power. Then, too, markets don't discount the far future. If you're worried about what happens when QE is entirely erased, well, that's at least six and a half years away-longer if the Fed decides it has slimmed enough or changes course for some reason. After all, there are currently three open seats on the Fed Board of Governors, and Yellen's future remains shrouded in mystery as the world waits to see whether President Trump will reappoint her. We could have entirely new cast of characters at the Fed in 2024! Trump could be on his late-second term victory lap, or we could have President Kanye West! Senator Kid Rock could be on the banking committee! Who even knows how that would impact Fed personnel and policy. Heck, we could all be rolling in bitcoins by then and laughing at the quaint old days when we had a dollar, a Fed and monetary policy as we teleport to Elon Musk's Martian Colony and text telepathically using the computer chips and SIM cards that will no doubt be embedded in our brains.

All kidding aside, markets usually look about 3-30ish months ahead. The Fed's charting a stable, predictable course over that period perhaps slightly eases the risk of a sudden monetary policy error, which is a positive. That said, it doesn't erase Fed risk. They could still hike too much and invert the yield curve, mess with reserve requirements, enact imprudent macroprudential regulations, do something nutso with the interest rate on excess reserves, or or or. Fallible humans are all too capable of error. But for now, we just don't see balance sheet slimming as a reason to fear the Fed.

[i] Source: Squinting really hard at a zoomed-in chart on FactSet and then doing math.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today