Personal Wealth Management / Market Analysis

A Breath of Fresh Air in Buenos Aires?

Investors are hot to trot for Argentina after Sunday's election, but markets move most on the gap between reality and expectations, and the new President has a tough road ahead.

Is this picture of blue skies over El Chalten in Patagonia a visual metaphor for Argentine stocks after Sunday's election? Photo by Luis Davilla/Cover/Getty Images.

Editors' Note: As always, our political commentary is non-partisan. We favor no political party and aim to analyze legislation, potential legislation and other policies from a capital markets standpoint only. Political bias is a dangerous error in investing.

Argentinians said "no, thanks" to another four years of Kirchnerismo Sunday, ending 12 years of Peronist presidents by electing the center-right mayor of Buenos Aires, Mauricio Macri. Out with the oil industry-nationalizing, economic mismanaging, hedge fund battling regime of Cristina Fernández de Kirchner and her late husband, Néstor Kirchner, and in with a former soccer executive who pledged to crack down on corruption, restore competitiveness and rebuild creditworthiness. Now the Internets are full of articles touting Argentina's newfound promise for foreign investors. Seems like a good time to remind investors everywhere of an age-old truth: Markets are party-blind and move on the gap between reality and expectations. The ascendance of a market-friendly leader often isn't a one-way ticket to sky-high returns, and it's important to assess all drivers-economic, political and sentiment-when making investment decisions.

Recent history features several reform-minded leaders who cheered, then disappointed markets. Shinzo Abe in Japan. Manmohan Singh in India. Nicolas Sarkozy in France. All made rousing pledges to unlock their economies' potential, reform bloated systems and boost investment. But after they took office, reality took hold. Some ran into entrenched opposition in their legislatures or in influential interest groups. Others lost political capital. Some just plain lost the will to press on. Overall and on average, all these gents fell short of expectations, to varying degrees, disappointing investors who let shiny campaign pledges sway their portfolio decisions while ignoring sentiment or the economic outlook.

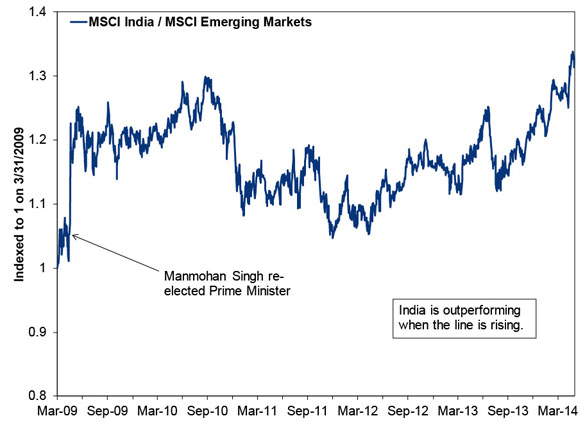

India is perhaps the most striking example (Exhibit 1). Singh was re-elected on May 16, 2009, strengthening his clout as his Congress Party upped its seat count by 61. His stronger majority heightened expectations for his second term, and investors' hopes for reforms hit the stratosphere. So did Indian stocks. On May 18, the first trading day after Singh's victory was announced, the MSCI India rose an astounding 17.9%.[i] But relative returns over his first year were choppy as opposition in his own coalition and among state governments thwarted many of his plans. India underperformed for most of 2011 and 2012 as he battled entrenched interests over opening up the retail sector to foreign investment-a move that would have boosted investment in India's creaky agricultural infrastructure and improved chronic food shortages (fully one-third of Indian produce rots in storage). He finally made some headway later in 2012 and 2013, as some government defections helped break key logjams, but investors had to wait years for the payoff.

Exhibit 1: MSCI India Relative Returns, Manmohan Singh's Second Term

Source: FactSet, as of 11/23/2015. MSCI India and MSCI Emerging Markets returns with net dividends, 3/31/2009 - 5/29/2014. Indexed to 1 on3/31/2009.

We see the same thing time and again in America in a little phenomenon we call the "perverse inverse." In our experience, about two-thirds of US investors lean Republican and perceive the GOP as market-friendly. Republican candidates also regularly campaign on pro-business platforms. That heightens hopes for market-oriented changes under a Republican administration, and it drives above-average returns in election years when the GOP wins the White House. But in the inaugural year, high hopes are usually dashed as all those campaign pledges are scrapped or watered down-sometimes because Congress blocks them, and sometimes because the new President turns out to be just another politician, trying his best not to alienate voters and jeopardize his re-election chances. A Republican has won the presidency 10 times since 1928. In their inaugural years, US stocks posted below average returns eight times-outright declining seven times.

