Personal Wealth Management / Market Analysis

Will the Fed Hike the Dollar Higher?

An initial Fed rate hike doesn't automatically mean a stronger dollar.

Is the Fed about to make the dollar too strong? We aren't sure what that means since currencies are only strong (or weak) relative to other currencies. But that doesn't stop folks from fearing it. Amid all the chatter and speculation about the fallout from an upcoming initial Fed rate hike, many assume the dollar will get even stronger as a result-a negative, since an already-strong dollar allegedly hurts American businesses. Now, we have spilled many words battling various misperceptions surrounding both the strong dollar and an initial Fed rate increase. Here are some more: Assuming a strict cause-and-effect relationship is a stretch, in our view. History shows the dollar doesn't automatically strengthen after a rate hike.

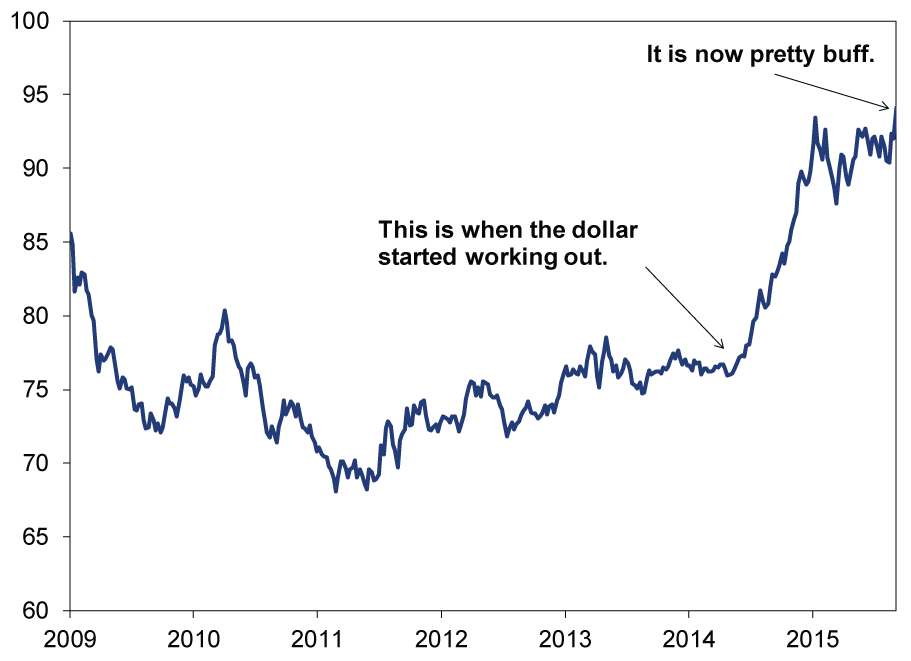

The concern stems from global monetary policy. Other central banks, namely the BoJ and ECB, are pursuing "ultra-easy" monetary policy with quantitative easing (QE) and the world's lowest overnight rates. US overnight rates-currently 0-0.25%-are also historically low but modestly higher than Europe and Japan, and a small rate hike would of course make them even higher. All else equal, money flows to the highest-yielding asset, and a tighter Fed policy would ultimately boost yields and, theoretically, demand for dollars. And with the dollar already strong (Exhibit 1), folks fear a rate hike would make the US's currency even mightier-exacerbating problems that a strong dollar allegedly causes.

Exhibit 1: Trade-Weighted US Dollar Index (Major Trading Partners) During Current Bull Market

Source: St. Louis Federal Reserve, as of 11/10/2015.

