Personal Wealth Management / Politics

What Now for Brexit?

Brexit uncertainty may linger a wee bit longer, alas.

The UK’s Parliament conducted its latest “meaningful vote” on Brexit Tuesday. On the bright side for Prime Minister Theresa May, who won a few concessions from Brussels overnight in hopes of rallying lawmakers to her side, more members of Parliament (MPs) voted for her deal than in the last vote. On the not-so-bright side, the No votes dropped from 432 to 391—still far exceeding the 242 Yes votes. For markets, this widely expected defeat merely extends the status quo of Brexit uncertainty. We remain of the opinion that the sooner this all ends, the better—regardless of the actual outcome—so that investors and businesses can get on with life. But the road there could go a number of ways.

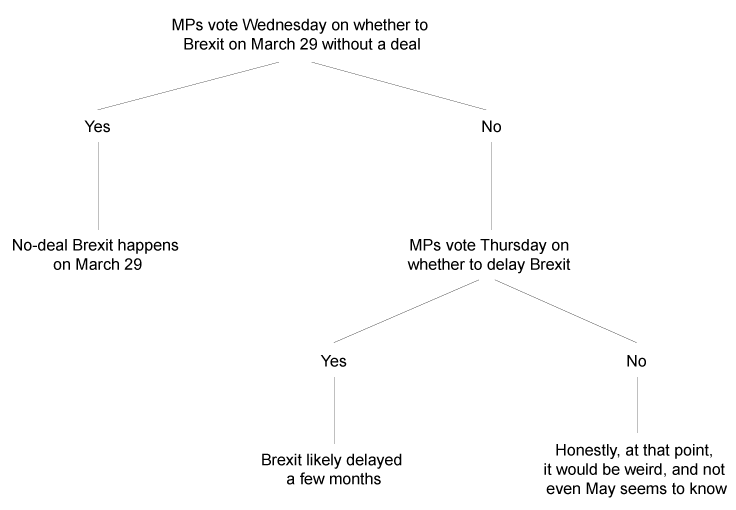

On paper, the next steps are as follows:

Exhibit 1: Your Handy Brexit Vote Flowchart

Source: The Right Honourable Theresa May MP, as of 3/12/2019. We didn’t talk to her directly, but we combed transcripts of things she said.

As we write, most observers agree MPs will likely shoot down a no-deal Brexit tomorrow. Overall, at this point, we reckon markets would probably prefer ripping the Band-Aid off, no-deal Brexiting in 17 days, reverting to WTO trading rules (and, if last week’s leaks are reliable, moving to zero tariffs or close to it on about 90% of all imports). Then we all move on. Uncertainty would be gone, and businesses could finally unleash long-term investments. But politicians have a knack for a) making things difficult and b) striving for re-election. Voting for an outcome Brits have spent the past year hearing would be tantamount to economic suicide doesn’t seem like a great way to do well at the next election. So, a no-deal Brexit probably bites the dust Wednesday.

Assuming that, May and others are acting like a delay is a foregone conclusion. EU leaders have said they’re open to the notion of buying a few more months to overcome stumbling blocks and reach a deal a majority of MPs can live with. But how this works in practice isn’t clear. May thought she had a victory last night, when European Commission President Jean-Claude Juncker agreed to “legally binding” assurances the UK could leave the Irish Backstop, preventing the UK from being tied indefinitely to the EU’s customs union. That all seemed skippy enough until this morning, when UK Attorney General Geoffrey Cox, he of the colorful metaphors and Twitter feed, released his official legal advice on the changes and declared they did not, in his opinion, give the UK leave to exit the backstop unilaterally. That was enough to tip euroskeptic Tory MPs and Northern Ireland’s Democratic Unionist Party, which props up May’s minority government, into the No column.

The trouble with all of this is, EU leaders have already said the deal is closed and won’t be reopened a third time. Now, we realize they said this before it was reopened a second time, and they, too, are politicians, so a U-turn is entirely possible. But one wonders what concessions May will receive within the next few months that she didn’t get this time. Then, too, May isn’t guaranteed to be the one to do the negotiating. Some MPs within and outside her party are already calling for her ouster, and a no-confidence vote is possible. Her cabinet could also strong-arm her into resigning, triggering a Tory leadership challenge and, potentially, a contest for a job no one seemingly wants. A snap election is also possible, though less likely, as a majority of MPs seem keen on doing whatever it takes to minimize the likelihood of a Labour Party run by Jeremy Corbyn taking the reins. We suspect Corbyn himself doesn’t want the role of prime minister right now—or even to fight a snap election—as he has already pledged to push for a second referendum that he doesn’t really want in order to keep Labour’s hip, urban, pro-EU young voters in the fold. Our best guess? May or some poor Tory successor goes another few rounds with Brussels, chipping away at the opposition within Parliament until the vote finally swings toward a deal that bears a strong resemblance to what MPs voted on today. However, that could change.

For markets, this means uncertainty lingers a while longer. This isn’t wonderful news, as prolonged uncertainty has already weighed on the UK economy. Witness business investment falling four straight quarters in 2018. GDP has continued growing, demonstrating the economy’s resilience, and growth even accelerated in January (though we wonder how much of that is due to pre-Brexit inventory builds, particularly within the pharmaceuticals industry). Given the country’s ability to keep eking out growth amid the fog, a short delay isn’t the end of the world. Plus, if nothing else, this is all a very orderly form of chaos—predictable uncertainty for markets, for what that is worth. That said, the day they finally get over this hump, kicking all major questions out another couple years (to the end of the transition period), will likely be a very happy day indeed.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today