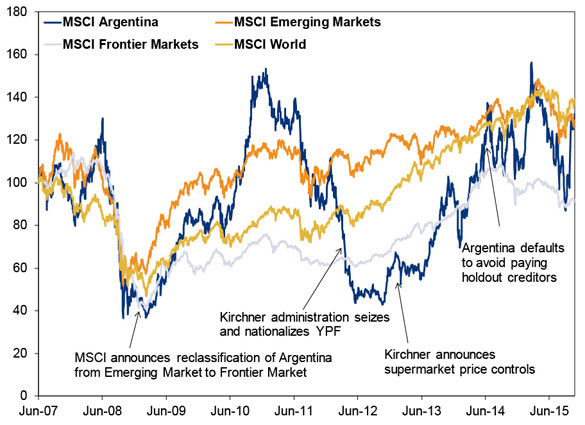

The reverse of all this is true, too: The presence of a nominally anti-market leader doesn't guarantee terrible returns. Here, too, it is about the gap between reality and expectations. As Exhibit 2 shows, Argentina outperformed wildly at times throughout Cristina Kirchner's eight years, despite her policy misadventures, a faltering economy and inflation that neared 30% annually by some estimates.[ii] Getting downgraded by MSCI from Emerging to Frontier Market in 2009 was supposed to confirm Argentina's long-term decline and cement its status as a submerging market. Instead it kicked off nearly two years of amazing relative returns, during which Argentine stocks nearly quadrupled. For as much as Kirchner's government intervened with markets-and as erratic as her behavior became later in her term-she never went fully down the road of Hugo Chavez-style communist authoritarianism. Hence, Argentina's political scene beat some very dreary expectations.

Exhibit 2: Argentina During the Kirchner Years

Source: FactSet, as of 11/23/2015. MSCI Argentina, MSCI Emerging Markets, MSCI Frontier Markets and MSCI World Index returns with net dividends, 6/30/2007 - 11/22/2015. Indexed to 100 on 6/30/2007.

That chart is a bit messy, but eagle-eyed readers will notice a big spike in Argentine returns at the end. Since September 30, they're up more than 48%.[iii] After Macri's surprising showing in the election's first round on October 25 triggered Sunday's run-off, the MSCI Argentina rose 28.3% through November 20.[iv] Markets have a long history of moving in advance of big events like this, and that big pre-election rise is a strong indication markets have already started pricing in the changing of the guard. If you need evidence stocks often do what few expect, look no further than Argentine markets on Monday: Stocks there fell -5.1%.[v]

Macri will join Indonesia's Joko Widodo and India's current Prime Minister, Narendra Modi, as would-be reformers facing high market expectations. Theirs is not an impossible task, and Modi and Joko have made some progress thus far. But Macri's road is the hardest. For one, Kirchner's party controls Argentina's legislature, making sweeping change difficult. Macri has already suggested he won't push for major overhauls like privatizing the state-owned Energy giant YPF.[vi] Argentina also remains locked out of international debt markets, and Macri will have to settle the state's dispute with US creditors to regain market access. He will likely also have to float and devalue the peso, as the central bank is running out of foreign exchange reserves-probably a positive move in the long run, but it will make life harder for households that haven't had to adapt to higher prices in the black market. High social spending, which Kirchner's government funded by ordering the central bank to print pesos, is also almost sure to fall. Though necessary to shore up state finances, the eurozone has proven time and again voters don't have much patience for social benefits cuts. Macri's political capital could erode quickly, further limiting his ability to pass reforms.

Now, that preceding paragraph could be too pessimistic. It is entirely possible Macri and his team settle with creditors quickly, find a happy medium and communicate their policies well enough to keep voters happy-after all, he has a choice between shock treatment and a gradual approach. He hasn't even taken office yet, much less outlined a detailed economic program, so it is too early to handicap his chances of success. This is a classic "wait and see" moment. But it illustrates the importance of carefully weighing potential reality against expectations-and the importance of throwing away the rose-colored glasses. The more sentiment heats up, the harder it will be for Argentina to live up to the hype.

Again, the same goes for all countries facing high political expectations. Don't let narratives carry you away. Weigh the facts and likely outcomes carefully, and measure them against sentiment. If you have compelling evidence reality can meet or beat expectations, go for it (but never over-concentrate). But don't let bias or hopes blind you.

[i] FactSet, as of 11/23/2015. MSCI India return with net dividends on 5/18/2009.

[ii] Argentina's official inflation rate was about 10% annually, but because it didn't include black-market prices (necessary because price controls caused shortages in several categories), most believe it habitually undershot. Many also believe official GDP statistics overestimated growth throughout Kirchner's tenure. Her administration also fired and jailed statisticians who questioned the official narrative.

[iii] FactSet, as of 11/23/2015. MSCI Argentina returns with net dividends, 9/30/2015 - 11/20/2015.

[iv] FactSet, as of 11/23/2015. MSCI Argentina returns with net dividends, 10/23/2015 - 11/20/2015.

[v] FactSet, as of 11/23/2015. Daily price return for Argentina's Merval Index.

[vi] This is the firm Kirchner's government seized from Spain's Repsol in 2012, launching a multi-year battle over compensation.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today