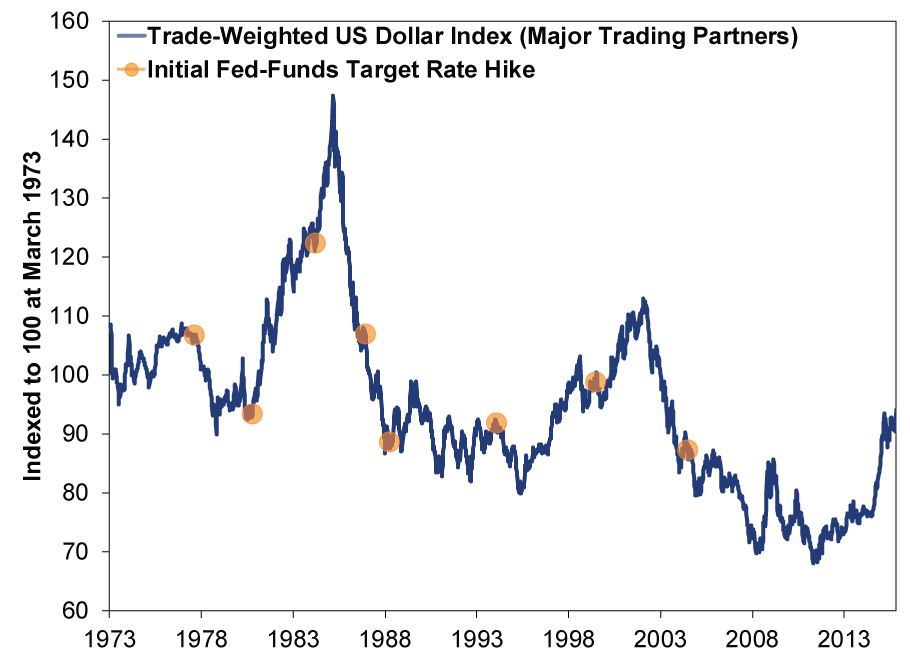

Hold your horses, though. If an initial rate hike alone caused the dollar to strengthen, history should confirm this relationship. But it doesn't. (Exhibit 2)

Exhibit 2: Trade-Weighted US Dollar Index (Major Trading Partners) Since 1973

Source: St. Louis Federal Reserve, as of 11/10/2015. Initial Fed rate hike dates since the inception of the US Dollar Index are: 8/16/1977; 10/21/1980; 3/27/1984; 12/16/1986; 3/29/1988; 2/4/1994; 6/30/1999; and 6/30/2004.

Eight data points isn't a huge array to draw big conclusions from, but even in this limited sample, the data don't support the conclusion a rate hike cycle means a stronger dollar ahead. In 1980, 1984, 1988 and 1999, it strengthened-four of eight, or exactly half the time. In 1977, 1986, 1994 and 2004, the dollar weakened sharply after the Fed first hiked rates. Heck, in 1994, it overall weakened throughout the seven hikes in the tightening cycle that ran from February 1994 - July 1995. It then strengthened significantly over the next three years, when the Fed was overall cutting rates.

There are several contributing factors behind these inconclusive results. But a key one worth considering today: Markets move in advance of widely discussed events, and a Fed rate hike has been one of the most widely discussed events in recent years[i]-it isn't sneaking up on anyone. So while it is unknowable to what degree, it is quite possible some of the dollar's strength from over the past year-plus is tied to markets pre-pricing higher US rates. The fact you can't forecast the Fed doesn't stop some folks from trying. So we aren't convinced the dollar will automatically strengthen when the Fed hikes rates this round. Plus, lifting short rates from 0-0.25% to 0.25% flat (or whatever similar move the Fed might cook up) doesn't really change the supply/demand factors all that much. The dollar is already modestly higher-yielding than most of Europe and Japan. British overnight rates, currently 0.5%, will likely still be modestly higher (though UK long rates are a bit lower). And again, markets are already well aware of this.

More importantly, whether the dollar strengthens further or weakens when the Fed finally hikes, the event isn't likely to roil markets. Despite all the fears, the strong dollar has yet to derail the current expansion or bull market (or any prior ones for that matter). Whether it strengthens or weakens from here, we don't see that changing. As we've written many times, a strong dollar isn't a huge earnings drag. Even though a stronger dollar knocks foreign sales a bit, it also reduces overseas costs (like parts, shipping or labor). The result is often a wash-not a negative imperiling US multinationals. Similarly, as we've frequently argued, an initial Fed rate hike is no deathblow to capital markets or economic growth. If the Fed would finally get on with it and hike, it would likely remove a long-persistent false fear-a positive for investors.

While some sentiment-driven short-term volatility could always arise related to the Fed hiking rates (or not), it doesn't negate the many positive drivers underpinning this bull market-and that's including whatever the dollar does from here.

[i] Coming in first: Politicians bickering.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today