Personal Wealth Management / Economics

GDPNow Says Little About the Future

Nowcasts may give an early look at what GDP may be, but markets are looking further ahead.

Where is GDP at now? Helpfully, the intuitively named GDPNow gives an answer—the Atlanta Fed’s model takes incoming economic data and uses past historical relationships to provide a nowcast estimate of the quarter’s growth. It evolves with releases throughout the quarter, a way to see how data are shaping up in summary form. But don’t take it to the bank. Fed models—and economists’ forecasts generally—are imperfect. They also reflect available data markets have already digested, making them a fun digest for investors—but little more than that.

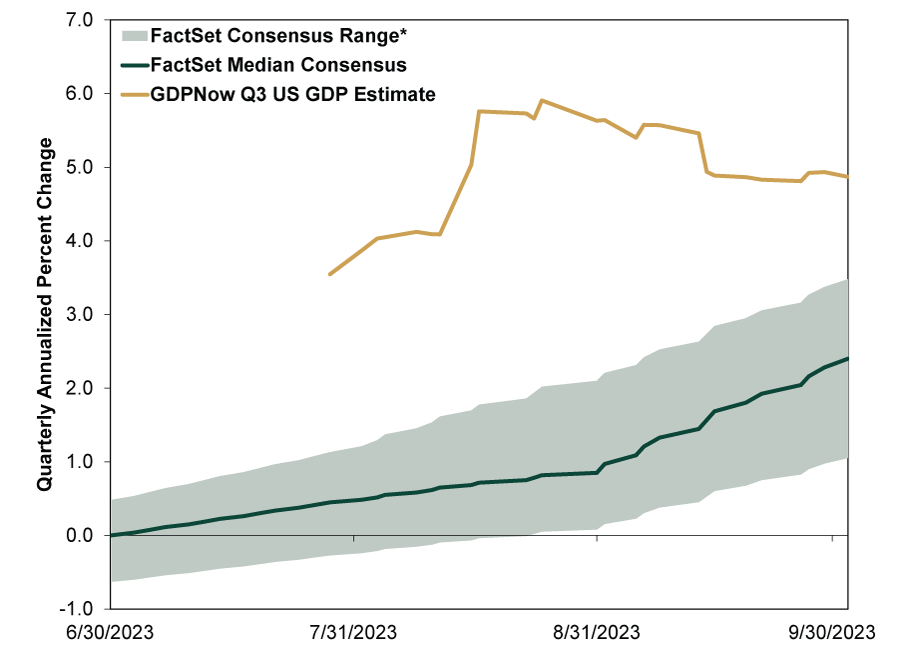

Over the last few months, GDPNow has raised eyebrows, projecting Q3 GDP growth well above economists’ estimates. (Exhibit 1) With September data still outstanding, GDPNow currently suggests 4.9% annualized Q3 GDP growth (yellow line). This comes alongside many economists dialing up their Q3 growth forecasts (green line), from zero at the quarter’s start to around 2.4% annualized at quarter end. Notably, their sunnier disposition apparently extends to the Fed’s staff economists, who dropped their recession forecasts at July’s end after calling for a “mild” one in March.[i]

Exhibit 1: Evolution of Atlanta Fed GDPNow Q3 GDP Estimate

Source: Federal Reserve Bank of Atlanta and FactSet, as of 10/2/2023. *Range of top 10 and bottom 10 average forecasts.

GDP growing consistently above 2% annualized since Q3 2022 also cuts against The Conference Board’s Leading Economic Index (LEI) readings over the last year. Through August, LEI fell 17 straight months (since April 2022), whereas it is supposed to lead “turning points in the business cycle by around 7 months.”[ii] This speaks to the fact GDP better captures the services industry than LEI, which is manufacturing-heavy—LEI’s biggest weak spot, in our view.

What to make of all these competing growth projections? First, GDP itself is a backward-looking indicator. The Bureau of Economic Analysis’s (BEA) preliminary “advance estimate” comes out almost a month after quarter end. Q3’s release is October 26, quite a late lag—and still a moving target long after the fact. It is subject to at least two more revisions (through December 21’s third estimate) before all is said and done.

GDPNow appears to improve on this by extrapolating much of the same incoming data that go into GDP into a real-time gauge. But we would caution: Quantitative models—while seemingly impartial—aren’t any more prescient than economists’ forecasts; they, too, are only ever opinions, their biases are just hidden in models’ assumptions.

