Personal Wealth Management / Market Analysis

Does a Strong Dollar Favor Smaller?

We investigate the claim that a strong dollar will kill large-cap US stocks.

Will the almighty dollar crush earnings? Photo by Scott Eells/Bloomberg via Getty Images.

One month into 2015, three factoids are hogging attention: The dollar is up, earnings growth is slowing, and small cap has outperformed. Some pundits are connecting these and extrapolating this very short-term trend forward[i], claiming the strong dollar is hammering US multinationals' overseas revenues, putting large-cap stocks at a relative disadvantage-and projecting small-cap leadership from here out. However, history and actual data show this theory doesn't hold water. The outlook for large US stocks remains bright.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

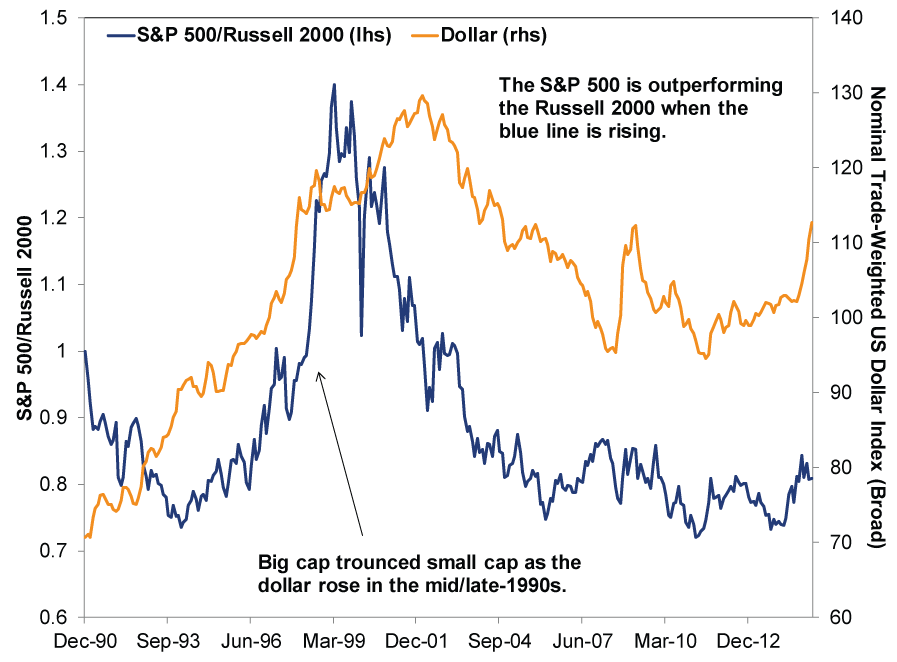

A quick look at the 1990s should throw cold water on the theory a strong dollar is automatically bad for large-cap US stocks. As Exhibit 1 shows, the dollar and S&P 500-the benchmark large-cap US index-soared for most of the mid-to-late 1990s. The S&P 500 also outperformed the small-cap-heavy Russell 2000 by a mile during this stretch (Exhibit 2).[ii] This doesn't mean large-cap US stocks always correlate with the dollar! But it does show US multinationals can (and do) do fine when the dollar is up.

Exhibit 1: Large Cap and the Dollar

Source: FactSet, as of 2/2/2015. S&P 500 Total Return Index and Nominal Trade-Weighted US Dollar Index, Monthly, 12/31/1990 - 1/31/2015.

Exhibit 2: Large Cap Vs. Small Cap and the Dollar

Source: FactSet, as of 2/2/2015. S&P 500 Total Return Index, Russell 2000 Total Return Index and Nominal Trade-Weighted US Dollar Index, Monthly, 12/31/1990 - 1/31/2015. S&P 500 and Russell 2000 relative returns are indexed to 1 on 12/31/1990.

