Personal Wealth Management / Market Analysis

A Closer Look at the Fiscal Cliff

Though oft-bemoaned in the media, the so-called fiscal cliff, when broken down, is likely a lot less worrisome than presented.

You’ve probably heard by now that unless US politicians take action, the domestic economy will plummet over a “fiscal cliff” on January 1, 2013—with a possible US recession to follow. However, if you look at the so-called fiscal cliff’s separate components and consider what politicians are likely to do, the overall impact seems a lot less worrisome.

The Congressional Budget Office (CBO) projects the full brunt of the fiscal cliff will slow GDP during the first half of 2013 by 1.3% (annualized), followed by 2.3% annualized GDP growth in the second half—with full year GDP growth of 0.5%. (Yes, the CBO projects positive GDP growth despite the fiscal cliff.) Set aside the fact the CBO has a not-so-great track record for projecting fiscal impact (not entirely their fault—they spit out projections based on assumptions [often lousy ones] handed to them by politicians).

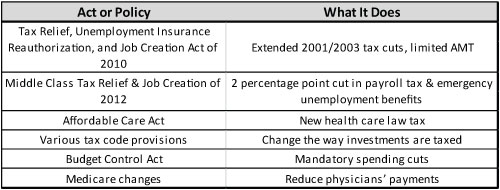

What are the odds nothing changes between now and when the fiscal cliff kicks in? Not great, in my view. Though often portrayed as a monolithic beast, the fiscal cliff is actually a series of policies—shown in Exhibit 1. Extending or modifying even some of the components can significantly change the impact.

Exhibit 1: Fiscal Cliff Components

Source: Congressional Budget Office.

For example, President Obama has proposed a one-year extension of the 2001/2003 tax cuts for families earning less than $250,000 a year, while Republicans prefer extension for all. Democrats seem keen to extend jobless benefits and possibly the payroll tax cut, whereas Republicans likely won’t favor extending jobless benefits. But as they’ve done before, Republicans may bend if they get a full extension of the Bush-era tax cuts. Or consider the Affordable Care Act, which Republicans have said they’d repeal, thereby negating those tax impacts altogether if successful—a tall order, but still a possibility. And there’s nothing preventing further delays or shifts on any of these taxes.

Congress is set to vote on the budget for fiscal year 2013 (which starts October 1) over the next few months, and the House has already passed legislation to replace the sequestered spending cuts with other cuts. (And as many senators alluded to during the so-called supercommittee talks, these cuts are by no means actually binding. Legislation can, and often does, change.) Since Congress hasn’t passed a budget in over three years, I can’t see why that changes this year. What’s more likely, regardless of who wins in November, is some sort of compromise that minimizes the fiscal cliff’s impact. Neither party wants to be associated with raising taxes, when they could position themselves as champions of the little guy (or small businesses, or job creators, or, or, or). But neither does either party want a truly permanent solution, which would take away their ability to similarly leverage the issue in future election cycles.

In short, it’s important to keep in mind this is much more a political issue than a fiscal or economic one. The fact is, of the acts or policies listed in Exhibit 1, only the Affordable Care Act is new—all of the others components have previously been extended or modified by the government. What’s to keep them from doing so again? Furthermore, we’ve seen this movie before—just last summer, when politicians came through in the 11th hour and extended the debt ceiling (something that had happened 90 times before but seemingly still required months of political debate).

Even if the fiscal cliff goes wholly unaddressed—which is a possibility, albeit a rather remote one, in my view—keep in mind it’s a US-only issue. Similarly, though higher taxes would be an incremental negative, they’d be a US-only incremental negative. Tax changes may annoy—but to date, there’s never been a bear market caused by incremental changes to tax rates and spending. The reality is the country-specific impact is just too small in a fully globalized market and the changes too telegraphed (tax changes sneak up on nearly no one).

Over the next few months, expect plenty of political rhetoric from both sides asserting their side is right and the other cruel and heartless. This is par for the course—especially in an election year. But the fiscal cliff may in fact be the only cliff in history that can be assembled and disassembled, moved, extended or altogether done away with. In this way, it’s more a sand dune than an actual cliff.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

-

Market Analysis Investors Are (Still) Fighting the Last War on Inflation2026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today