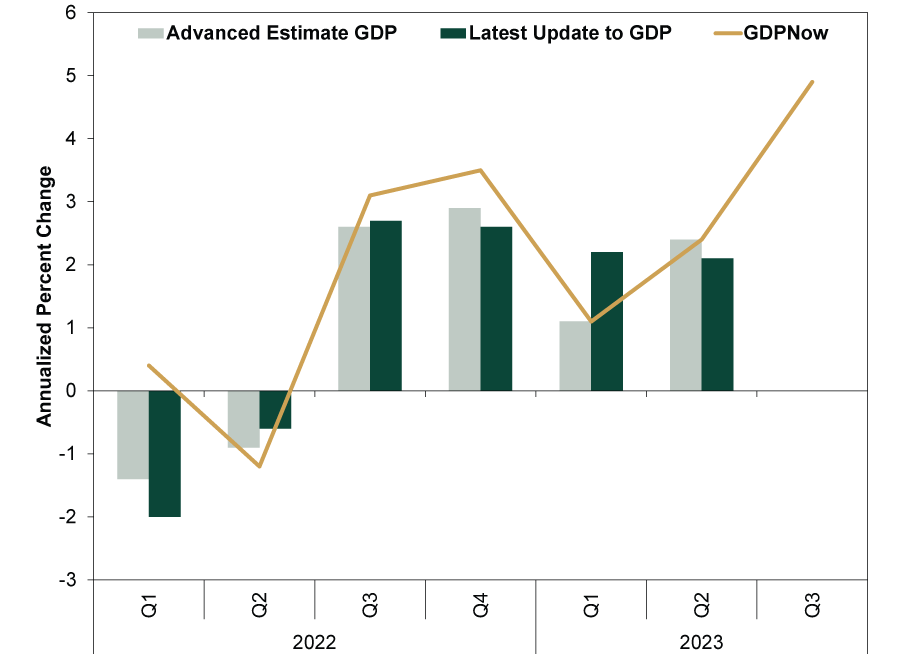

Even if mechanical, GDPNow—like all models—is prone to error. In Q2, for example, GDPNow initially estimated 1.7% annualized GDP growth in April, but it stood at 2.4% in July on the eve of the actual report—which it nailed! (Exhibit 2) The advance estimate for Q2 GDP was 2.4% annualized—however, the BEA subsequently revised this down to 2.1%.

Exhibit 2: GDPNow Guestimates

Source: Federal Reserve Bank of Atlanta and FactSet, as of 10/2/2023.

Or take Q1 GDP. In mid-March, GDPNow was looking at 3.2% annualized growth. But this fell to 1.1% annualized by late-April’s Q1 GDP advance estimate release—which, ta-da, was also 1.1%—only it didn’t stay that way (again). The BEA later revised Q1 GDP all the way up to 2.2% annualized (on September 28, in Q2 GDP’s third estimate).[iii] While nice that GDPNow tends to converge on the BEA’s advance estimate—as more data become available—it moves a lot during (and after) the quarter and often doesn’t bear much resemblance to the BEA’s subsequent revisions.

So how close will GDPNow’s present 4.9% annualized estimate for Q3 GDP be to reality (or at least the BEA’s continually updated version of events)? A lot depends on September’s data—forthcoming throughout this month. Then, too, besides the Atlanta Fed’s GDPNow, other Fed districts have their own (wildly varying) nowcasts. The New York Fed’s is currently looking at 2.1% annualized, while the St. Louis Fed’s projects 1.6%.[iv] And those are just some of the Fed’s more widely watched ones. There are more on the private side: Moody’s Analytics High Frequency GDP Model is at 3.7% annualized, and Bloomberg Economics’ US GDP Nowcast is “about” 3%.[v] Never mind the plethora of private-sector forecasts and surveys incessantly making the rounds. All to put a number on what is now in the rearview!

But here is the thing for investors: Even if gussied up and massaged mathematically, GDPNow and its siblings are based on available data—which markets have long since priced. Stocks are looking further ahead at how economic (and political) factors are likely to affect earnings over the next 3 to 30 months versus what they already expect. GDPNow (alongside other nowcasts) may provide a useful signal of what data in total are showing—before the official GDP report. And this can influence sentiment and expectations along the way.

But an aggregation of backward-looking data, and an imperfect one at that—no matter how they are sliced and diced or combined and recombined—doesn’t fundamentally yield much new information to forward-looking markets, which move most on surprise. As all the attention and effort at divining GDP’s path show, stocks relentlessly pre-price all that data and then some (opinions, forecasts and attitudes about them) well ahead of time, to the point that GDP—and estimates thereof—are usually among the least shocking econometrics markets encounter.

In that context, don’t get carried away with GDPNow (or nowcasting generally for that matter). Instead, hard as it is, focus on conditions 3 – 30 month out, like stocks do—which, short-term volatility aside, we find are better than any model or forecaster.

[i] “Fed Staff Drop US Recession Forecast, Powell Says,” Staff, Reuters, 7/26/2023.

[ii] “LEI for the US Fell Again in August,” Staff, The Conference Board, 9/21/2023.

[iii] Source: BEA, as of 9/28/2023.

[iv] Source: Federal Reserve Banks of New York and St. Louis, as of 10/3/2023.

[v] “US High Frequency GDP Model,” Matt Colyar, Moody’s Analytics Economic View, 10/2/2023. “Fed Can’t Disregard Another Inflation Head Fake,” Jonathan Levin, Bloomberg, 9/6/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today