Personal Wealth Management / Market Analysis

Your Half Yearly Checkup on the US Economy

At 2018’s midpoint, the US economy is chugging along.

With the first half of 2018 in the books, the state of the US economy is up for debate. Growth seems to have accelerated in Q2, so should we cheer it—and expect more of where that came from? Or is the optimism unwarranted, with a slowdown looming? In our view, debating over the pace of growth misses the more important point for investors: The US economy is on sound footing and the expansion looks likely to continue for the foreseeable future.

Ask a number of experts for their thoughts on the US expansion, and you will likely get a number of different prognoses. Bulls might argue tax reform and the overall friendlier business environment are paying dividends and will continue doing so. Bears may suggest growth will slow for a number of reasons: The Fed is raising interest rates and tightening monetary policy; tariffs raise uncertainty and implementation potentially discourage business activity; tax reform provides only a one-time boost unlikely to repeat, especially if tariffs offset its benefits. This camp sees the current uptick as a “temporary blip in growth.”

Even different Federal Reserve Banks have seemingly conflicting opinions. The Atlanta Fed’s most recent “GDPNow” estimate puts Q2 2018 GDP at a 4.1% annualized rate. If that estimate holds, it would be a big acceleration from Q1’s 2.0% and the fastest since Q3 2014’s 5.2%. In contrast to “Hotlanta,” the New York Fed’s “Nowcast” report projects a less spicy 2.8% growth (which would still be a pickup from Q1). So who is right? The different interpretations each carry their own biases, so when in doubt, look at the data.

Though we won’t have the BEA’s official Q2 numbers until the end of July, we can be fairly confident GDP was positive for the quarter. The Atlanta Fed’s GDPNow mimics the BEA’s estimates and tracks the subcomponents that comprise GDP. In contrast, the NY Fed’s Nowcast uses a modeling strategy that follows the “best practices” used for many macroeconomic forecasts globally. These estimates are still usually off from the actual reading by some amount (and even further off after revisions hit), but based on the economic data released throughout Q2, US GDP likely grew. That would officially make the current economic expansion nine years old. (Happy Birthday, US economic expansion!)