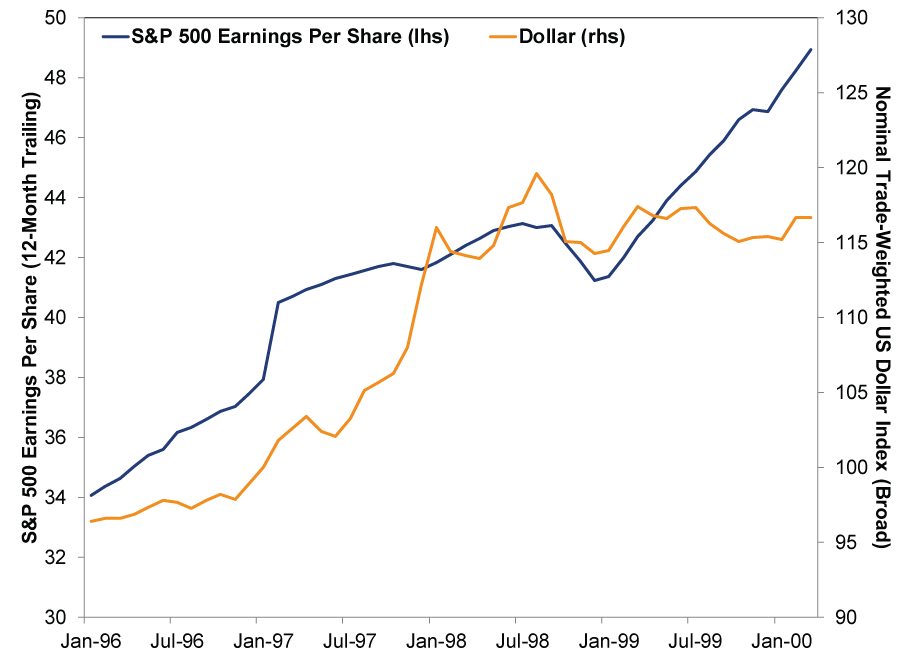

A strong dollar isn't necessarily a brake on large-cap firms' earnings growth, either. As Exhibit 3 shows, S&P 500 earnings per share rose alongside the dollar throughout the mid-to-late 1990s.

Exhibit 3: Large Cap Earnings and the Dollar

Source: FactSet, as of 2/2/2015. S&P 500 Earnings Per Share and Nominal Trade-Weighted US Dollar Index, Monthly, 1/1/1996 - 3/31/2000.

How can this be, when a strong dollar hurts US multinationals' export revenues? Simple: Few US firms export goods made with 100% US-sourced inputs. Most import components and raw materials. When the dollar is strong, these imports are cheaper, which reduces input costs. That offsets a good chunk of the dollar's impact on overseas sales, helping protect margins. Plus, overall and on average, less than half of US multinationals' revenue comes from overseas.

As for today, we don't see much evidence all the strong-dollar hollering hits the mark. Yes, S&P 500 earnings slowed in Q4, with growth falling to just 2.1% y/y with 227 companies reporting as of 1/30. Revenues slowed, too, growing just 1.4% y/y thus far. And many companies have cited the stronger dollar as their primary headwind. But CEOs have a long history of reaching for convenient culprits whenever results disappoint. After all, part of their job is to keep investors buying their stock even if earnings look a bit sad. Blaming disappointing numbers on external factors they can't control is an easy way to deflect-why blame company shortcomings and poor decision-making, spooking investors, when you can point fingers at the weather, currency swings or Vladimir Putin? It's mostly marketing spin, folks.

