Personal Wealth Management / Market Analysis

A Break in the Regulatory Clouds

Central bank chiefs eased a key provision of the Basel III banking standards, which should help ease ongoing regulatory uncertainty.

The world’s banks won a small reprieve from tough regulatory changes on Monday, when central bank chiefs eased one of Basel III’s key liquidity requirements. Though this only incrementally improves global regulatory uncertainty, the added flexibility could enable banks to avoid having to raise capital in the near term—potentially freeing funds for a bit more lending, perhaps easing one global economic headwind.

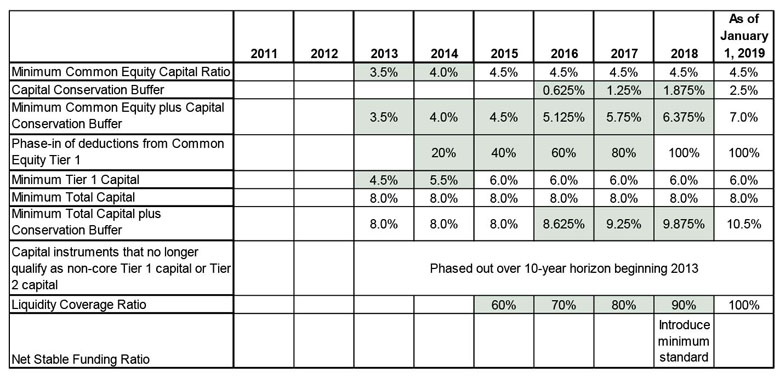

The potential side effects of implementing Basel III—the new global banking standards, which gradually take effect between 2013 and 2019—are one of today’s less-frequently discussed potential risks. Drafted in response to the events of 2008, the new rules increase the amount of capital banks must keep, with the largest banks facing even stricter requirements. The new rules aim to prevent a repeat of 2008’s wave of bank failures and bailouts—a fine goal. But as originally drafted, they threatened to interfere with banks’ ability to lend freely during normal environments, and they made it possible even compliant banks would have to raise significant capital during times of crisis, potentially causing interbank funding markets to freeze (exactly what the framers claimed to want to prevent). Monday’s changes should offer improvement on both fronts: Banks will get four extra years to implement the Liquidity Coverage Ratio (LCR), the list of eligible assets will expand and banks will be able to tap the liquidity buffer in times of stress.

The LCR requires banks to keep a pool of High Quality Liquid Assets (HQLA) equal to or greater than the total net cash outflows expected over the next 30 days. This aims to ensure banks can access enough cash to meet their liquidity needs for 30 days during a “liquidity stress scenario” at a moment’s notice. Under the original agreement, the rule would enter into full force in 2015, and only cash, central bank reserves, short-term sovereign debt, government bonds, covered bonds and high-rated corporate debt would qualify. Now, the rule will phase in from 2015 to 2019, with the ratio starting at 60% in 2015 and rise 10 percentage points annually. Additionally, lower-rated corporate debt (A+ to BBB-), certain equities and mortgage-backed securities (AA or higher) become HQLA, though with 25% to 50% haircuts off their face values.

In our view, this is much more logical than the original rule—the gradual phase-in gives banks somewhat less incentive to hoard capital today, while the broader HQLA eligibility eases banks’ compliance burden without watering down protections. Equally important, banks now have some clarity on the future regulatory environment. Since the LCR was introduced in 2010, many countries and banks have lobbied for amendments, and most assumed the rule would change. But without knowing exactly how it would change, banks couldn’t properly plan, and many opted to “wait and see” rather than lend aggressively now and risk having to shore up capital later. With the (easier) rules now in place, banks can likely plan and lend a bit more.

The other key change should help ease pressure on banks during tougher times. As originally written, the rule would have required banks to maintain a 100% LCR at all times, forcing them to raise capital to meet liquidity needs during times of stress (a procyclical regulatory measure)—arguably when raising capital is most difficult! Banks whose LCRs fell below 100% would have potentially been treated as insolvent even though they had perfectly large capital buffers. Allowing banks to tap these reserves removes this risk and makes perfect sense, in our view—what’s the point of having extra liquidity if you can never use it?

Overall, these changes are a welcome relief and should give banks a bit more latitude to lend. That said, given other existing headwinds, we wouldn’t expect a flood of lending overnight. Other Basel III requirements begin phasing in this year (See Exhibit 1 for a full timeline), and pending national regulatory changes are still causing uncertainty globally. These include Dodd-Frank in the US, upcoming UK legislation based on the Independent Committee on Banking’s recommendations, France’s recent proposal to ringfence retail and investment banking and the eurozone’s ongoing deliberations on a common banking supervisor, to name a few. Plus, monetary policy in the US and UK, which flattens the yield curve and pays banks to park excess reserves at the central bank, gives banks there additional incentive against lending more freely.

The silver lining is slower lending slows the velocity of money, which should help keep inflation in check, mitigating another investor worry. But it likely also keeps the global economy from growing as much as it otherwise would. That the economy continues growing despite this headwind is a testament to its underlying health and the private sector’s strength—a positive for stocks.

Exhibit 1: Basel III Phase-in Timeline

Source: Bank for International Settlements. Shading indicates transition periods.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

In The News Expert says investors are ignoring a massive global rally2026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today