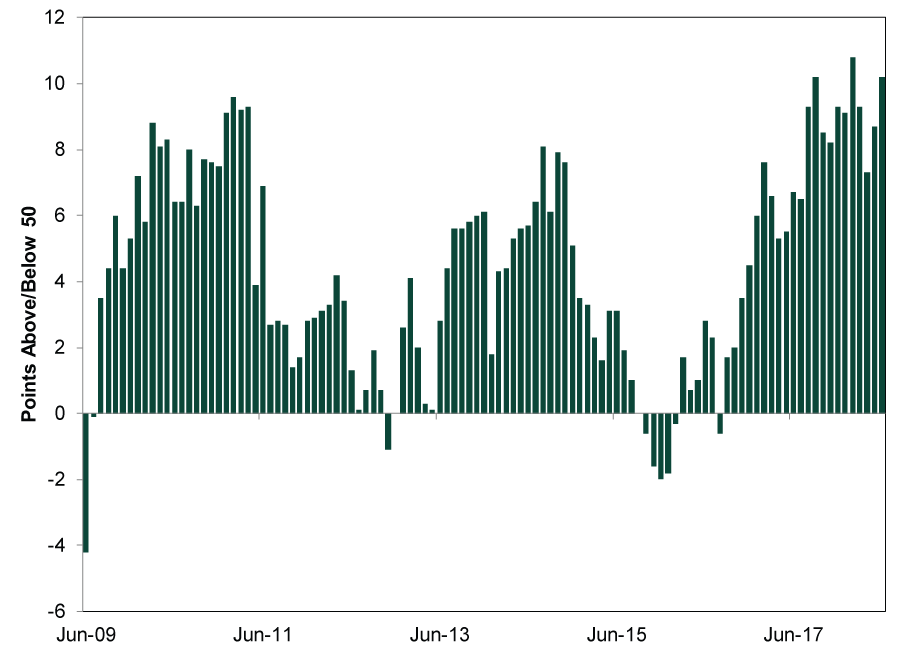

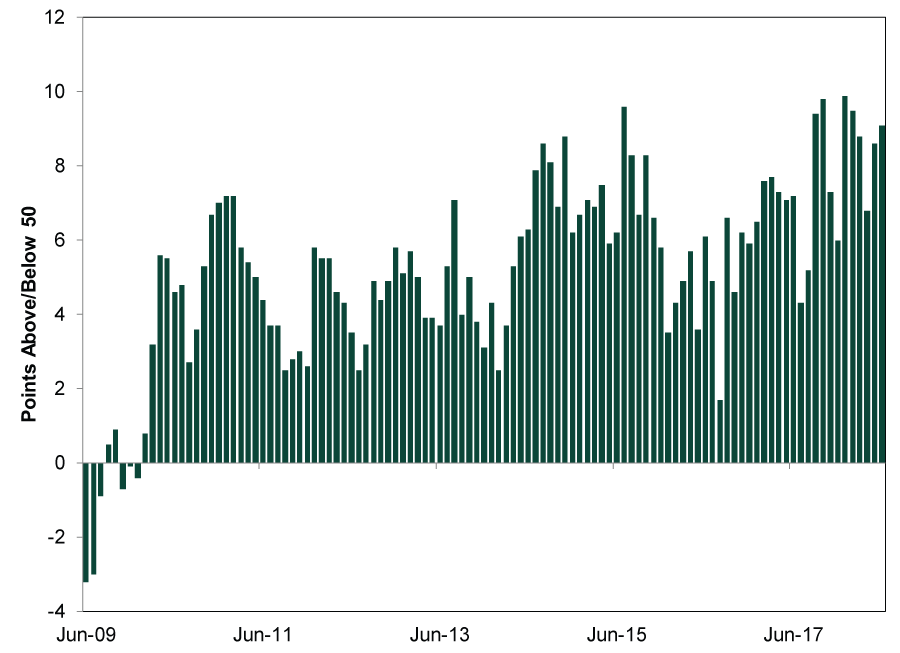

Besides official GDP components, other data point to growth as well. The Institute for Supply Management’s (ISM) manufacturing and non-manufacturing purchasing managers’ indexes (PMI) for June hit 60.2 and 59.1, respectively.[i] Readings above 50 indicate more businesses expanded than contracted, and PMIs for both sectors have been well in expansionary territory recently. PMIs aren’t perfect since they are survey responses that indicate the breadth, not magnitude, of growth. However, they provide a helpful snapshot of how the US’ private sector—the economy’s growth engine—is doing.

Exhibit 1: ISM Manufacturing PMI Since June 2009

Source: FactSet, as of 7/5/2018. June 2009 – June 2018.

Exhibit 2: ISM Non-Manufacturing PMI Since June 2009

Source: FactSet, as of 7/5/2018. June 2009 – June 2018.

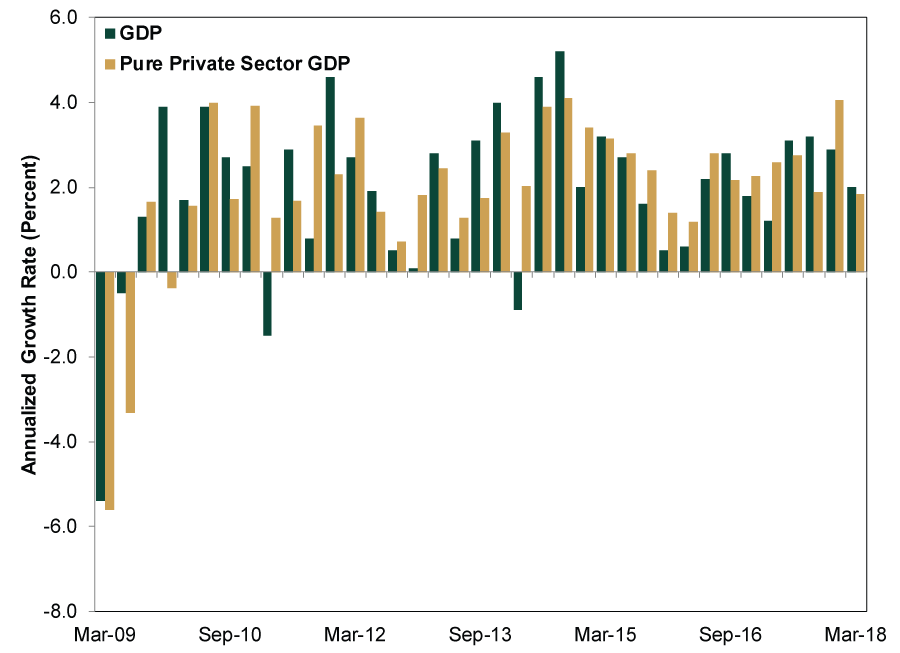

This growth is consistent with official BEA numbers, too, whether you look at headline GDP or “Pure Private Sector GDP” (which cuts away the noise by focusing on consumer spending, non-residential fixed investment[ii] and residential fixed investment).

Exhibit 3: US GDP and Pure Private Sector GDP Since Q2 2009

Source: Bureau of Economic Analysis, as of 7/3/2018. From Q1 2009 – Q1 2018.

While recent growth is aligned with the longer-term trend, that alone doesn’t tell you much about the future. Looking ahead, though, forward-looking indicators suggest US economic growth should continue chugging along. The new orders subindexes of June’s manufacturing and non-manufacturing PMIs were a robust 63.5 and 63.2, respectively. Today’s orders are tomorrow’s production, which bodes well for future growth. The Conference Board’s forward-looking Leading Economic Index (LEI) for the US rose 0.2% m/m in May—adding to its long uptrend. In LEI’s 50+ year history, no recession has started when the gauge was high and rising. Moreover, the interest rate spread was the biggest contributor—a sign lending remains profitable for banks.

While that interest rate spread has narrowed recently—spurring concerns over a flatter yield curve—flat doesn’t equal inverted. Banks still have incentive to lend, if a bit more judiciously.[iii] Partner that with benign inflation and steadily growing money supply, and you have a Goldilocks setting in which the economy isn’t running too hot or too cold. In our view, stocks can do great in this type of environment—businesses are not only profitable, new business activity is also likely to rise for the foreseeable future.

The upshot: The US economy should remain a big contributor to the broader global expansion, which also looks healthy. This seems like a bullish cocktail to us, especially when sentiment globally remains low as fears over tariffs and other political developments dominate headlines. This disconnect between sentiment and reality is a big reason we remain bullish for the rest of the year.

[i] Source: Institute for Supply Management, as of 7/5/2018.

[ii] Also known as business investment.

[iii] Much of this fretting targets the 10-year Treasury minus the 2-year, but we believe this is a less accurate way to view it than the 10-year minus the 3-month (or fed funds target rate). This is because banks typically fund loans by borrowing overnight or at shorter maturities than the 2 year.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today