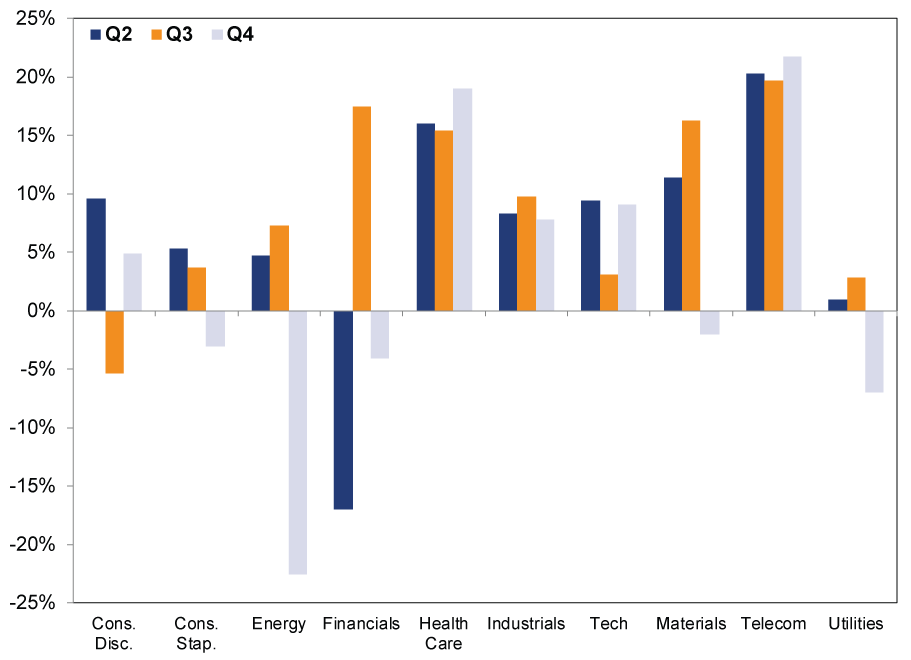

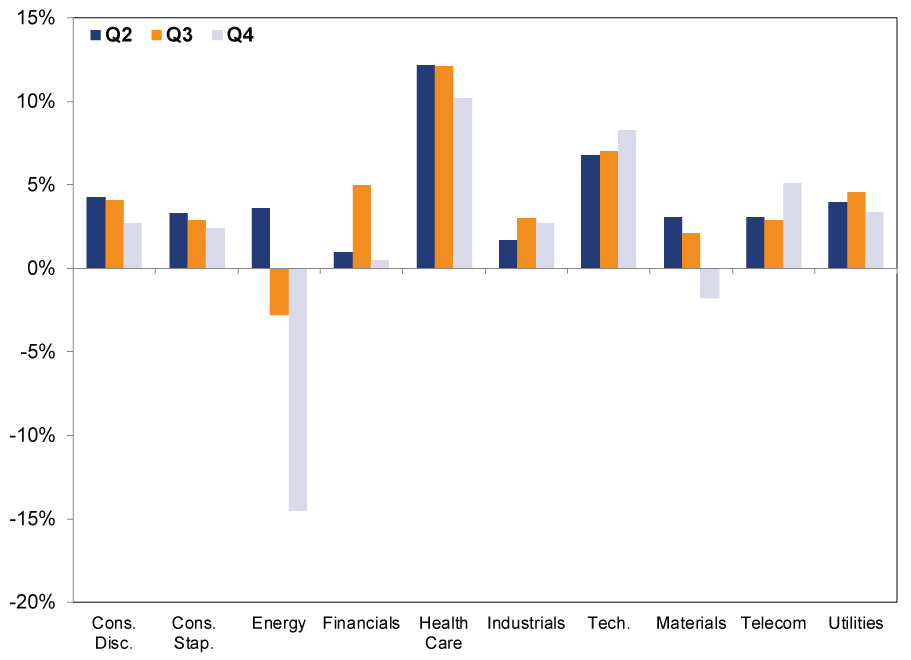

Plus, if you view earnings and revenues by sector, things don't look bleak (Exhibits 4 and 5). Unsurprisingly, Q4's biggest laggard is Energy-falling oil prices hurt. Utilities, were second worst-nothing to do with exports. Ditto for Financials. However, Technology, Industrials and Consumer Discretionary, which export a heck of a lot, all grew fine. Revenues grew fine in Q3, too, as the dollar started climbing.

Exhibit 4: S&P 500 Earnings Growth by Sector

Source: FactSet, as of 2/2/2015. Y/y growth in S&P 500 earnings per share, Q2 - Q4 2014. Q4 earnings are preliminary, with 227 firms reporting as of 1/31/2015.

Exhibit 5: S&P 500 Revenue Growth by Sector

Source: FactSet, as of 2/2/2015. Y/y growth in S&P 500 revenues per share, Q2 - Q4 2014. Q4 earnings are preliminary, with 227 firms reporting as of 1/31/2015.

Even if earnings growth slows from here, it needn't spell the end for this bull market. Earnings have slowed and even dipped plenty of times during bull markets-it's fairly normal as bulls age and year-over-year comparisons become tougher to beat. Also, stocks and earnings don't move one-to-one. As bull markets progress and investors become increasingly confident, they usually bid more for future earnings, pushing valuations up. They also usually focus on the biggest stocks, not small cap. The longer bull markets last, the more individual investors spooked out of stocks during the prior bear market feel comfortable coming back to stocks. These folks are naturally more skittish and don't gravitate toward what they see as risky, speculative smaller stocks. They go for big blue chips with names they know-or broad index funds, which are heavily skewed toward large caps if they're based on cap-weighted indexes. So the biggest stocks usually benefit disproportionately from improving sentiment late in a bull.

You won't read this most places, but that's ok. Unpopular categories are often the most profitable for investors-expectations are lower. Small cap today earns plaudits because of recency bias (assuming what has just happened will keep happening) and errant assumptions. With pundits hyper-focused on small-cap mythology and largely ignoring contrary evidence and fundamental reality, large-cap US stocks seem ripe for a happy surprise. Strong dollar fears are largely bricks in big-caps' wall of worry.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Ye olde recency bias.

[ii] The flipside is also true. In the 2002 - 2007 bull market, small cap outperformed amid a weak dollar. Again, not saying this correlation is causal, just that it doesn't support the notion that huge multinational firms do best with a weak dollar and lag when the dollar is strong.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today